Daily Market Outlook, July 1, 2022

Daily Market Outlook, July 1, 2022

Overnight Headlines

- US Stocks Suffer Sharpest First-Half Drop In More Than 50 Years

- Q2 Earnings Concerns Weigh On Risk Sentiment

- Bitcoin Pares Jump Amid Dip Buying In Hope Of Better Second Half

- Oil Heads For Worst Run Of Losses This Year On Recession Concern

- McConnell Threatens China Bill Over Biden Tax, Climate Plan

- ECB's Holzmann Says He Would Have Preferred Earlier Hikes

- UK’s No 10 Float’s Plans VAT Cut To Ease Pain Of Rising Prices

- China's June Factory Activity Expands At Fastest Pace In 13 Months

- China Announce $45Bln In Stimulus To Pay For Infrastructure

- Tokyo June Core Consumer Prices Rise At Fastest Pace In 7 Years

- Japan Manufacturers Turn Less Optimistic, Helping BoJ’s Case

- Japan's Factory Activity Growth Slows In June, Hurt By China Curbs

- Dollar Heads For Weekly Gain As Investors Weigh Rates, Recession Risks

- EU Says May Not Be Possible To Cross Finish Line On Iran Nuclear Deal

- Stocks Make Tentative Start To Second Half Under Growth Clouds

- Micron's Weak Outlook Sparks Concerns Of Chip Down Cycle

The Day Ahead

- Risk-off sentiment continued to prevail as global recession concerns weigh on equities, government bond yields and oil prices. The S&P 500 index In the US fell by more than 20% in the first half of the year, the most since 1970. Stock markets are lower overnight across most markets in Asia. In Japan, the closely watched Tankan report revealed weaker-than-expected confidence in Q2 among large manufacturers. China’s Caixin manufacturing PMI, however, returned to growth territory at 51.7 in June, up from 48.1 in May.

- This morning’s Eurozone and UK June manufacturing PMIs are final estimates, although we will get the first readings for Italy and Spain. The final PMIs are expected to confirm earlier flash estimates. The Eurozone survey was particularly weak with the composite index dropping to 51.9 in June, the weakest since early 2021, reflecting contraction in manufacturing and fading pent-up demand for services. In the UK, the composite PMI held steady at 53.1, but is significantly lower than in the first four months of the year, and the future output index points to further losses of momentum in the coming twelve months. Inflationary pressures remained elevated, but the price indices hinted at near-term peaks.

- Eurozone flash CPI inflation estimate for June is also out this morning. Look for an increase in annual headline CPI to a new high of 8.5%, up from 8.1% in May, driven by further rises in food and energy as well as an uptick in core inflation to 3.9% from 3.8%. National data this week showed a surprising fall in German EU-harmonised inflation to 8.2% offset by a surge in Spain to 10.0%, while France was in line with forecasts at 6.5%. Such a print for the Eurozone would likely be seen as reaffirming the ECB’s signal that it will raise interest rates by 25bp in July and boost market expectations of a larger 50bp increase in September.

- UK money and credit figures from the Bank of England are expected to show mortgage approvals falling to 64k in May, down from 86k a year earlier. Data for consumer credit will also be watched, particularly credit card borrowing which has risen by more than 10% compared with a year ago.

- Ahead of Monday’s holiday, the US focus will be on construction spending and the ISM manufacturing survey. Expect construction spending for May to rise by 0.4% and the ISM manufacturing index to fall to 55.5 in June from 56.1 in May. The declines in the S&P Global (IHS Markit) manufacturing PMI to 52.4 and in the regional Philadelphia Fed survey may point to downside risks for the ISM report.

