Daily Market Outlook, June 24, 2022

Daily Market Outlook, June 24, 2022

Overnight Headlines

- Asian Equity Markets Broadly Higher; US And EU Futures Also Rise

- UK Conservatives Lose Key District In Major Blow To PM Johnson

- UK Consumer Confidence Falls To Lowest Since Records Began

- Powell Hammers Home Unconditional’ Commitment To Cool Prices

- Fed’s Bowman Backs Raising Funds Rate By 75 Basis Points In July

- US Banks Ace Fed Stress Tests, Pave Way For Shareholder Payouts

- US Meets With Refiners On High Pump Prices But No Plan Yet

- EU Leaders Vote To Grant Ukraine And Moldova Candidate Status

- ECB’s Kazimir: The ECB Rate May Be At 1.5-2.0% In A Years’ Time

- China Central Bank Raises Cash Injection To Keep Liquidity Stable

- Japanese Consumer Inflation Tops BoJ Target For Second Month

- OPEC+ To Stick To Oil Supply Rise Plan As Biden Heads To Saudi

- US Dollar Stumbles As Interest Rate Path Fuels Recession Worries

- Bitcoin Rangebound Remains Above Recently Reclaimed 20,000 level

The Day Ahead

- Asian equity markets chalked up gains as US Treasury yields fall with attention appearing to be shifting towards the loss of economic momentum and a potential near-term peak in inflation. While US policy rates are expected to rise significantly further this year, market pricing currently points to rate cuts around the middle of next year.

- In the UK, data released overnight showed consumer confidence in the GfK survey fall to an all-time low of -41 in June, weighed by the squeeze on incomes from high inflation. Meanwhile, the Conservatives lost both by elections in Wakefield and in Tiverton and Honiton. Party Chairman Oliver Dowden resigned.

- Just released official UK data showed the volume of retail sales decline by 0.5% in May while the previous month’s rise was revised lower. Sales volumes fell in predominantly food stores, linked to higher prices, and were flat in other (non-food) stores. In the year-on-year comparison, the volume of sales fell by 4.7%. However, in nominal terms (actual pounds spent), retail sales were up 5.0%. That suggests high inflation is resulting in consumers paying more for less goods.

- The German IFO survey of businesses will be released this morning. It has so far shown some degree of resilience in the economy in the face of supply bottlenecks, rising costs and the war in Ukraine. Nevertheless, confidence fell sharply in March and, despite slight rises in April and May, it remains below levels at the start of the year and is consistent with a slowdown in economic activity. For June, anticipate the headline index to remain steady at 93.0. It is worth noting that yesterday’s flash PMIs for Germany were weaker.

- In the US, latest data for new home sales will attract some attention, particularly as higher interest rates cool the housing market. Also due is the final reading of the University of Michigan consumer sentiment survey. The preliminary reading showed sentiment falling to an all-time low of 50.2, while longer-term inflation expectations rose to a 14-year high.

- On the central bank speaker front, the Bank of England’s Chief Economist Pill and external MPC member Haskel will speak at separate events this afternoon. Pill’s speech on ‘Challenges for Monetary Policy after Covid-19’ may attract particular attention. US Fed speakers include St Louis Fed President Bullard (voter) on central banks and inflation.

FX Options Expiring 10am New York Cut

- EUR/USD: 1.0400 (670M), 1.0420-30 (674M), 1.0450 (574M)

- 1.0495-00 (1.15BLN), 1.0520-30 (365M), 1.0575 (275M)

- 1.0600 (483M), 10660 (560M)

- USD/CHF: 0.9600 (240M), 0.9700 (540M). AUD/JPY: 95.60 (407M)

- AUD/USD: 0.6900 (923M), 0.6980 (229M), 0.7000 (290M)

- USD/CAD: 1.2850 (390M), 1.2900 (230M), 1.2950 (400M)

