Daily Market Outlook, December 16, 2020

Daily Market Outlook, December 16, 2020

Asian equity markets are mostly up this morning ahead of tonight’s US Federal Reserve policy announcement. Leaders of the four UK nations will discuss Christmas arrangements today amid calls for the advice on behaviour to be strengthened. There are no new reports on progress with Brexit discussions, but media sources say that the UK parliament is on alert for an extended session next week to potentially pass legislation.

The UK November CPI showed a drop in annual inflation to 0.3% from 0.7% in October. The ‘core’ rate also slipped to 1.1% from 1.5%. That was the third successive month that headline inflation has been more than 1% point below the 2.0% target. It means that Bank of England Governor Bailey will need to write a letter to the Chancellor of the Exchequer explaining what action he intends to take. However, today’s outturn, while lower than expected, will probably not lead to any new monetary policy moves at Thursday’s BoE update.

The US Fed has its last monetary policy meeting of the year today. It seems most likely to leave monetary policy unchanged for now, particularly given renewed hope of more US fiscal stimulus. However, Treasury Secretary Mnuchin’s decision not to extend most of the Fed’s emergency lending facilities past the end of the year and some slowing of US economic data have led to speculation that the Fed may take some action. If that is the case, it will probably involve changes to its asset purchase programme.

Two possibilities have been suggested. First, enhancing its forward guidance to clarify what economic conditions would prompt a change in the programme. Secondly, a shift in the purchases towards buying longer-dated Treasuries to exert downward pressure on longer-term yields. Both moves seem likely at some point, but the Fed will probably leave them until next year.

After this week’s announcement of new restrictions in parts of England, today’s UK December PMIs may immediately look dated. Given the end to the November lockdown in England, we expect the headline services PMI reading to rebound back above the 50 mark that signals expansion, while manufacturing is likely to rise for the second straight month, helped as in November by stockpiling ahead of new EU trading arrangements.

Look for declines in both Eurozone PMI measures, with services expected to fall further below 50. That reflects a continued high level of restrictions in many Eurozone countries. US retail sales, which disappointed in October, may do so again in November primarily because of a slide in car sales.

Today’s Options Expiries for 10AM New York Cut

- EUR/USD: 1.2000 (1.2BLN), 1.2070 (820M), 1.2100 (1.1BLN), 1.2150 (450M), 1.2200-10 (500M)

- GBP/USD: 1.3300 (566M)

- AUD/USD: 0.7450-60 (1.2BLN), 0.7500 (1.2BLN)

- USD/JPY: 103.50-60 (510M), 103.90-104.00 (580M)

Technical & Trade Views

EURUSD Bias: Bullish above 1.20 targeting 1.23

EURUSD From a technical and trading perspective, as 1.20 now acts as support bulls target primary ascending trendline resistance to 1.23

Flow reports suggest offers light through to the 1.2180 area where offers are likely to be thick to the 1.2220 area and stops appear for possibly a strong breakout if that is possible, downside bids light through the 1.2080 area before weak stops appear for a chance at a quick move through to the 1.2060 level and stronger stops on any attempt through the 1.1980 areas and a failed topside opening up some further weakness through to the congestion around the 1.1900 areas

