April ECB Minutes Show the Central Bank Doesn’t Know What to Expect

The minutes of April ECB meeting, released on May 22, revealed that the Central bank is eager to deliver more. “Minutes” are worthless they say, because it’s priced in... not the case this time.

Two key things from the report: the ECB is ready to ease credit conditions more and the fact that PEPP remains key policy tool. By the way, PEPP is an emergency “pandemic” program of purchases of private and public sector securities in the amount of 750 billion euros and which will be in effect until the end of 2020. Programs of this kind are usually done in crisis. Their key feature is lowered bar for quality of purchased debt. The key purpose is to directly buy debt of struggling firms and local governments, which are avoided by other creditors because of concerns about creditworthiness. The launch of the program basically leads to the appearance of indiscriminate buyer on the market which hampers market price discovery, leads to excessive risk-taking, etc., but these are considered to be manageable “side effects”. Another issue is that the program has a limit and it will end soon. With current pace of buying the ECB will reach the current limit in September-October. But the minutes, as we see, hinted that extension of the PEPP limit may be on the agenda of one of the next meetings. Given the ECB’s bias to act proactively, the expansion of PEPP may be discussed as early as June.

It is also curious that the ECB for the first time described medium-term uncertainty as radical uncertainty – i.e. risks which can’t be quantified. The Central Bank seeks a solution, experimenting more with preventive policy decisions which tend to cause positive shocks in market sentiments.

The USD index rose at the start of Monday although losing punch later, but it wasn’t about stronger USD: the cause of gains was weaker euro, which has the biggest weight in the index.

IFO index update showed expectations rose higher than expected, but assessment of current situation was worse than expected. A number of survey indicators for May, which we analyzed earlier, where respondents were asked to assess future expectations, turned out to be better than forecasts. This also indicates that a lot of expectations are priced in equities.

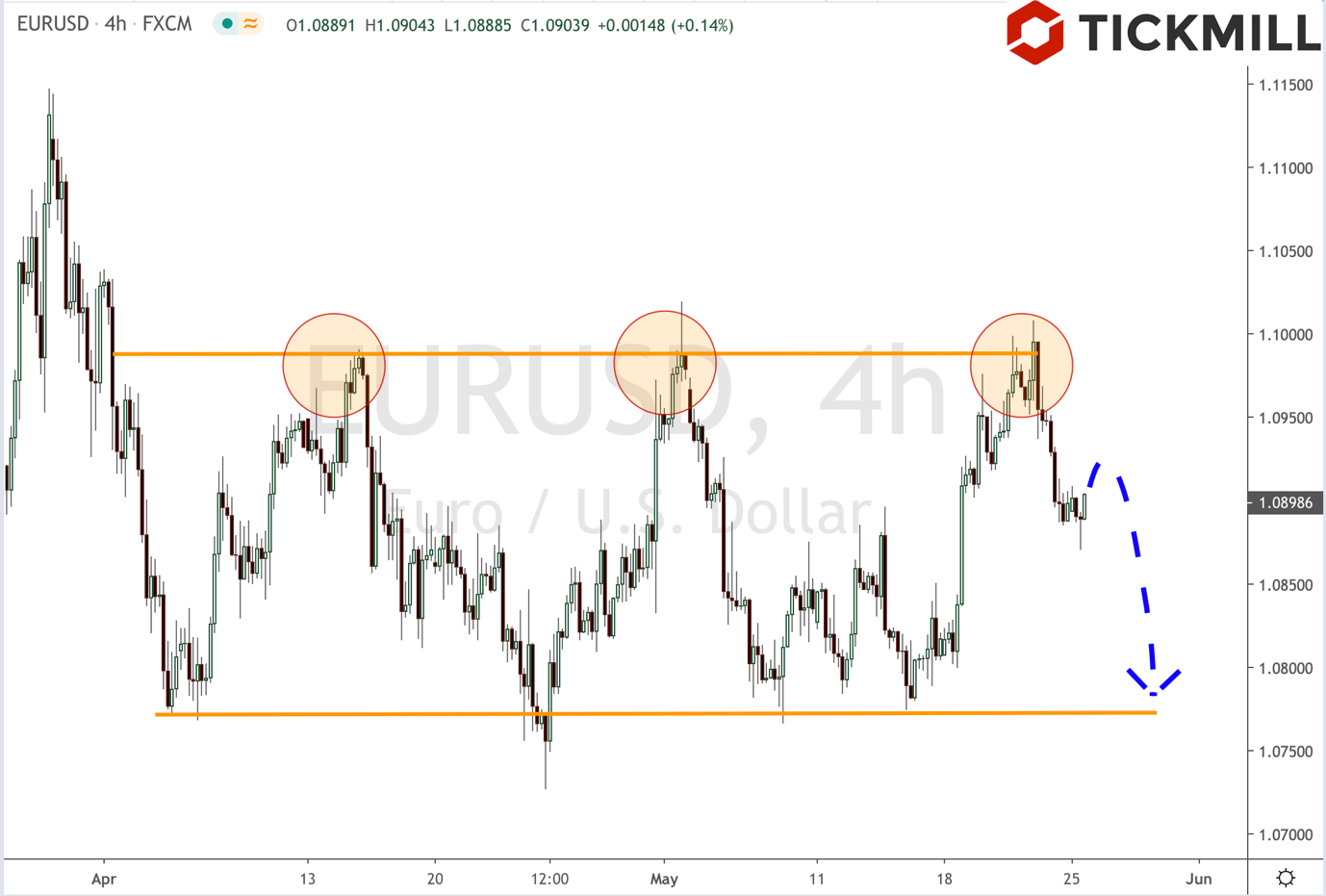

On balance, the balance for euro shifts towards more declines with possible test of the lower bound of two-month range:

In Asian markets, attention has been drawn to a rise in the USDCNY reference rate to its highest level since the 2008 crisis. Pressure on the yuan is rising due to capital outflows, and the central bank of China has “officially recognized” this, weakening CNY official rate. Investors are getting rid of Chinese assets because of fear that a new conflict between China and the United States may escalate into a full-fledged financial war. The dynamics of USDCNY over the past two years shows that the mainland yuan depreciated against the dollar whenever Trump threatened tariffs and strengthened anti-Chinese rhetoric. The last episode of the weakening of renminbi probably reflects an anxiety of the same nature:

Accordingly, the demand for risk can get hit from this front as well, which is undoubtedly a positive factor for strengthening the dollar.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 73% and 70% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.