FX Options Expiring 10am New York Cut

- EUR/USD: 1.0400-05 (937M), 1.0425 (287M), 1.0450 (521M)

- 1.0475-80 (914M), 1.0500-05 (454M), 1.0520-25 (363M)

- 1.0540-55 (2.0BLN), 1.0565-75 (2.6BLN)

- 1.0590-00 (2.53BLN), 1.0615 (611M), 1.0630 (994M)

- USD/JPY: 133.50 (1.47BLN), 134.00 (1.58M), 135.25 (295M)

- 135.50 (571M)

- GBP/USD: 1.2000 (408M), 1.2100 (259M), 1.2150 (222M)

- 1.2200 (248M). EUR/GBP: 0.8600 (329M), 0.8635-40 (276M)

- USD/CHF: 0.9450 (750M). 0.9650-60 (450M)

- AUD/USD: 0.6800 (754M), 0.6900-10 (816M), 0.6950 (337M)

- 0.7000 (400M), 0.7050 (1.96BLN). NZD/USD: 0.6400 (1.153BLN)

- AUD/NZD 1.1100 (348M). USD/ZAR: 16.0175 (590M)

Technical & Trade Views

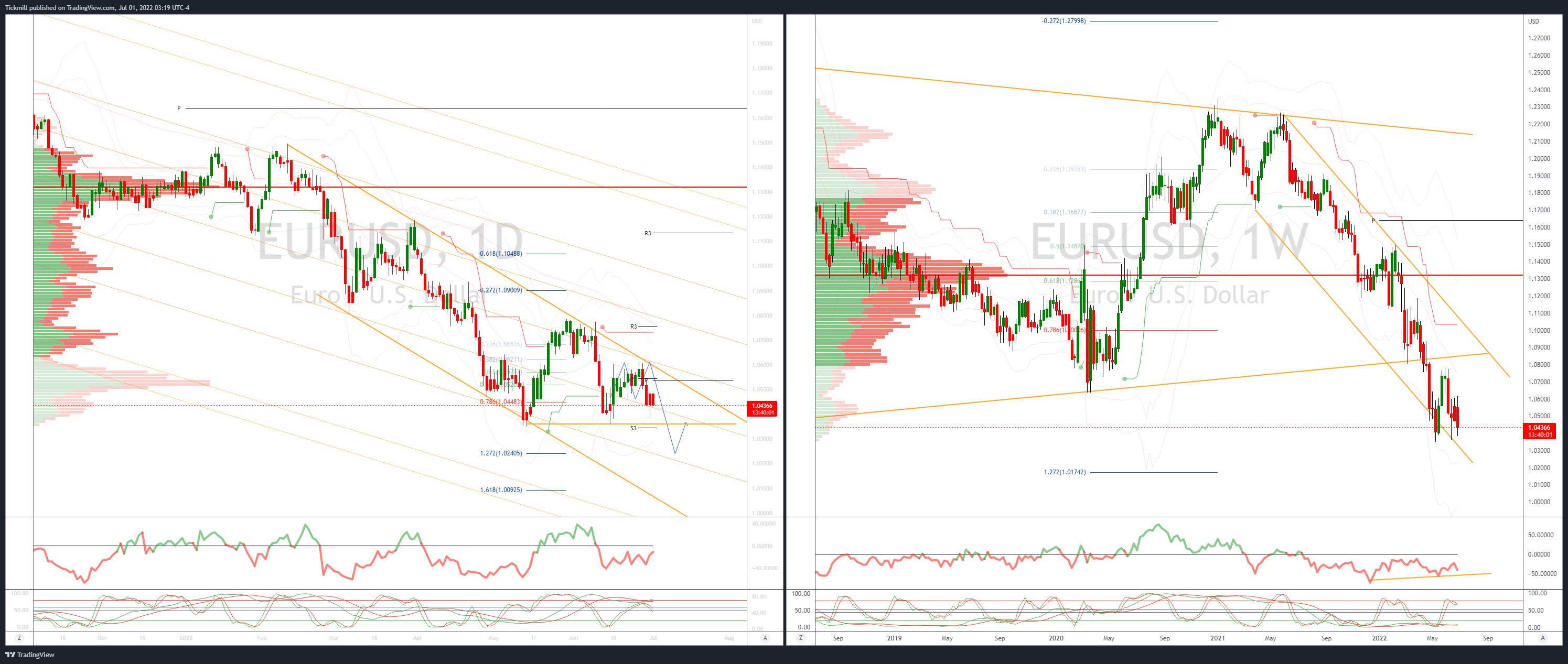

EURUSD Bias: Bearish below 1.07 Bullish above

- EUR recovery attempt supported by a pullback in US yields and quarter-end flows

