Daily Market Outlook, October 18th, 2021

-1634552475.png)

Daily Market Outlook, October 18th, 2021

Overnight Headlines

- US Democrats Face A Deadline On Benefits And Climate Bill Consensus

- Senator Johnson Hoping For 'Gridlock' On The Reconciliation Package

- ECB Considers Boosting Purchases Of EU Recovery Fund Debt: FT Sources

- ECB’s Knot Sees Rates Edging Up As Stimulus Programs Are Curtailed

- German Greens Vote To Start Formal Coalition Talks With SPD, Liberals

- BoE Governor Bailey: Bank Of England Will Have To Act To Contain Inflation

- China Q3 GDP Growth Hits One-Year Low, Raising Heat On Policymakers

- New Zealand CPI Surges To Fastest Pace In Ten Years; Kiwi Dollar Jumps

- Australian Bond Yields Surge With New Zealand’s As Rate-Hike Bets Rise

- Oil Climbs To Highest In Years On Covid Recovery And Power Generators

- Asian Equity Markets Mostly Lower; Chinese Property Shares Firm

The Day Ahead

- Most Asian equity markets are trading lower following the release of weaker-than-expected Q3 GDP data from China. The economy expanded by just 0.2% in the third quarter as tighter restrictions on the property sector and September’s energy shortages weighed on activity. In particular, the rate of annual industrial production growth eased to 3.1% in September from 5.3% in August as the energy shortage resulted in factories either shutting down or reducing their output.

- Over the weekend, Bank of England Governor Bailey continued to reiterate that the recent acceleration in UK inflation will prove temporary, albeit rising energy prices means that inflation will rise further and stay elevated for longer. However, he also noted that he would act to prevent higher inflation from becoming entrenched through higher inflation expectations.

- Prospects of slower global growth and more persistent high inflation remain at the forefront of investors’ minds. The global economic outlook remains uncertain, with risks predominantly related to the pandemic impact on demand/supply mismatches in goods and labour markets, and policy responses from governments and central banks. Later this week, global ‘flash’ PMIs for October will provide an early indication of activity and price pressures at the start of Q4. Overall, the surveys are expected to indicate continued expansion, but with supply constraints contributing to a further softening in momentum.

- Last week’s release of the September FOMC minutes highlighted elevated uncertainty over the inflation outlook and the extent to which supply chain pressures would continue to persist. Today’s US industrial production release for September are expected to show the impact of going supply chain constraints, with growth expected to post its slowest rate since April. Industrial outages linked to Hurricane Ida are also expected to have weighed on activity.

- US housebuilders’ sentiment is also expected to have slid this month as rising material costs and shortages of labour continue to weigh on confidence. The October NAHB survey is forecast to dip to 75 from 76.

- In terms of central bank speakers, Fed members Quarles and Kashkari speak at separate events today, though neither are expected to focus on the near-term outlook for US monetary policy. In the UK, Bank of England Deputy Governor Jon Cunliffe speaks at a Bank of Spain event on “Central Bank Digital Currencies and Financial Stability”

The Week Ahead

- China growth and global inflation data in focus While China's Q3 GDP dominates this week’s calendar of key data, global inflation indicators will also remain in focus amid continuing supply constraints. Chinese GDP grew 4.9% year-on-year, well below the 7.9% rise in Q2, and versus a 5.2% poll forecast. September industrial production also disappointed, rising 3.1% against a 4.5% forecast, but retail sales outperformed with growth of 4.4% versus the 3.3% forecast. Chinese house prices and the monthly Loan Prime Rate setting are due later this week. U.S. data includes IP, housing starts, building permits, existing home sales, the Philly Fed index and Markit flash PMIs. Euro zone flash PMIs and consumer confidence will be released this week, but the focus will be on inflation data as Germany reports producer prices and the EZ will release final September HICP inflation. The UK will be in the spotlight, as a raft of inflation data could fuel already hawkish Bank of England expectations. September CPI, PPI and RPI are due this week, while retail sales and flash PMIs round off a busy UK calendar. Japan's nationwide CPI will be released, along with trade data and flash manufacturing PMI. There is no key data due from Australia this week, while New Zealand released much hotter-than-expected Q3 CPI early Monday. Canada's data highlights are house starts, CPI and retail sales.

- U.S. earnings, Biden stimulus plan watched Risk assets moved higher last week, largely due to very strong earnings reports from the U.S. banking sector. Earnings season kicks into high gear this week, with Netflix, Tesla, Procter & Gamble and Intel among the dozens of companies reporting. The fate of U.S. President Joe Biden's spending package still hangs in the balance, as two moderate Democrat Senators want to reduce the size of the package, while progressive Democrat Senators on the left want to maintain the $3.5 trillion price tag. Progress towards passing the spending bill is further complicated by the impasse between U.S. Republicans and Democrats on agreeing to raise the debt ceiling. The markets have largely priced in the economic benefits of a U.S. spending plan, so there will be disappointment if one isn't passed.

