EURUSD poised to extend downside trend after dovish German inflation report

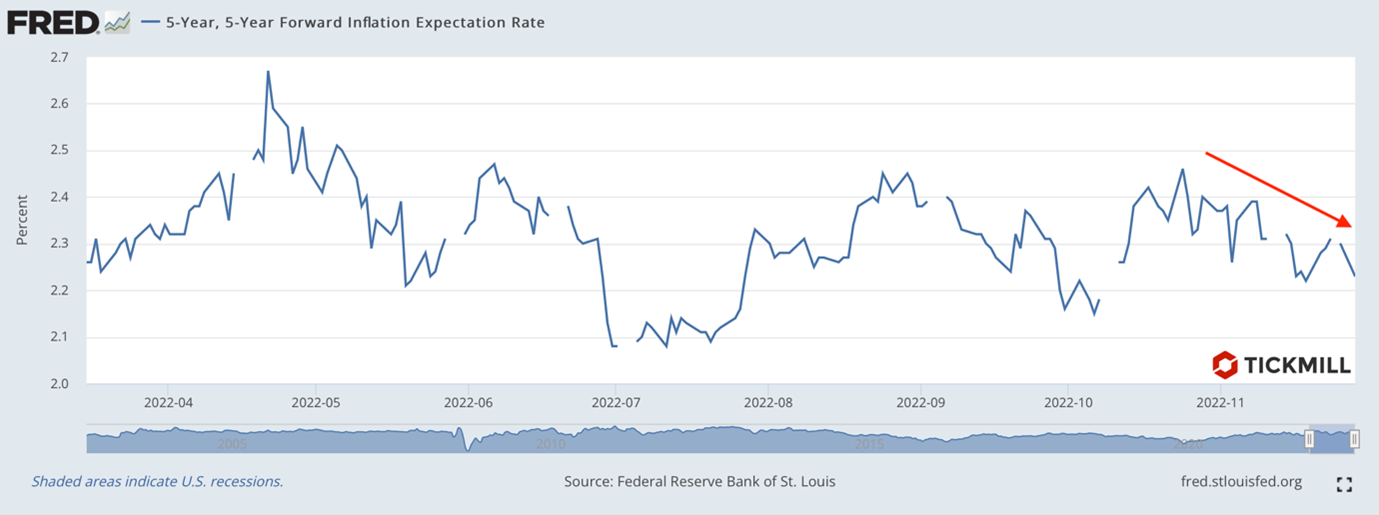

Buying pressure in equity markets remained quiet on Tuesday, cyclical stocks dipped due to worsening global economic prospects. The mass protests in China against the harsh lockdowns and the continued increase in new Covid cases have been one big step back on the path to the reopening of the Chinese economy. Fed Bullard's comments yesterday halted the rise in bond yields as he said markets underestimate the risk that the Fed will continue to aggressively tighten monetary policy. Williams and Loretta Mester, two other Fed officials, made more centrist statements, hinting that the Fed might start cutting rates in 2024 whereas more tightening is needed in the short-term. The Dallas Fed manufacturing index rose from -19.4 to -14.4 in November. Forward market inflation expectations in the US fell to their lowest level in a month amid a sell-off in the commodity markets:

Market rumors that OPEC will decide to cut production at the meeting on December 4th seem to offset the risks of a demand blow from China. Spot WTI and Brent rebounded 3% today.

The indicator of economic sentiment in the EU rose slightly compared to the previous month, mainly due to rebound in consumer confidence.

Manufacturing sentiment fell from -1.2 to -2 in November, the lowest level since January last year. Firms reported a sharp decline in production trends as new orders continued to decline. Manufacturing expectations improved marginally, thanks to the normalization of the supply chains.

In the services sector, the demand indicator continued to decline, but the pace slowed down. The retail sector noticed some recovery in demand and has an optimistic outlook about short-term growth prospects.