- Overnight Eminis retreat 1% in risk off Asian trade, EURJPY flows weigh

- The hurdle for nascent bulls sits at 1.0530/60

- Technical descending triangle forming break should give directional drive

- Failure below the base opens a test of 1.0270’s next

- Initial offers are seen at 1.0615/20 ahead 1.0650

- Bids 1.0450 stops below to fuel a test of 1.04

- 20 Day VWAP is bearish, 5 Day bearish

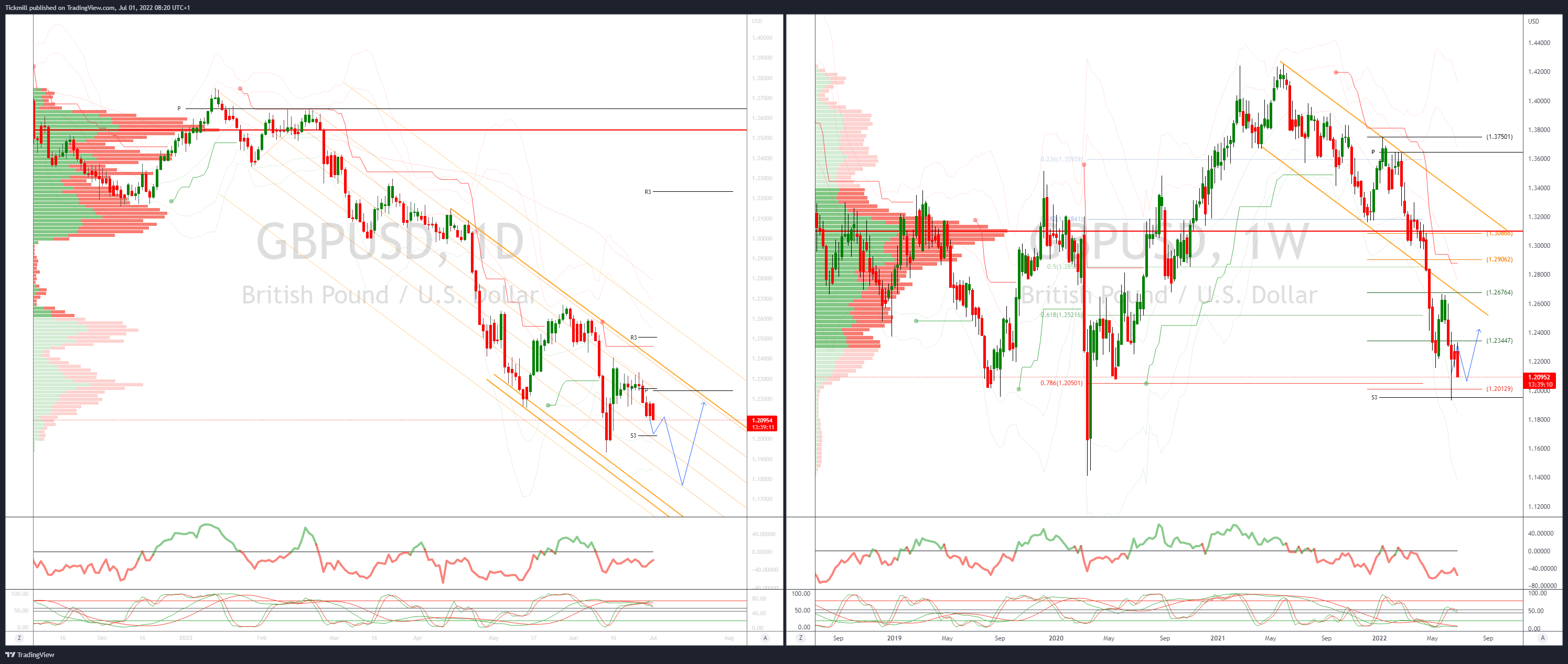

GBPUSD Bias: Bearish below 1.26 Bullish above.

