Decreasing US Economic Uncertainty Pushes Equity Prices Back into Bull Territory

Incoming data on the US economy continues to surprise on the upside, triggering massive unwinding of recession bets and luring investors back into risk assets on decreasing uncertainty. One such report was the ISM report on the non-manufacturing sector released yesterday which surprisingly showed that the sector continued to expand in July at a healthy pace despite aggressive Fed rate hikes and consumer spending pressured by high inflation. The behavior of the index components proved to be even more unexpected: the price index fell from 80.1 to 72.3 points, indicating that pipeline inflation pressures decreased, the new orders index rose from 55.6 to 59.9 points, laying the groundwork for the expansion of activity next month, while the business activity index, contrary to expectations of a decrease, rose from 56.1 to 59.9 points.

ISM Report Price Index

ISM Report NewOrders Index

The reason why the report had major bullish implications for the market is simple – accelerating inflation combined with the Fed's ultra-aggressive pace of rate hikes led to a sharp rise of recession plays in May and June. The point is that the tightening was supposed to suppress high inflation, but at the cost of “demand destruction”— lower consumer spending and reduced investment. However, a number of recent data, in particular the ISM report, have shown that the scenario of a "soft landing" of the economy, which the Fed hopes so much for – bringing inflation back under control while maintaining positive growth rates in consumer demand and investment – is becoming more realistic. The July reports did indeed show the first signs of an easing in price pressures, while at the same time, activity and output indicators, leading indicators such as new orders continued to rise, and in some cases even better than estimates. Given that there is still much uncertainty priced in risk assets, the current rebound should have some room to continue especially if data continues to show resilience of economic activity to the Fed tightening and inflation. The next report in focus is labor market’s NFP which will likely extend the streak of positive US data surprises, giving another boost to risk assets (i.e., equities) and greenback.

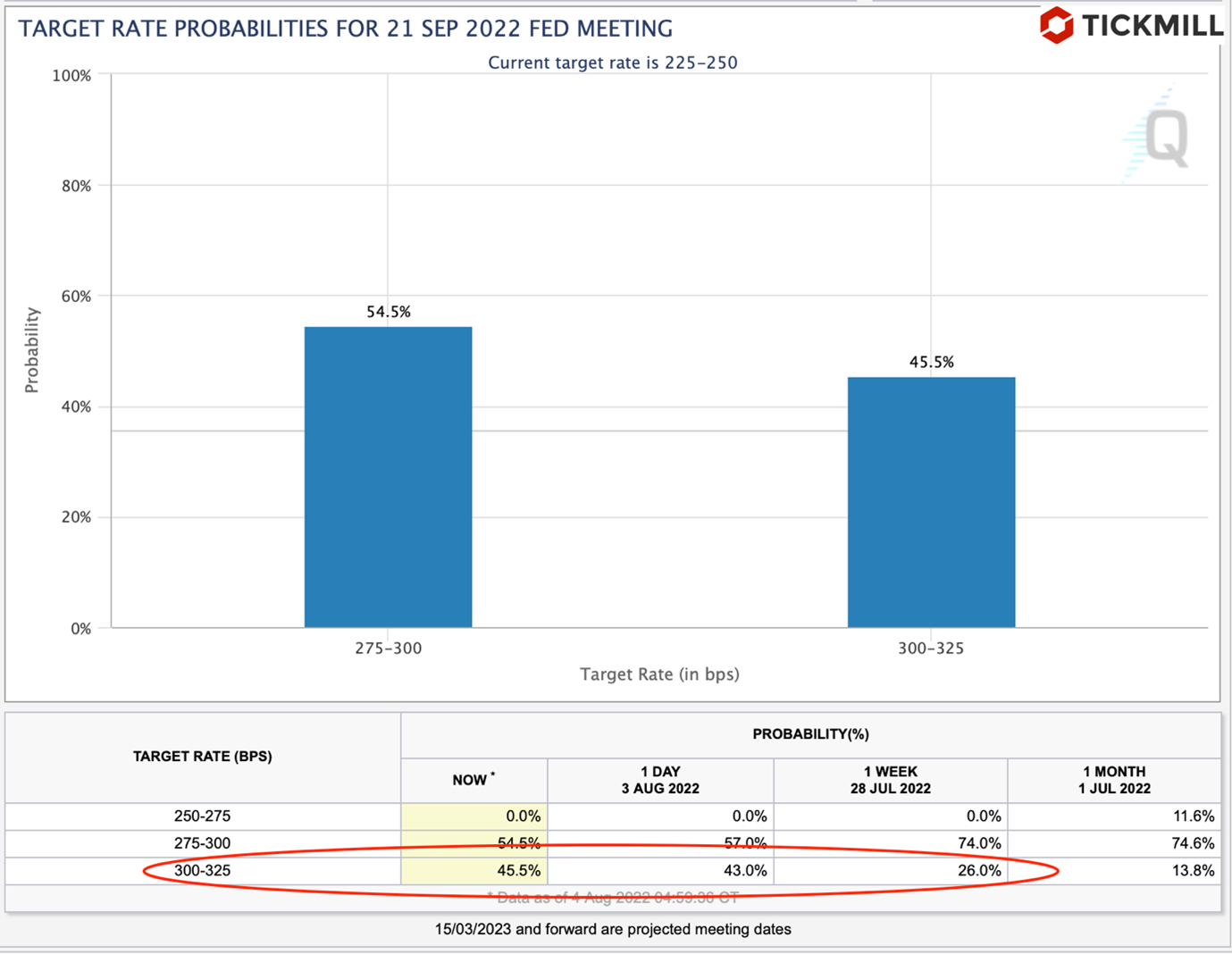

Also yesterday, two Fed officials, Barkin and Daly, made comments, refuting rumors about a policy easing cycle next year. According to the policymakers, the inflation comedown will likely be slow (due to the fact that approximately 50% it is driven by supply-side factors) while fears that policy tightening will drive the economy into a recession that will require rate cuts, are exaggerated. In general, this week, the Central Bank increased verbal interventions to curb the rise of market expectations that the pace of policy tightening will slow down or that the easing cycle will start next year. As a result, the odds that the third rate hike by 75 bp will take place in September increased from 26% to 45.5%:

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.