Technical & Trade Views

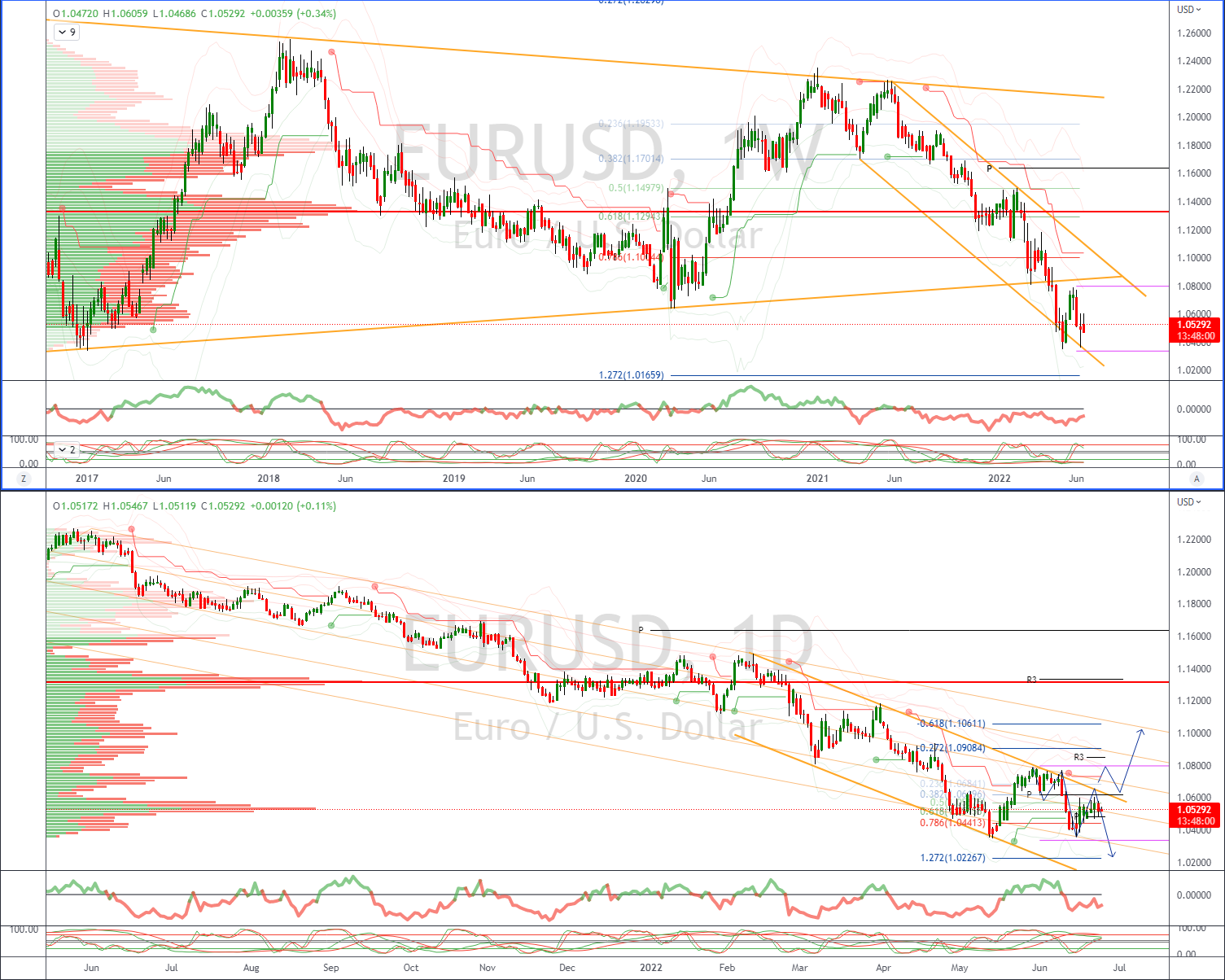

EURUSD Bias: Bearish below 1.07 Bullish above

- EUR/USD trades in a subdued fashion as PMI data continues to weigh

- Support coming from slower Asian session and bid in risk sentiment

- Bulls to challenge 1.06 into the end of the week adding support to daily double bottom