CFTC Data

- Speculative accounts sat back and consolidated positioning over the course of the past week, following the sharp increase in aggregate USD long position seen in early October. The trend reflected price action in the spot market over the past few days, with profit taking and position squaring dominating trading. Overall data show very little change in net exposure to the USD, however investors are sticking with USD longs by and large. Data compilation shows the aggregate USD long down USD335mn this week to a still elevated USD22.9bn.

- The JPY saw a further increase in net shorts, however, with investors adding USD1.2bn to the bearish JPY position, taking it to USD8.4bn. This equates to 76.6k contracts in net short positioning, the most bearish speculative sentiment since mid-2019. Speculators added lightly to net CAD shorts (up USD99mn) and net MXN shorts by an even lighter USD89mn.

- Meanwhile, investors moved to cover some shorts in the GBP (cut USD688mn), the EUR (down USD586mn) and the CHF (USD370mn lower). Investors also pared record net AUD shorts but so marginally that it barely makes a difference. Net AUD shorts were cut USD122mn; the remaining net AUD short of USD6.4bn is substantial and the second largest single currency exposure for speculative investors.

- The NZD is the only currency reflecting any degree of bullish sentiment; speculators hold a modest (USD606mn) net long and added a marginal USD45mn to that total this week, likely reflecting the RBNZ starting its interest rate tightening cycle at the start of the month.

G10 FX Options Expiries for 10AM New York Cut

(Hedging effect can often draw spot toward strikes pre expiry if nearby (P) Puts (C) Calls )

- USDJPY - 113.90/114.10 458m. 113.60/70 486m. 113.00/10 430m. 112.50/60 713m. 110.00 720m

- EURUSD - 1.1840/50 750m. 1.1760/80 592m. 1.1650 551m. 1.1610/20 450m. 1.1600 652m. 1.1570/80 586m. 1.1520 644m.

- GBPUSD - 1.3760/70 431m.

- AUDUSD - 0.7600 620m. 0.7420 640m. 0.7240/50 482m.

- NZDUSD - 0.7050/70 613m.

- USDCAD - 1.2450 740m.

- USDMXN - 20.71 409m. 20.70 495m. 20.50 549m.

- USDCNH - 6.65 464m. 6.55 465m. 6.51 683m. 6.47 727m

Technical & Trade Views

EURUSD Bias: Bearish below 1.17 Bullish above

- EUR/USD consolidating in lower-half 20-day Bollinger bands 1.1493-1.1619

- Today's range 1.1574-1.1602 EBS, last week's high 1.1622, low 1.1522

- EUR 650mln expiries at 1.1600 today, EUR 600mln at 1.1575-80 and 1.1525

- EUR/USD bets little changed with traders holding a small net shortIMM/FX

- U.S. manufacturing and IP data at 13.15GMT, EZ final Sep HICP data Oct 20

- Low vol weighs neg yield EUR, energy costs up, EZ imports EUR negative

- EUR/USD options retain a downside risk premium which can cheapen protection

- 1-month 25 delta risk reversals 0.25, 3-month 0.325 (peaked 0.4 last week)