- GBP offered in Asian trade GBPJPY flow weighs on Cable

- BoE dovish tilt and Brexit concerns also seen as adding pressure

- Markets sense BoE may fall behind the curve in a similar fashion to the ECB

- Bears targeting a break of YTD lows en-route to a test of 1.18

- Resistance remains sited at 1.2410

- 1.2150 failure will open a test of bids at 1.2050

- 20 Day VWAP is bearish, 5 Day bearish

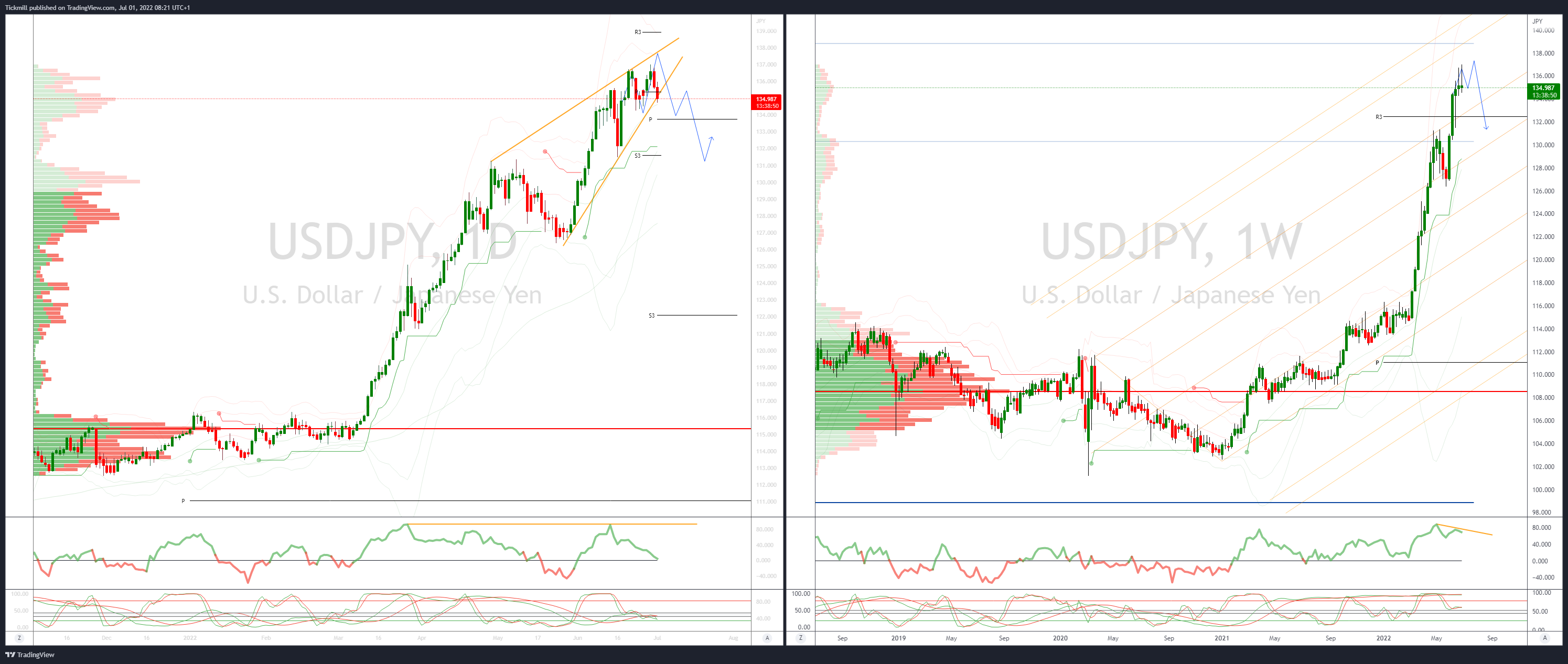

USDJPY Bias: Bullish above 132 Bearish below

- USD/JPY continues to retreat with lower US yields

- US yields soften on recession fears, 10 yr Treasury trading 2.96%

- US 10yr sub 3% sees JPY inflows with a reversal in global risk sentiment

- Japanese importer bids sited towards 135 eroded, carry buyers seen in wait towards 1.34

- Notable options expiries at 133.50 and 134.00 strikes go off today

- Option barriers KO’s quoted at 137 remain intact

- 20 Day VWAP is bullish, 5 Day bullish

AUDUSD Bias: Bullish above .7200 Bearish below

- AUD mints new 2022 lows

- Bears target a test of the equality objective at .6640’s

- Commodities roll over in Asia Iron Ore very soft towards a 5% loss, Copper also weak