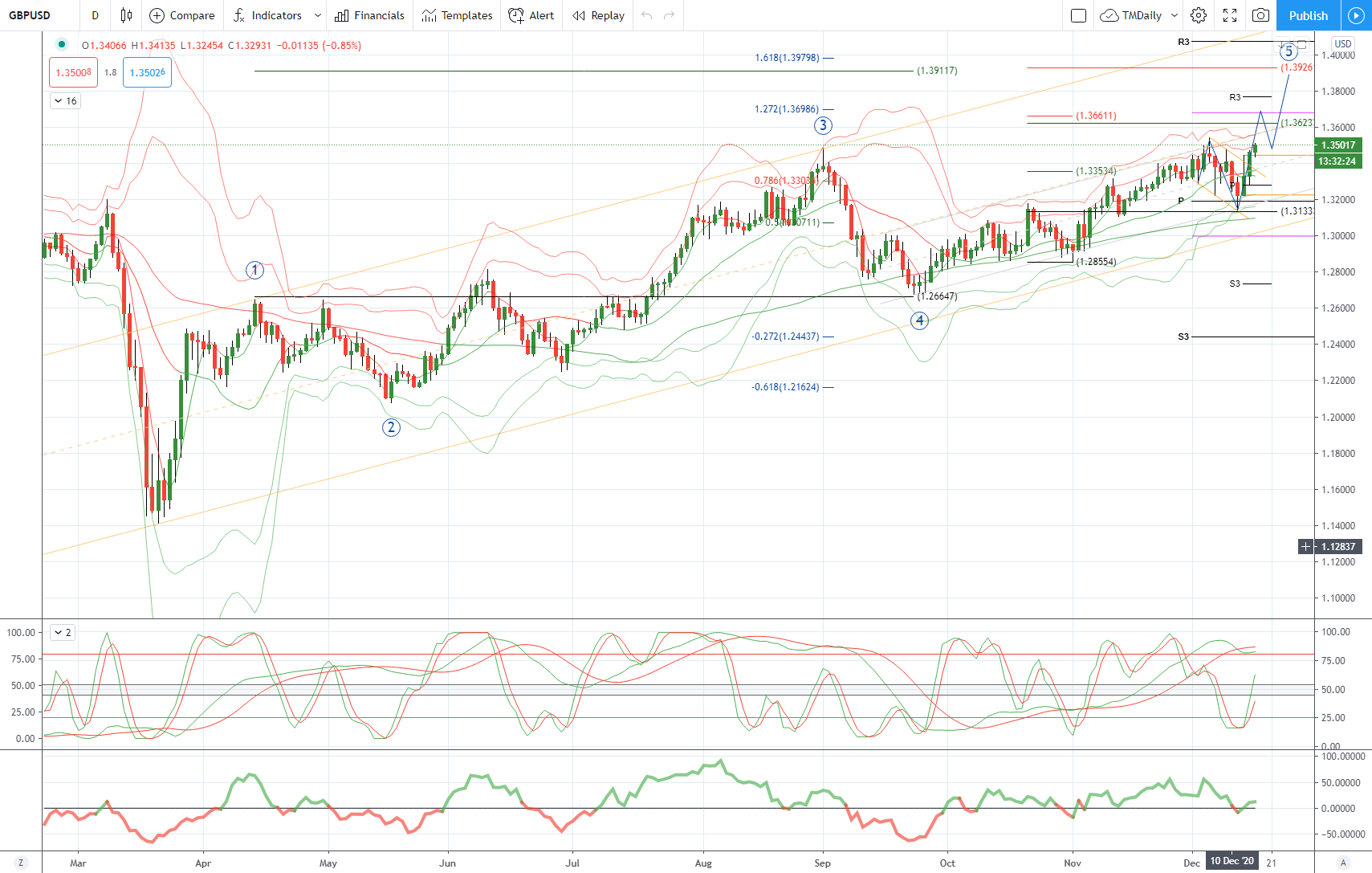

GBPUSD Bias: Bullish above 1.3175 targeting 1.39

GBPUSD From a technical and trading perspective, as as 1.3250 supports then prices can extend higher to test wave 5 upside objectives to 1.3910/80 area,failure below 1.3175 opens the pivotal 1.30

Flow reports suggest offers are likely to be piled up through to the 1.3550 area before some weakness starts to appear through to the 1.3800 area given a few days. Downside bids light back through the 1.3500 level with weak stops through the level and then opening to a quick move through to 1.3450 with limited bids appearing with weakness continuing through to the 1.33 handle

USDJPY Bias: Bearish below 105 targeting 101.20

USDJPY From a technical and trading perspective,near term short covering to challenge offers to 105 descending trendline resistance, as this area contains upside attempts look for the next leg lower to target year to date lows at 101.20

Flow reports suggest congested through to the 104.80 level where offers are likely to be a little stronger with weak stops on a move through the 105.20 level before further offers into the 105.50 area and weakness through to the 106.00. downside Bids into the 103.50 level increasing on move through the 103.00 area with the stops likely to increase through 102.80, topside offers likely to increase through to the 106.00 area with weak stops through the 106.20 area and increasing congestion on a push above the 106.50 level and into the 107.00

AUDUSD Bias: Bullish above .7230 bullish targeting .7700

AUDUSD From a technical and trading perspective, as .7240/20 now acts as support look for a retest of offers and stops above .7400 from here anticipate a profit taking pullback towards .7200 again before price attempts to extend higher again to target wave 5 upside objective towards .7700

Flow reports suggest strong offers on the move into the 76 cents area with likely weak stops in the usual 0.7620-30 area however, congestive offers likely to continue through to the 0.7750 areas with sentimental areas likely to be very strong, downside bids light back through the 75 cents area with weak stops on a dip through the 0.7480 area and the market then opening through to the 74 cents with very light bids.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72% and 75% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!