Daily Market Outlook, September 24th, 2021

.png)

Daily Market Outlook, September 24th, 2021

Overnight Headlines

- Biden Admin Preparing For Possible Government Shutdown

- Pelosi Vows Avert Shutdown, GOP Opposes Debt-Limit Link

- White House Weigh Invoking Defence Law To Get Chip Info

- House Dems To Vote Saturday To Advance Tax, Spend Plan

- China Maintain Liquidity Support, Evergrande Woes Persist

- Evergrande Bondholders Await News On Interest Payment

- Japan Ruling Party Race Put Abenomics Legacy In Focus

- Japan’s CPI Halts 12-Month Decline, Still Well Below Target

- IMF Urges Australia To Use Curbs To Cool Red-Hot Housing

- EU Confirms Inaugural US Trade-Tech Summit To Go Ahead

- UK Conservatives Fear Voter Backlash On Rising Living Cost

- UK Confidence Falls, Consumers Brace For Income Squeeze

The Day Ahead

- With the glut of central bank meetings now out of the way, it may be a quiet end to this week. This week’s policy updates produced few surprises but what they did show was a range of views on what should happen next. At one end of the spectrum, the Norwegian central bank announced an immediate 0.25% interest rate hike with almost certain to follow. At the other end, both the Swedish and Swiss central banks confirmed that they think any rate rises are probably still years away. Possibly of most importance was the confirmation that the US Federal Reserve will probably start tapering its asset purchases in November and that US interest rates may start to rise from next year. Markets initially took the news calmly but it will be interesting to see if that remains the case if those policy moves unfold.

- Yesterday’s September PMI data for the Eurozone, UK and the US highlighted the difficult situation central banks currently face. The data showed further indications that growth is fading, primarily because of supply-side constraints. At the same time, inflationary pressures remain elevated mostly because of those same supply-side issues. Central banks generally still expect these pressures to be transient, but how quickly they will fade is highly uncertain.

- Today’s German IFO survey will provide further evidence on Eurozone growth trends. The last few updates have seen rises in the current conditions measure but future expectations have fallen for the last two months. Expect the latest update to see a continuation of those trends.

- The September CBI retail survey will be released in the UK. The official retail sales measure unexpectedly fell in August for the second month in a row. That may be primarily due to consumers switching to spending on services, but nevertheless the CBI measure will be watched for indications whether September spending patterns have been any different However, given that the CBI actually posted a surprisingly strong reading last month it is clearly not always an accurate gauge of the official measure.

- In the US, new home sales are expected to have risen in August for the second month in a row. However, that is still likely to leave them well below their start of 2021 level.

G10 FX Options Expiries for 10AM New York Cut

(Hedging effect can often draw spot toward strikes pre expiry if nearby)

- USDJPY - 110.50 425m.

- EURUSD - 1.1770/80 729m. 1.1750/60 528m. 1.1720/30 725m. 1.1700/10 1.41bn (1.29bn P). 1.1670 663m. 1.1650 663m.

- AUDUSD - 0.7350/60 627m. 0.7270 837m. 0.7250 565m.

- USDCAD - 1.2900 1.49bn (C). 1.2850/60 1.05bn (C). 1.2800 1.71bn (1.10bn C). 1.2740/50 493m. 1.2710/20 464m. 1.2700 622m.

- 1.2680 760m. 1.2650/60 1.55bn (800m P). 1.2630/40 804m. 1.2610/20 1.50bn (961m P). 1.2580/1.2600 1.35bn (855m P). 1.2560/70 526m. 1.2500 744m.

- EURJPY - 131.50 487m.

- USDMXN - 20.20 475m. 20.10 500m. 19.95 440m.

- USDCNH - 6.60 922m. 6.47 780m. 6.45 514m.

Technical & Trade Views

EURUSD Bias: Bearish below 1.19 Bullish above

- Consolidates gains in quiet Asian session

- EUR/USD opened +0.44% at 1.1737 after USD and JPY eased on broad risk rally

- It consolidated in a 1.1737/47 range in Asia and is around 1.1740 into the afternoon