- Bids are tipped toward .6750

- 20 Day VWAP remains untested confirming downside

- Offers seen towards .69

- 20 Day VWAP is bearish, 5 Day bearish

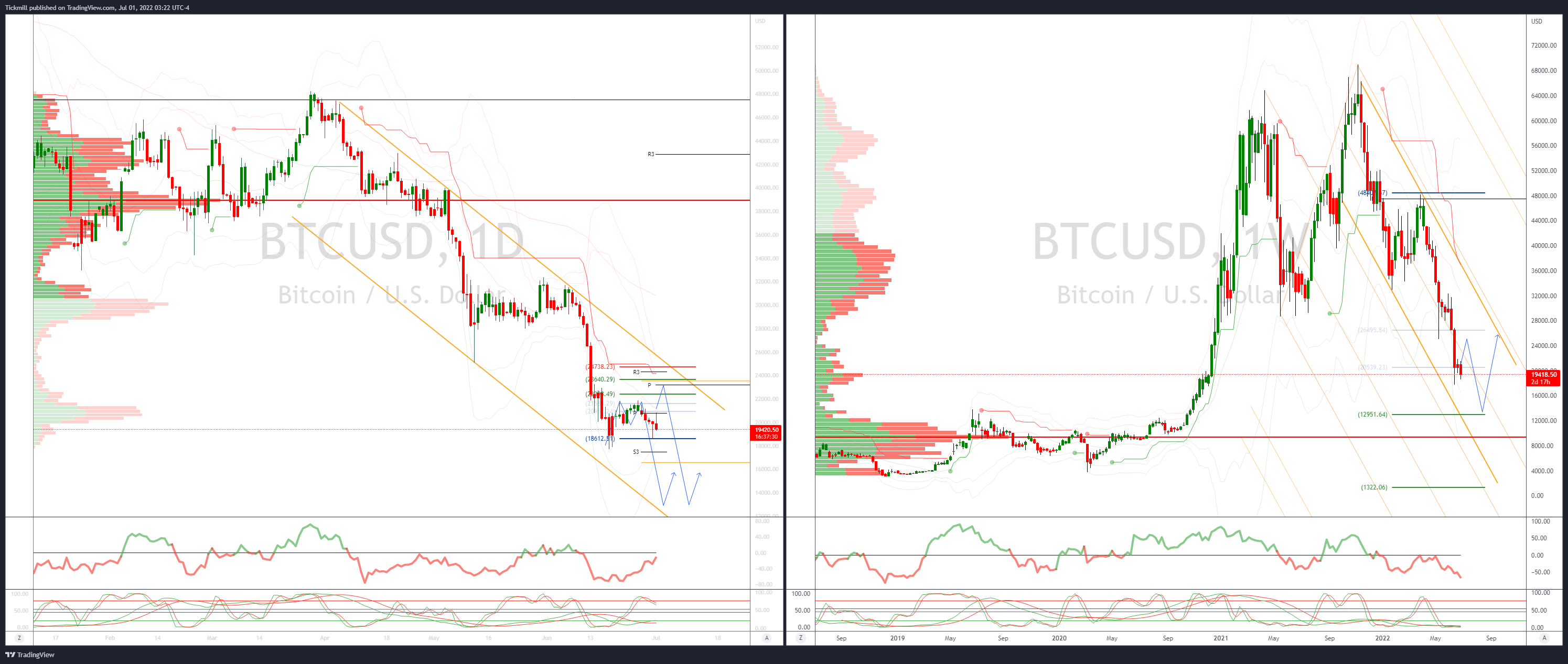

BTCUSD Bias: Bullish above .22000 Bearish below

- BTC sinks below 20k again after late pop higher yesterday gaining 4.9%

- Failure to gain traction above 21K leaves dip buyers second-guessing fresh bids

- Trend remains down as within broader bearish channel beckons

- Support seen at 19k then 18300 the base of the daily VWAP bands failure here opens a retest of lows

- 20 Day VWAP remains bearishly oriented and untested

- Additional pressure seen from BTC miners liquidating positions on declining profitability

- 20 Day VWAP is bearish, 5 Day bearish

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!