- 2-month date in demand since capturing Dec Fed and ECB policy announcements

- Hedge to sell EUR/USD at 1.1500 in 2-months (Dec 16) costs $64-pips

- Add a 1.1300 KO barrier to that and premium reduced to just $10-pips

- Profit potential on former unlimited, but latter option dead if 1.13 trades

- Would suits those looking for limited losses below 1.1500

- Expiry and barrier can be adjusted - less time, lower barrier raises cost

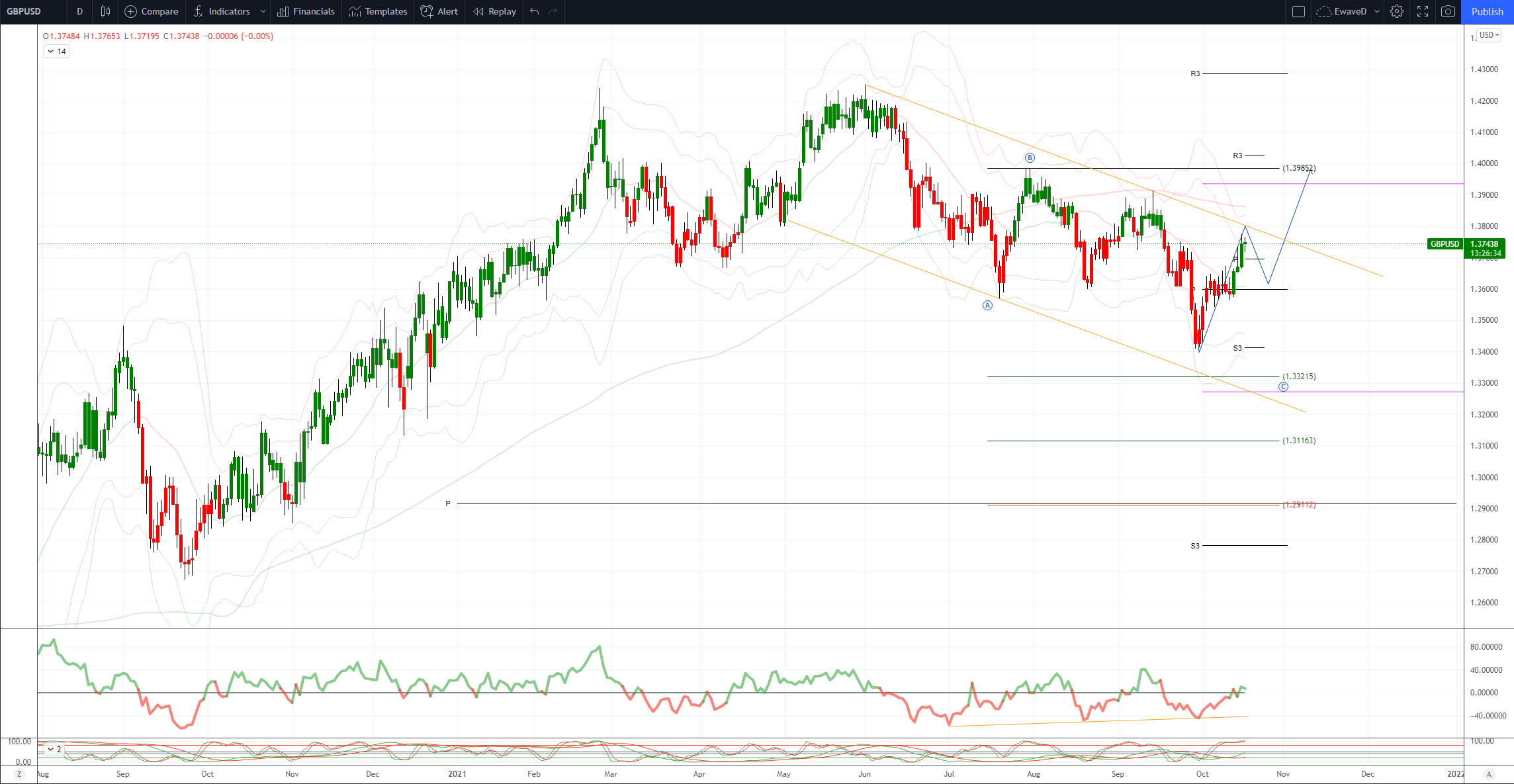

GBPUSD Bias: Bearish below 1.37 Bullish above.

- GBP/USD retreats from hawkish Bailey – spurred high

- Cable eases to 1.3721 (intra-day low) as higher UST yields support USD

- 10-year UST yield circa 1.60%, following Friday's rise

- 1.3765 was GBP/USD high in Asia, following hawkish Bailey comments on Sunday

- Bailey sent a fresh signal that BoE is gearing up to raise interest rates

- 1.3765 was eight pips shy of Friday's four-week peak

- Bids may emerge around 1.3700 (ex-resistance level) if cable extends south

USDJPY Bias: Bullish above 111.50 Bearish below

- USD/JPY and JPY crosses retraced down a bit but downsides limited

- JPY bias remains down however, plenty sellers on any rallies

- USD/JPY 114.35 to 114.02 before bouncing to 114.45, high Fri 114.47 EBS

- Good bidding interest down to 114.00, below, Japanese importers, others

- Importers looking to buy with option barriers at 113.00, 114.00 taken out

- 115 seen even bigger level for option barriers, break above very bullish

- Option expiries today supportive, 113.50-114.00 total $934 mln

- US yields firm despite flatter curve, Treasury 10s firm @1.607%

AUDUSD Bias: Bearish below 0.75 Bullish above

- Slightly lower after early rally fizzles out

- AUD/USD opened 0.7419 and moved up to 0.7438 in early trading

- It was dragged higher by spike up in NZD/USD after hot NZ CPI

- Light AUD/JPY selling helped to cap AUD/USD and send it down to 0.7410/20

- There was no reaction to China GDP miss and it remained in the 0.7410/20 window...

- Heading into the afternoon the AUD/USD is steady around 0.7410

- Resistance has formed at 0.7435/40 ahead of trend high at 0.7477

- Support is at Friday's low at 0.7404 and 10-day MA at 0.7350

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!