- German IFO main release of note and will likely drive sentiment short term

- Initial offers are seen at 1.0560 ahead 1.0615

- Bids eyed towards 1.0450/70 ahead of cycle lows

- 20 Day VWAP is bearish, 5 Day bullish

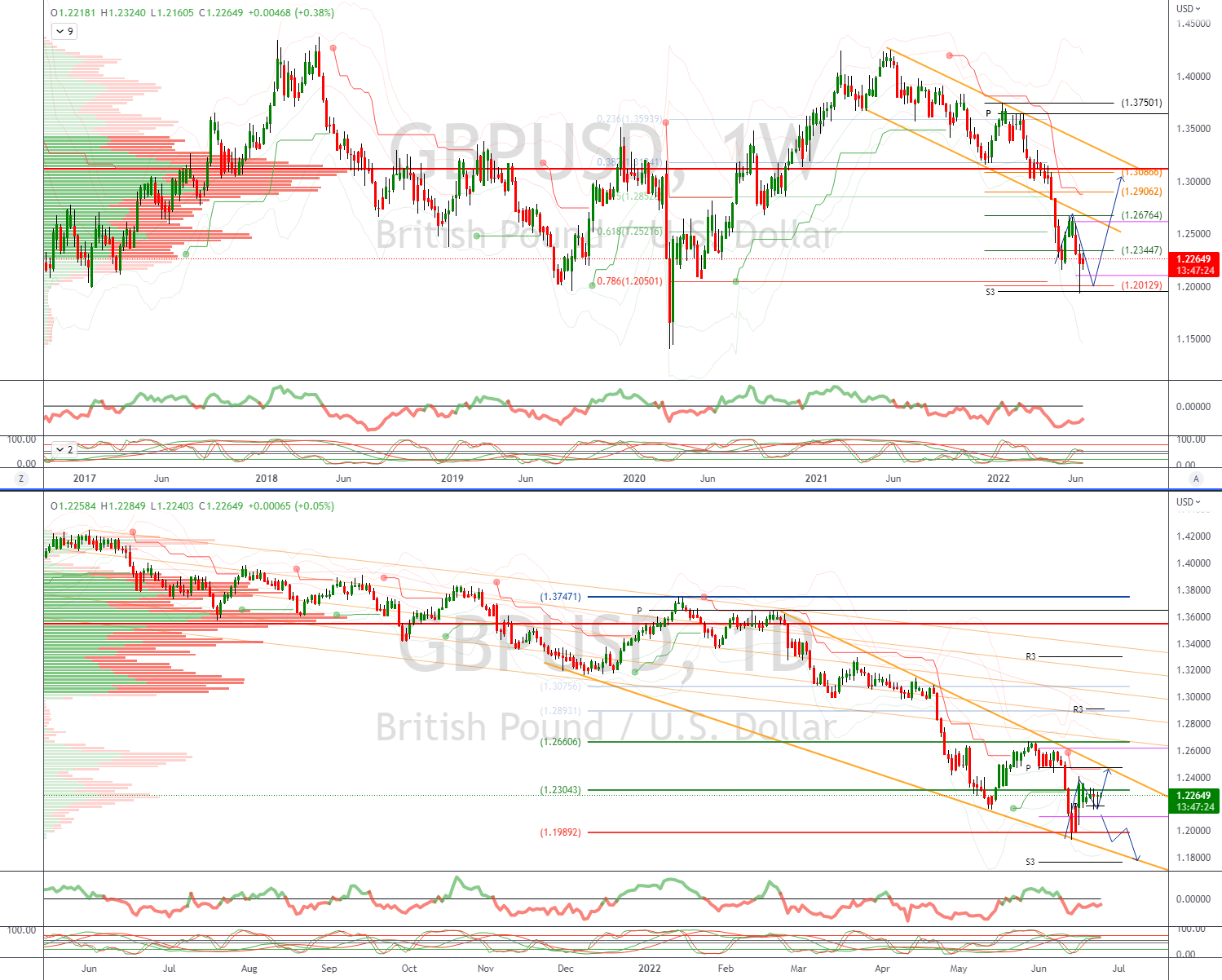

GBPUSD Bias: Bearish below 1.26 Bullish above.

