Bond Markets Discount Weak NFP, Focus is Back on Inflation

Weaker-than-expected September NFP report put a drag on broad USD rally. On Monday the greenback index struggles to resume advance, hovering not far from 94 points, forming a breakout “triangle” pattern. At the same time, the price continues to consolidate near September 2020 highs:

US job growth totaled 194,000 in September, with more than 11 million job openings in the same month. The labor supply deficit continues to restrain employment growth, which should translate into even greater wage inflation. By the way, the growth of wages again exceeded the forecast and amounted to 0.6% instead of the expected 0.4%.

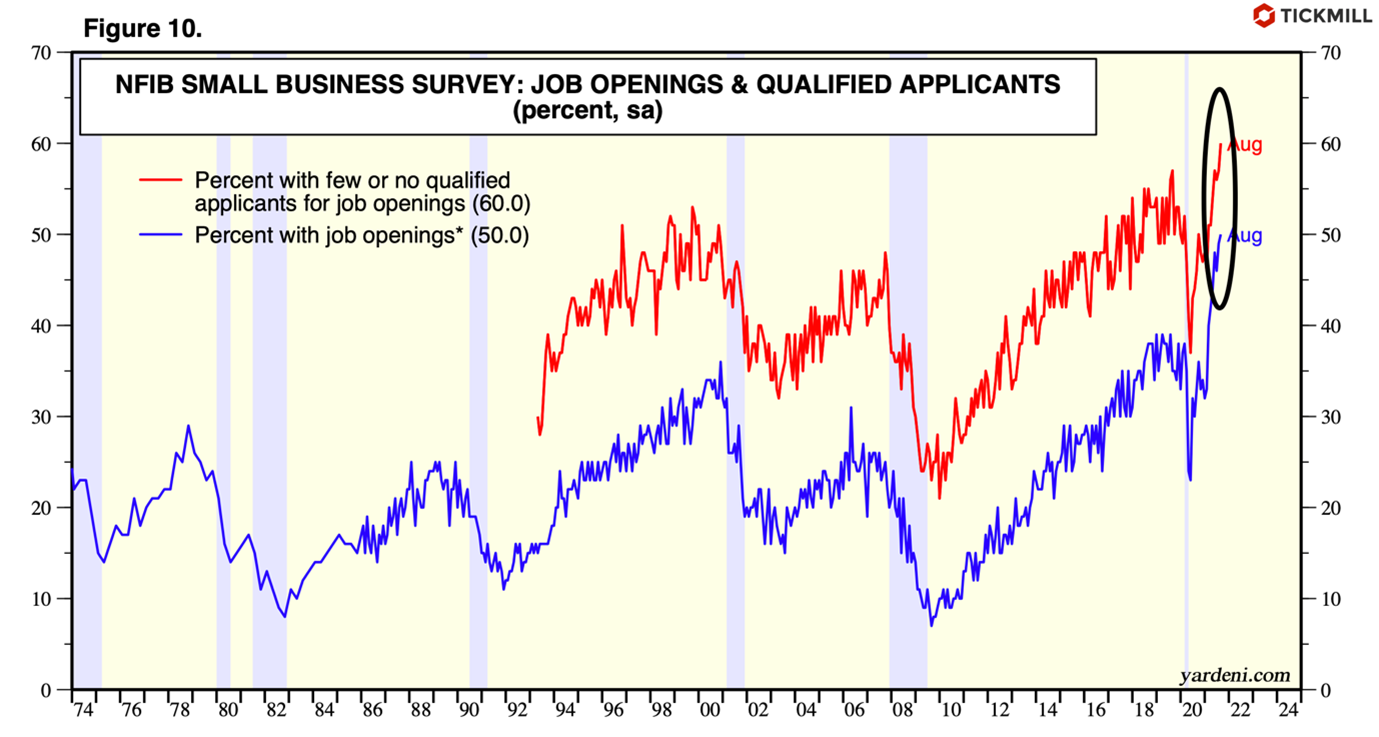

Earlier NFIB reports showed that the share of small businesses with open vacancies and experiencing shortage of skilled workers is at record levels:

The fact that the US government cut the number of jobs at once by 123K in September helped markets to discount the weak Payrolls figure.

The Treasuries market also ignored weak job growth as, after a short-term decline, bond yields began to rise again, signaling that the market was quickly discounting fears of a slowdown in economic activity due to the weak NFP print and again focused on inflation risks:

Chances that the Fed will announce QE tapering in November remain high, supporting the dollar and keeping bonds under pressure.

It is difficult to expect inflation expectations to stabilize or turn into decline when there is a strong uptrend in the oil market and fears of possible deficits are not abating. On Monday, the WTI price tested $ 81.50, the highest since October 2014. Gas storage facilities in Europe are 76% full, with a 5-year average of 91% before the heating season. China is trying to ramp up coal production, but heavy rains in Shanxi are forcing some mines to suspend production.

Considering the recent rally, it was expected to see the growth of long positions of speculators in the COT data. The long position in WTI increased by 18K lots to 316K lots, but if you look at the July high of 426K lots, there is still room to build up long positions. On Brent, the growth in the net-long position of speculators turned out to be more modest - only 3.7K lots.

Also on the agenda of this week are the OPEC and IEA forecasts for the growth of oil consumption. Investors will analyse growth forecasts, taking into account the demand that has arisen due to the transition from expensive gas to oil, because the stabilisation and decline in gas prices could strongly affect the forced demand for oil and hit the prospects for a rally.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.