Daily Market Outlook, November 19, 2020

.png)

Daily Market Outlook, November 19, 2020

Asia equity markets were mixed, as concerns about the impact of rising Covid-19 infections offset Pfizer’s upgrading of its vaccine effectiveness to 95%. The Oxford/AstraZeneca vaccine also reported positive results in early phase-two trials. Japan recorded a sharp rise in coronavirus cases and Tokyo’s virus alert was raised to the highest level. In the US, Covid-related deaths exceeded 250k and New York City announced the closure of schools from today. In the UK, the government announced a boost to defence spending over the next four years, ahead of next week’s Spending Review. The UK and Canada are also reportedly on the brink of agreeing a new trade deal.

President Lagarde kicks off the day at a European Parliament hearing before the Economic and Monetary Affairs Committee at 8am. The ECB has indicated that it is set to ‘recalibrate’ policy at the next meeting in December in response to the resurgence in Covid-19 cases across Europe and the likely stalling of the economic recovery. Ms Lagarde said that the ECB is likely to ease policy via the pandemic emergency purchase programme and long-term refinancing operations. It will be interesting to hear her views on to what extent the recent coronavirus vaccine news has altered the economic assessment. She may also urge the rollout of the €750bn EU recovery fund, which requires unanimity among the member states, and has been blocked by Hungary and Poland because of rule-of-law conditions attached.

The afternoon focus will be on US weekly jobless claims and the Philadelphia Fed survey. Initial claims are expected to remain elevated, look for a slight fall to 705k from 709k in the prior week. For the Philly Fed survey, look for a pullback to 25.0 in November after last month’s strong result. Overall, US economic growth has slowed but has still outperformed expectations.

In the UK, the CBI will release an update of its monthly industrial trends survey this morning, with the total orders balance seen falling to -40 in November from -34. More attention is likely to be on October retail sales figures, which will be released at 7am tomorrow. The update will cover the period before lockdown in England. After several months of strong returns, look for a modest 0.2% fall for October (ex-fuel). More timely is the UK November GfK consumer confidence survey due in the early hours of tomorrow. It will capture the first two weeks of the month and will reflect the impact of England moving back into lockdown, but it may be too early to show a positive impact from vaccine hopes. We look for a drop to -34 from -31 previously

Today’s Options Expiries for 10AM New York Cut

- EURUSD: 1.1850-60 (850M), 1.1870-75 (700M), 1.1885 (360M), 1.1900 (873M)

- GBPUSD: 1.2995 (240M), 1.3400 (570M)

- EURGBP: 0.8900 (645M), 0.8925 (733M),0.8960 (244M), 0.9035 (200M)

- USDJPY: 103.25 (455M), 103.50-55 (400M), 104.25-35 (1.1BLN), 104.50-60 (1.6BLN)

- AUDUSD: 0.7225-35 (350M), 0.7250 (321M)

Technical & Trade Views

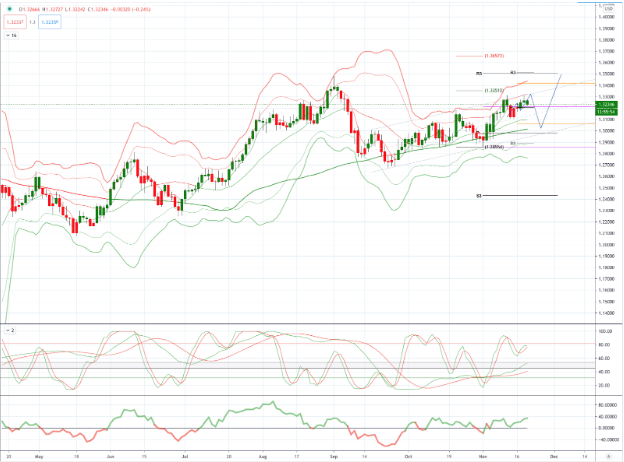

EURUSD Bias: Bullish above 1.1750 targeting 1.20

EURUSD From a technical and trading perspective, as 1.1750 acts a support look for a retest of cycle highs at 1.20, failure below 1.1750 opens a retest of range support at 1.16

Flow reports suggest topside offers through to the 1.1920 level, even there where you’re likely to see weak stops you will find the same type of congestion continuing to the 1.1950 before weakening a little and increasing for any move to the 1.2000 level. Downside bids light through the 1.1800 area with weak stops on a dip through the 1.1780 area and opens the market for a renewed challenge of the 1.1700 area with light support from there.

GBPUSD Bias: Bullish above 1.3150 targeting 1.3480

GBPUSD From a technical and trading perspective, as 1.3150 supports look for a test of prior cycle highs at 1.3480

Flow reports suggest offers into the 1.3300 level are likely to be a little light with limited congestion through to the 1.3400 level before stronger offers start to appear with weak stops on a break through the level to open the 1.3500 level for a second test of the year. Downside bids light back through the 1.3200 level with congestion forming around the 1.3150 and stronger to the 1.3100 level, weak stops on a move through the area and nothing special until the 1.3000 one suspects

USDJPY Bias: Bearish below 104 bullish above

USDJPY From a technical and trading perspective, look for another tet of 103.20 projected ascending trendline support, another hold here could prompt near term short covering to challenge offers to 105 descending trendline resistance

Flow reports suggest downside bids into the 104.00 level increasing on move through the 103.50 level with weak stops likely on a dip through the 103.00 area with the stops likely to increase through 102.80, topside offers likely to increase through to the 106.00 area with weak stops through the 106.20 area and increasing congestion on a push above the 106.50 level and into the 107.00

AUDUSD Bias: Bearish below .7243 bullish above targeting .7400

AUDUSD From a technical and trading perspective, as .7240/20 now acts as support look for a retest of offers and stops above .7400

Flow reports suggest downside bids cleared through to the 0.7260 level yesterday but reforming with stronger bids likely through to the 0.7240 area, a move through the level is likely to see limited bids into the 0.7200 area with weak stops appearing on a move through the 0.7180 area opening a deeper move over several days to the 70 cents level. Topside offers through the 0.7350 area likely to continue to be strong with increasing offers beyond the 0.7380 area through to the 0.7410-20 level before stops appear however, offers around the 0.7450 area likely to increase beyond the level

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72% and 75% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!