- GBP continues to trade in a tight range, election news does little to excite the market

- Despite ongoing negative headlines, weak econ data, strikes & partygate GBP holds up

- Trading should pick up as LDN session starts, traders likely to square books into W/end

- Resistance remains sited at 1.2410

- Support eyed at 1.2180

- 20 Day VWAP is bearish, 5 Day bullish

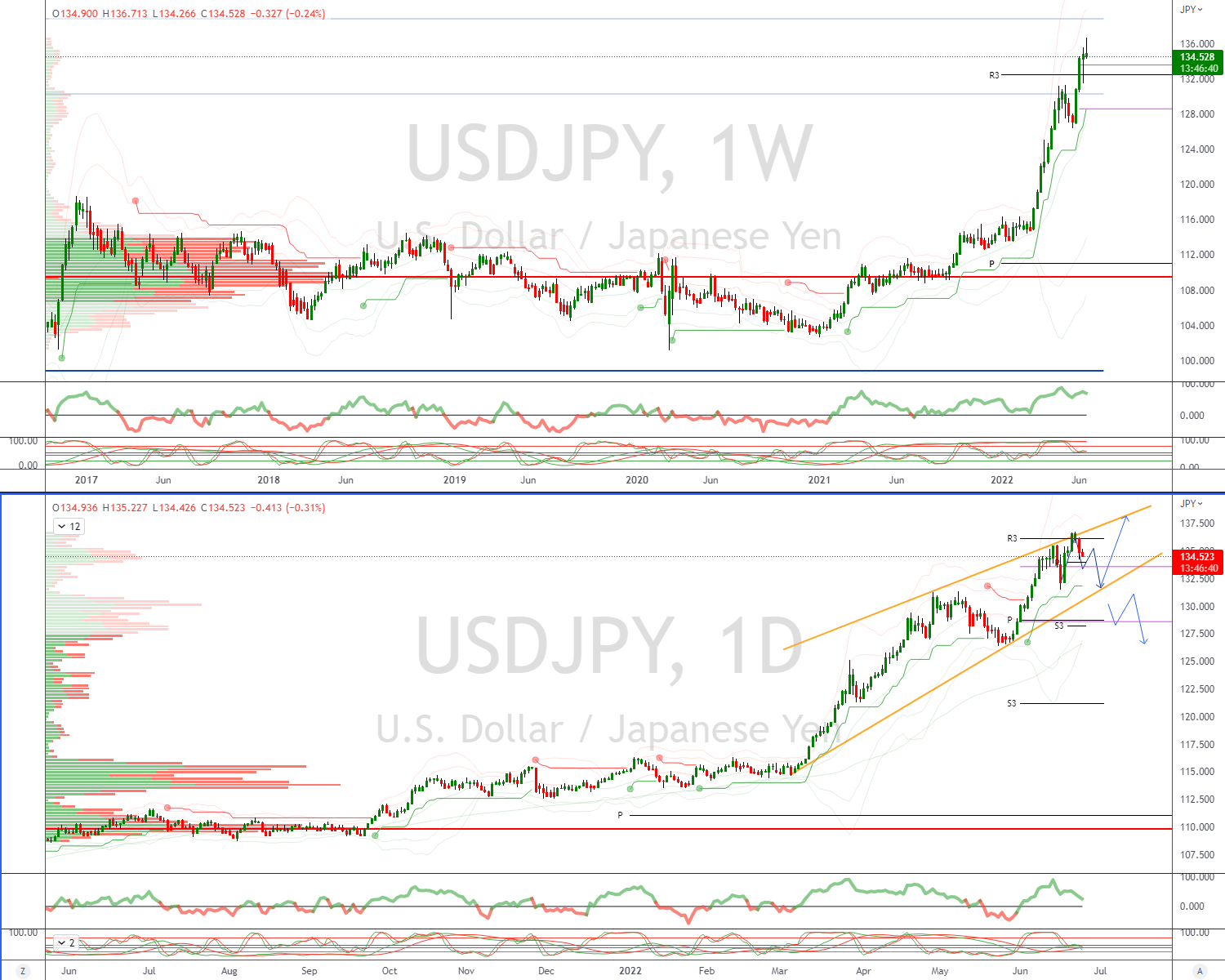

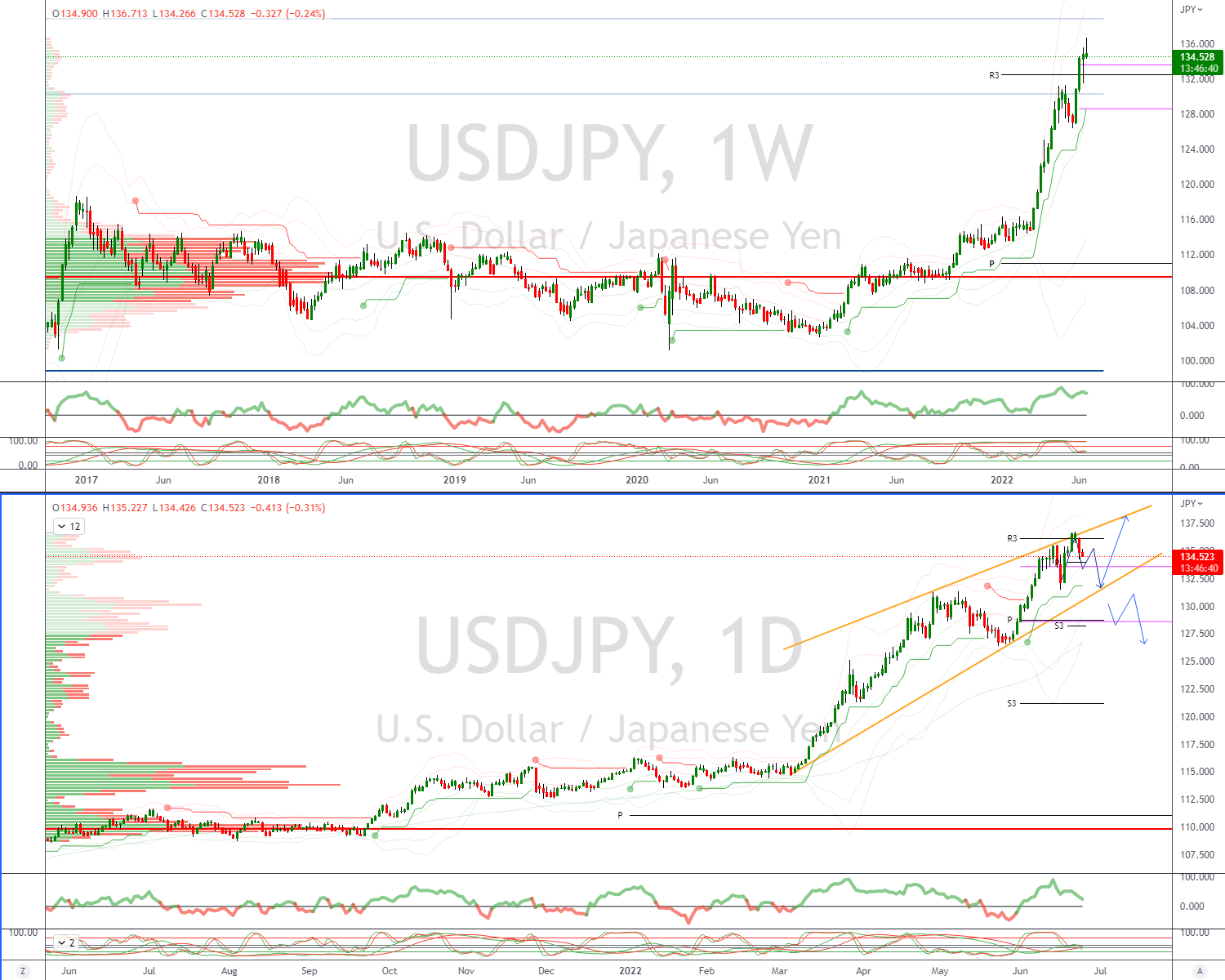

USDJPY Bias: Bullish above 132 Bearish below

- JPY retains broad-based bid

- USD/JPY offered as LDN session gets underway

- Giving back gains after Gotobi Tokyo fix bids have been absorbed

- Japanese importer bids seen below 134.50

- DTTC option expiries Monday 134.50, 135.00 strikes

- US yields off lows but retain an offered tone

- Global equity sentiment improves overnight

- 20 Day VWAP is bullish, 5 Day bearish

AUDUSD Bias: Bullish above .7200 Bearish below

- Rotates around 0.6900 in slower Asian session

- Soft commodities continue to weigh

- Near term resistance site at .6950/60

- How commodities close out the week will likely drive AUD action

- 20 Day VWAP remains untested confirming downside

- Bears now targeting a test of the base towards 0.6840’s

- Offers seen towards .6960, bids eyed back at .6850

- 20 Day VWAP is bearish, 5 Day bearish

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!