Daily Market Outlook, January 28, 2021

Daily Market Outlook, January 28, 2021

The US Federal Reserve left policy unchanged yesterday, as widely expected. Chairman Powell continued to push back on speculation that a ‘tapering’ of bond purchases may begin as soon as this year. He said “the whole focus on exit is premature''. That did not prevent the main US S&P500 index falling 2.6%, the most since October. The ‘risk off’ sentiment has followed through to the Asian trading session, with significant declines in major equity indices.

First estimates of Q4 GDP growth for the US and some major European economies over the next couple of days may be deemed backward-looking. Nevertheless, they are likely to show the divergence in economic performance that has opened up between the US and the Eurozone. Although US growth likely slowed in Q4, it is expected to have remained positive, as businesses and households adapt to Covid restrictions. Nevertheless, growth is forecast to have fallen sharply to around 4% (annualised) from over 30% in Q3, led by slower services activity and consumer spending.

In contrast, figures for France and Spain early tomorrow morning are expected to show a return to negative growth as a consequence of more restrictive lockdown measures. France, in particular, is forecast to have contracted by 4%.Germany may have just escaped a decline, helped by robust industrial activity, but overall Eurozone GDP (due next week) is expected to show a negative outturn following the stellar rise in Q3.

Another quarter of negative Eurozone growth in Q1 is a distinct risk as new coronavirus variants result in tighter and longer lockdowns. Vaccine rollout rates in the EU have also lagged behind some other countries, while there remains attention on the dispute with AstraZeneca about vaccine supplies. This morning’s Eurozone economic sentiment index (a weighted average of confidence measures, including consumer, industrial and services) is expected to fall back to 89.3 in January.

Accommodative ECB policy is also likely to be reinforced by subdued domestic inflation pressures. Today’s German January CPI is expected to jump higher because of the reversal of the temporary VAT cut and higher energy prices. That will probably bring Eurozone CPI, due next week, out of negative territory, but it will remain well below the ECB’s goal of ‘below, but close to, 2%’.

Finally, the Lloyds Business Barometer early tomorrow will provide a timely update on UK economic optimism and trading prospects. It will also give details on how businesses are feeling about Covid restrictions and vaccinations and the extent of disruptions to EU trade.

Citi FX Quants preliminary estimate of month-end FX hedge rebalancing flows point to a marginal need to sell USD against all major currencies except JPY by this Friday's fix.

Citi notes equities continued their gains at the start of 2021 while bond indices suffered losses. Although Citi expect foreign needs to hedge gains in U.S. equities will still dominate, likely USD buying by U.S. investors to hedge foreign equity gains and foreign fixed-income investors to reduce U.S. bond hedges largely neutralise the signal. That leaves it short of 0.5 historical standard deviations in all crosses except EUR/USD. The 0.6 standard deviation signal to buy EUR/USD is driven by weak performance of euro area assets, Citi says, which reduces non-European needs to sell EUR, allowing local rebalancing needs to dominate to a greater degree. On the other hand, low assumed hedge ratios among Japanese investors and good performance of Japanese assets tilt the signal for JPY to a sell against USD, suggesting that this month's strongest relative signal is to buy EUR/JPY.

G10 FX Options Expiries for 10AM New York Cut

EUR/USD: 1.2200-20(658M)

USD/JPY: 103.45-60 (595M), 103.80-95(560M)

EUR/GBP: 0.8900(705M)

AUD/NZD: 1.0665 (530M)

NZD/USD: 0.7050(645M), 0.7100 (254M)

----------------

Larger Option Pipeline

EUR/USD: Jan29 $1.2070-75(E1.0bln); Feb01 $1.2000(E1.5bln), $1.2220-30(E1.2bln-EUR puts); Feb02 $1.2150(E1.2bln-EUR puts)

USD/JPY: Feb05 Y103.00($1.0bln-USD puts)

USD/CHF: Jan29 Chf0.8800($1.46bln-USD puts)

AUD/USD: Feb02 $0.7600(A$1.1bln)

USD/CNY: Jan29 Cny6.50($1.5bln); Feb02 Cny6.55($1.1bln)