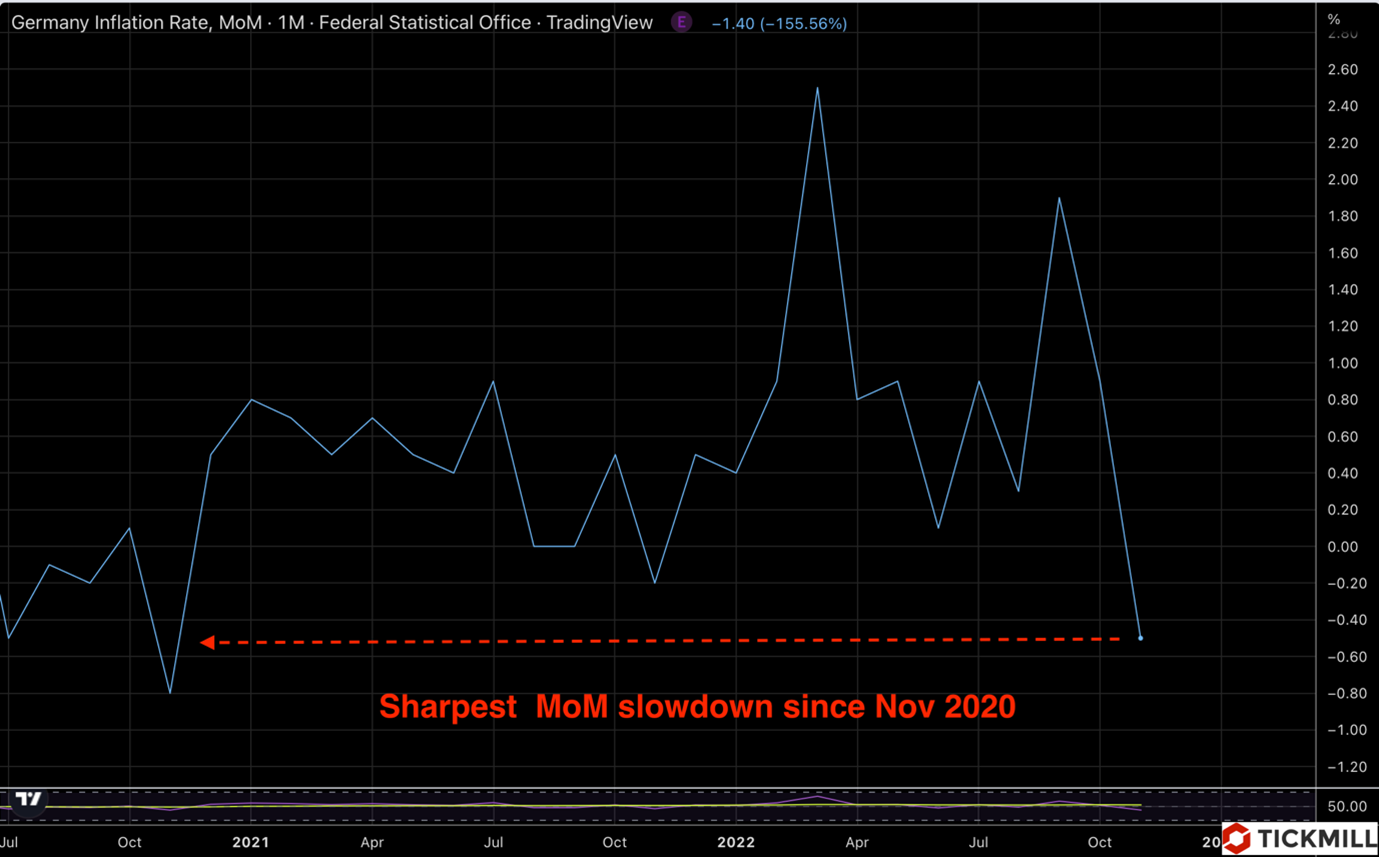

Inflation in Germany slowed to 10% against the forecast of 10.4%, on a monthly basis, deflation was 0.5%, which was the sharpest monthly slowdown since November 2020, the report released on Tuesday showed:

In general, EU’s economic state indicates the onset of a mild recession. However, the ECB said earlier that a slight recession would not be enough to bring down inflation. With supply chains normalizing, inflation expectations lowering and recession risks rising, the ECB is likely to opt for a 50 bps hike in December. With some investors still pricing in a 75 basis point rate hike, this outcome would be disappointing for the market and could trigger a bearish reaction in EURUSD.

EURUSD fell today after release of the inflation report by 50 points, from 1.0370 to 1.0320:

The pair looks poised to extend the downside trend and break below 1.03 level on Powell remarks, due to speak on Wednesday, and on the NFP report due on Friday. Key short-term support levels are seen at Nov 21-21 low of 1.0250 and 1.02.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.