- EUR/USD resistance is at the 10-day MA at 1.1754

- More resistance comes in at the 38.2 of 1.1909/1.1683 move at 1.1769

- EUR/USD has likely put in a short-term bottom at 1.1665/85

- Range trading likely to resume after downside failure

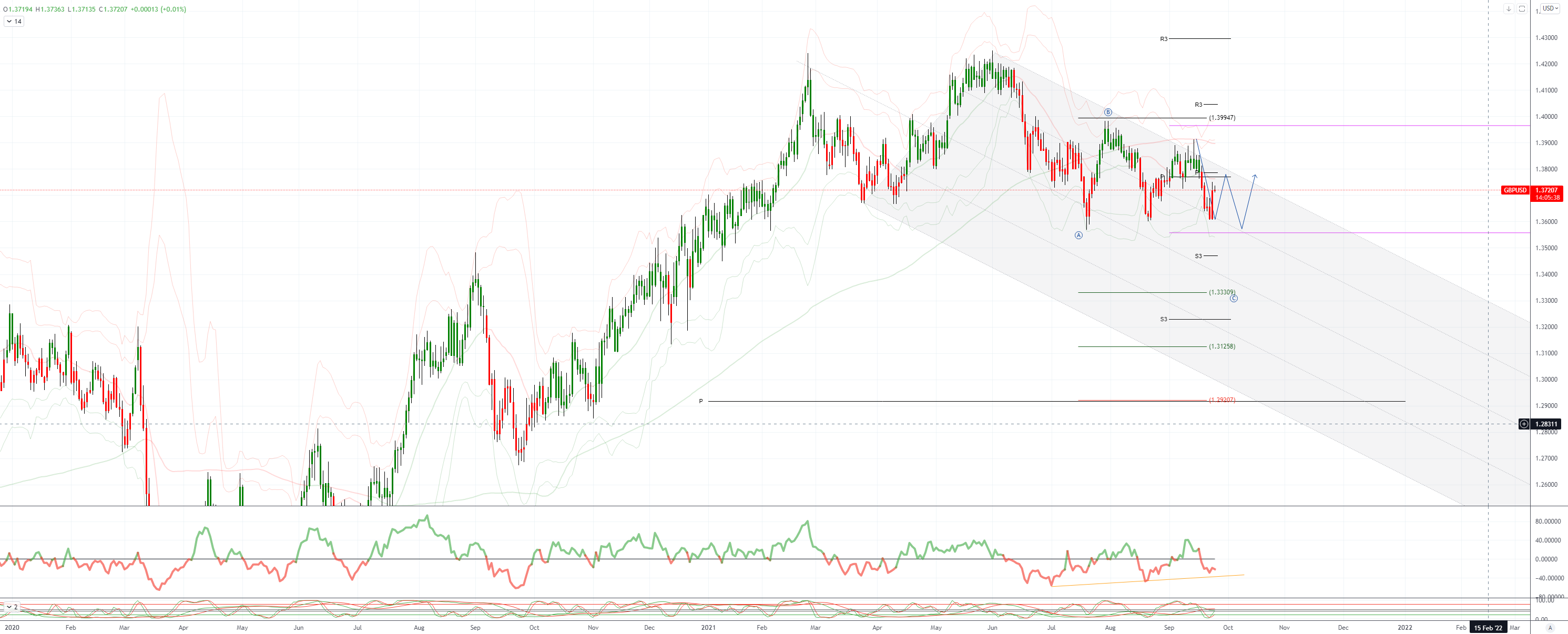

GBPUSD Bias: Bearish below 1.39 Bullish above.

- Sustains Thursday's gains – 1.3770 key

- Steady in a 1.3718-1.3736 range with decent morning flow, then quiet

- Sunak accepts call for financial reforms on Greensill collapse

- UK consumer morale slides on cost-of-living crisis: GfK

- Charts; momentum studies, 5, 10 & 21 DMAs conflict - neutral setup

- 21 day Bollinger bands contract - bias still lower while 1.3771 21 DMA holds

- Close above 1.3771 21 DMA would target the 1.3902 upper 21 day Bolli band

- 1.3602 August low held, leaving a solid double bottom support above 1.3600

- 1.3696, 38.2% of this week's bounce first support - NY 1.3750 top resistance

USDJPY Bias: Bullish above 109 Bearish below

- +0.1% at the top of a 110.20-110.43 range, resilient risk - Nikkei +1.9%

- Japan August core CPI was flat - well below the BoJ target

- PMI slowed as output and orders contracted due to COVID-19

- Effectiveness of Abenomics a key factor for LDP leadership

- Tenkan line poised to cross the horizontal Kijun line - positive signal

- Break above the daily cloud sustained in Tokyo - 110.45 Sept high caps

- 110.50 break to target 110.80 August high, then 110.96, 76.4% Jul-Aug fall

- 109.86 and 110.19 daily cloud parameters are now initial supports

AUDUSD Bias: Bearish below 0.75 Bullish above

- Unchanged after early strength repelled

- AUD/USD opened +0.76% at 0.7396 after USD fell on risk rally

- It traded up to 0.7316 before fading when Asian equities eased slightly

- Heading into the afternoon it is unchanged around 0.7395

- AUD/USD resistance is at 38.2 of 0.0.7477/0.7222 move at 0.7318

- More resistance is found at the 21-day MA at 0.7331

- Close support is at the 10-day MA at 0.7390 and break eases upward pressure

- Key to direction will be sustainability of the risk rally

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!