Dovish ADP Sends Dollar into Decline as Markets Price in a Soft NFP Report

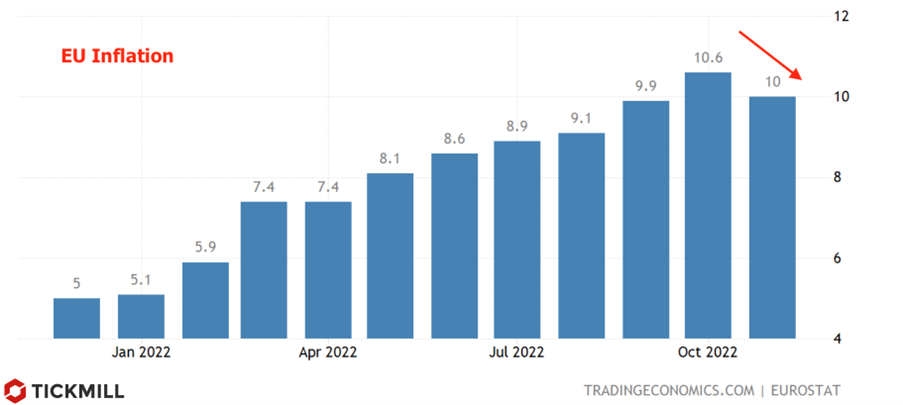

Inflation in the EU declined more than expected, from 10.6% to 10% in November. The main contribution to the favorable dynamics was made by energy prices. The market, as well as the ECB, will be disappointed by the "sticky" behavior of core inflation, which remained unchanged at 5%. However, EU inflation has probably peaked out and therefore there is a growing possibility that the ECB will decide to raise the rate by 50 bp instead of 75 bp in December.

After two surprises on the upside in September and October, inflation in the EU has finally begun to decline. The largest decline was observed in energy prices from 41.5% to 34% in annual terms. Food inflation rose, while core inflation, which is more stable month-on-month and better reflects consumer trends, remained flat at 5%. Inflation is still high, but the turning point appears to be near.

A new episode of the energy crisis could easily resume the growth of headline inflation and delay the decline in core inflation. That is why the market is in no hurry to make the base outcome of 50 bp in December, which provides additional support for the Euro.

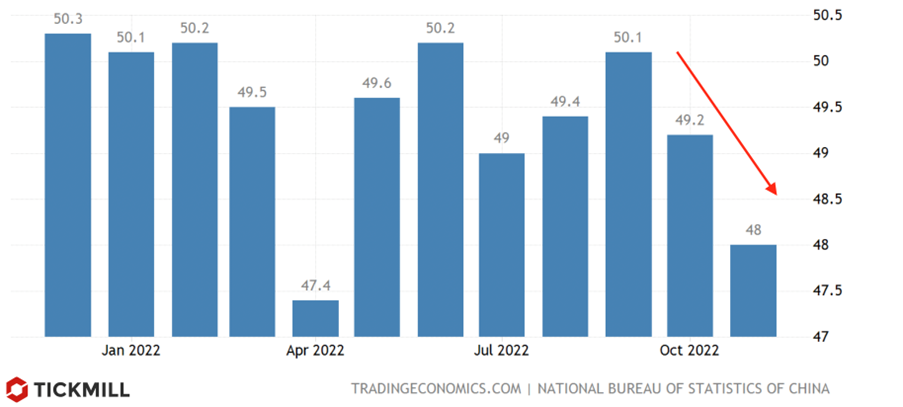

The index of manufacturing activity in China fell from 49.2 to 48 points, which is below the forecast of 49 points. The index has been declining for the second month in a row, and the rate of decline is increasing, which suggests that the situation in China's manufacturing sector is deteriorating at an increasing rate:

The report dampened the market's risk appetite, but the blow to sentiment was softened by the US GDP report (final estimate), which indicated a growth of 2.9% in the third quarter. The ADP report fell short of expectations, with job growth of just 127K vs. 200K forecast. European currencies rose against the dollar, the US currency index sank by 0.4%. If the NFP report also falls short of expectations, markets may start to expect a softer rhetoric from the Fed in December, which the market is likely to factor into prices. This will translate into an additional decline in the dollar, renewed upside in risk assets and decrease in bond yields. The market is waiting for Powell's speech, where the head of the Fed may hint that the central bank will soon begin to slow down the pace of tightening. This is indicated by the minutes of the last meeting of the Fed, in which the degree of dovish rhetoric has increased significantly. Most officials said it would be appropriate to start slowing down the rate of tightening after some time. In addition, two Fed officials, Mester and Williams, talked about the fact that in 2024 the Fed may move to cut rates.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.