The IndeX Files 17-09-2019

Risks Remain Amidst Positive Backdrop

The fundamental backdrop for equities remains supportive in the near term though benchmarks in the US, Europe, Asia and the UK have seen a pause in momentum so far this week.

The announcement of a new range of easing measures from the ECB at its meeting this month has helped keep European equities well bid. The central bank announced a cut to the deposit rate along with the restarting of QE. While the measures underwhelmed some elements in the market, creating a counter-intuitive bullish move in EUR, the DAX has seen steady buying.

The latest developments in the Brexit space have given a positive contribution also as it now looks unlikely that the UK PM will be able to push ahead with a forced no-deal Brexit. Following the passing of the Benn Bill last week, UK parliament can now require the PM to officially request an extension to the Article 50 process should it be unable to approve a deal (or agree to exit without a deal) by October 19th. While the reduced risk of a no-deal Brexit has created upward pressure in GBP, UK asset prices have also appreciated as investors welcome the further postponing of a potential economic cliff.

Traders are readying themselves for a further easing announcement from the Fed this week with the market expecting another 25 basis point cut. Recent US data points have highlighted remaining weakness and while there have been improvements in the expectations for a positive outcome to trade negotiations between the US and China, uncertainty and risks remain.

Volatile moves in WTI this week have been largely responsible for creating a pause in equities . A drone attack on Saudi Oil sites at the weekend resulted in a 20% jump higher in WTI on Sunday evening. Despite some initial pull-back following the move, WTI is now higher once again as the risk of military conflict between the US and Iran has grown.

Technical & Trade Views

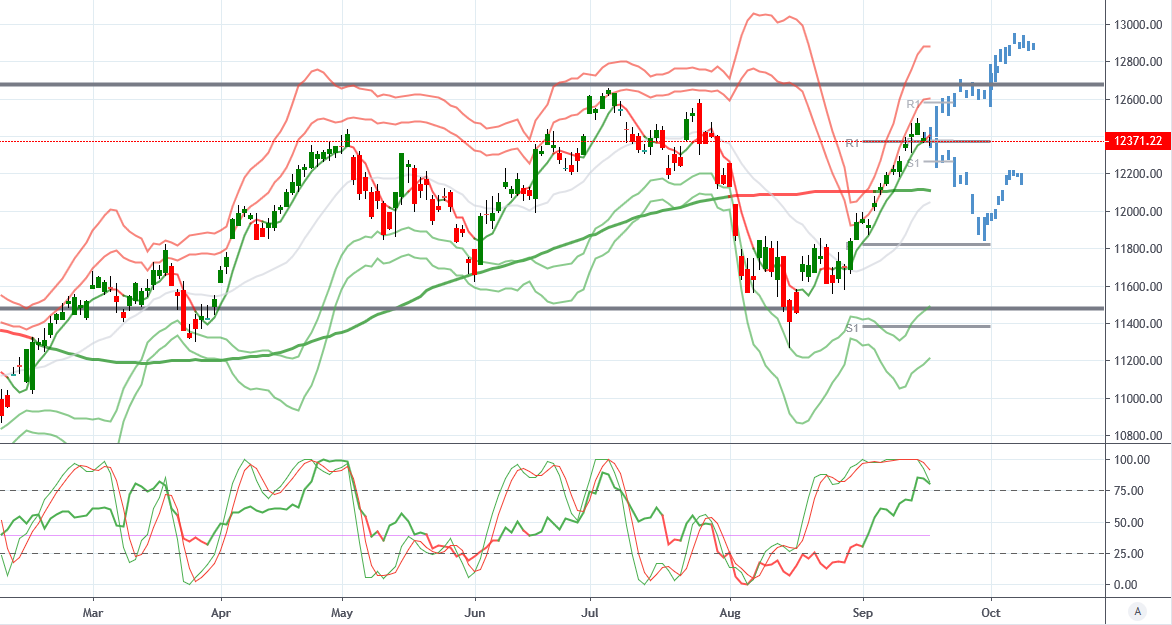

DAX (Bullish above 12382, targeting above 12663)

From a technical and trading perspective. On a wider scale, Index continues to range between the yearly pivot between the 11490 level and the year R1 at 12689. In the near term, indicators support further upside with bias towards an eventual break of the R1 and a push higher. If the index suffers losses from here, I will be monitoring any retest of the 11822 support for bullish reversal candles to initiate long positions.

S&P (Bullish above 2971, targeting above 3035)

From a technical and trading perspective. The index has made solid gains recently taking the market back to just below all-time highs. I will be looking to use a break and retest of the monthly R1 level to set fresh longs. On the other hand, momentum indicators raise the risk of a short term pullback in which case I will be monitoring support at the 2906 level for long opportunities.

FTSE (Bullish above 7300, targeting above 7600)

From a technical and trading perspective. FTSE finds itself in the middle of the range between the yearly Pivot (7056) and yearly R1 (7577). VWAP continues to support a push higher to test offers into the 7577 level, for an eventual break. However, given the uncertainty in the backdrop, a pullback into the 7056 cannot be ruled out which I will be watching as a test of this base should offer long opportunities.

Nikkei (Bullish above 21771, targeting above 22374)

From a technical and trade perspective. The Nikkei is once again testing the medium-range bearish trend line. If selling pressure creates a pullback here I will be watching for bullish reversal candles between 21545 and 21173 for longs targeting an eventual break above the trend line. Should any pullback run deeper than 21173, we are likely to see some ranging play around the yearly pivot.

Please note that this material is provided for informational purposes only and should not be considered as investment advice. The views discussed in the above article are those of our analysts and are not shared by Tickmill. Trading in the financial markets is very risky.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!