USD/MXN: Jan29 Mxn19.80($1.1bln), Mxn20.00($1.2bln); Feb04 Mxn20.50($1.5bln)

Source: DTCC

Technical & Trade Views

EURUSD Bias: Bearish below 1.2265 targeting 1.2050

EURUSD From a technical and trading perspective, failure below 1.22 opens a retest of bids to 1.2050, only a close back through 1.2265 would suggest a false downside break. Downside target achieved expect profit taking pullback to test offers at 1.2150/1.22. Potential reversal developing on the second test of bids towards 1.2050, daily close through 1.22 would be constructive for a move to retest 1.2350

Flow reports suggest downside bids into the 1.2050 area with increasing bids into the 1.2000 level with weak stops on any move through into the 1.1980 level with break out stops a possibility, Topside offers through the 1.2100 level light with the topside likely to remain weak through to the 1.2180 area before some stiffness appears through to the 1.2200 level with very little in stops until 1.2220 level and weak stops easily absorbed in stronger resistance.

GBPUSD Bias: Bullish above 1.35 targeting 1.3830/60

GBPUSD From a technical and trading perspective, as as 1.35 supports then prices can extend higher to test interim wave 5 upside objectives to 1.3830/60 area

Flow reports suggest topside offers through the 1.3750 area and increasing on any move towards the 1.3800 level weak stops on a break through opens up a larger rise with limited stops through the 1.3850 area but opening the 1.41/1.42 over time. Downside bids light through to the 1.3650 area and stronger bids currently being tested with weak stops likely on a dip through light for the moment and stronger bids into the 1.3600 level and increasing on any move to the 1.3550 area.

USDJPY Bias: Bearish below 104.50 targeting 101.20

USDJPY From a technical and trading perspective, as 104.20/50 contains upside attempts look for the next leg lower to target 101.20

Flow reports suggest topside offers into the 104.40-60 area with congestion likely to be light and then increasing on any move through the 104.80-105.20 area and weak stops above to push to the 105.50 and more congestion, downside bids light through to the 103.50 level with some bids building in the area with stronger bids moving through the 103.20-102.80 area with importers likely to be happy to buy in the area through to the 100 level before BoJ starts to comment.

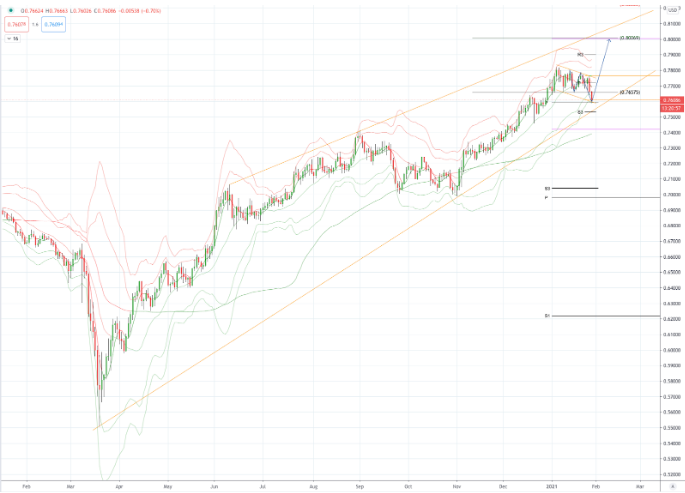

AUDUSD Bias: Bullish above .7600 bullish targeting .8000

AUDUSD From a technical and trading perspective, as .7600 now acts as support, look for target wave 5 upside objective towards .8000. Note .7800 is an interim measured move upside objective that may prompt a profit taking pullback before the uptrend resumes from.7450 trend support

Flow reports suggest bids likely just below the lows and through into the 0.7580 area before weak stops appear opening the market a little through to the 0.7550 area with stronger bids again and possibly continue through to the 0.7500 area. Topside offers light through the 77 cents level and likely to continue through to the 0.7750 with very little interference however beyond that level is likely to see stronger offers the closer the market gets to the 78 cents area and continuing through to the 0.7820 area before stops appear and open a higher move over the next couple of days.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 65% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!