FOMC Minutes: Strong Dollar Will Help to Weather Tough Period of High Inflation

The level of 107 in the dollar index (DXY) remains a hard nut to crack as a bullish retest failed yesterday; the Fed Minutes did not work as a catalyst for a sweeping move, although there were some solid grounds to expect an increase in hawkish rhetoric. Nevertheless, key takeaways from the report argue in favor of a strong dollar, which we will discuss below.

The minutes of the July FOMC meeting showed that the policymakers welcomed the strengthening of the dollar, for the simple reason that it is a strong national currency that is an efficient way to contain import inflation. Given the negative US trade balance, the expensive dollar came in handy to keep inflation from accelerating even higher. The Fed does not think that a strong dollar is hurting the economy or somehow suppressing its growth. Therefore, it is now in the best interest of the Fed to shape policy so as to get through a period of high inflation with a strong exchange rate.

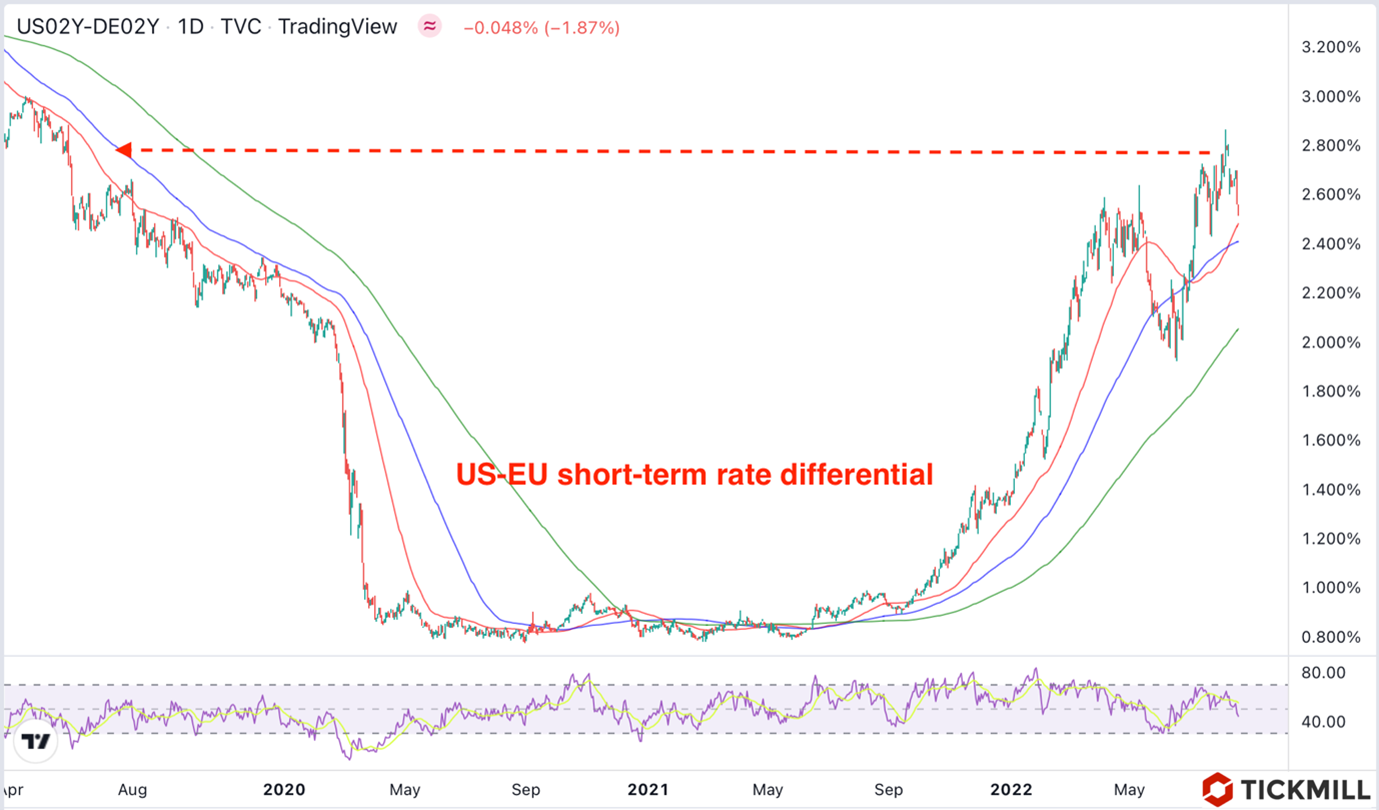

The report said that the weakening euro was the key driver of dollar appreciation, which the Fed believes was the result of a widening real yield differential. The nominal 2Y US-Bund yield spread rose to the highest level in three years with the yearly peak seen on August 1 (2.87%):

To expand room for maneuver, in case incoming US economic data warrants slowdown or pause in tightening, there was a mention in the report about the risk of overdoing rate hikes and QT. This, in fact, was behind the dropping of forward guidance at the last meeting - now the Fed is talking less about its medium-term tightening plans and instead urging markets to focus on incoming economic data in order to understand what to expect at the upcoming meeting. Essentially, this implies a risk that the Fed can put less pressure on the brakes by slowing down the economy to dampen inflation and given that this will happen in the world's first economy, growth in the rest of the world may also be suppressed to a lesser extent. Consequently, currencies that rise during the boom phase of business cycles gain a support factor.

There are three events ahead of us that will help to gauge the odds of a 75 bp rate hike in September. These are the Jackson Hole Symposium (August 25-27), the August NFP (September 2) and the Inflation Report (September 13).

The exchange rate of the European currency, the pound and the yen has now become almost entirely a function of gas prices, which in turn depend on the level of tension in the relations between Russia and the EU. A ceasefire or a truce in Ukraine will help reduce tensions, so markets can be very sensitive to any signals in this direction. Turkish President Erdogan has once again volunteered to extinguish the flames of the conflict, with reports that he will try to convince the Ukrainian President to agree for a temporary ceasefire at a meeting in Lvov on Thursday and even try to revive the Istanbul negotiation process. The markets' attention may be focused on the news after the meeting.

The economic calendar today is not particularly interesting. The final estimate of inflation in the EU for July remained unchanged. US jobless claims data and business data from the Philadelphia Fed may draw some attention. Among them are indices of hiring, new orders, prices paid, and investments in fixed assets. The overall index of manufacturing activity is expected to rise from -12 to -5. Later in the evening, the speeches of the Fed officials, George and Kashkari, are due.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.