Inflation in Germany Eases, Taking off some Pressure on the ECB to Deliver Faster Rate Hikes

Signs of escalation in geopolitical tensions and fresh warnings of recession in top economies pushed stock markets off balance, with the S&P 500 closing down 2% and Nasdaq shedding 3% on Tuesday. European markets picked up the negative baton today, the main equity indices in Europe fall by 1-1.5%. Yesterday it became known that Turkey was able to resolve differences with Sweden and Finland, which means that the path for these two countries to join NATO is now open. The risks of Russian retaliatory measures and a possible new round of escalation boosted demand for defensive assets (bond yields of longer-maturity bonds declined) and dampened risk appetite.

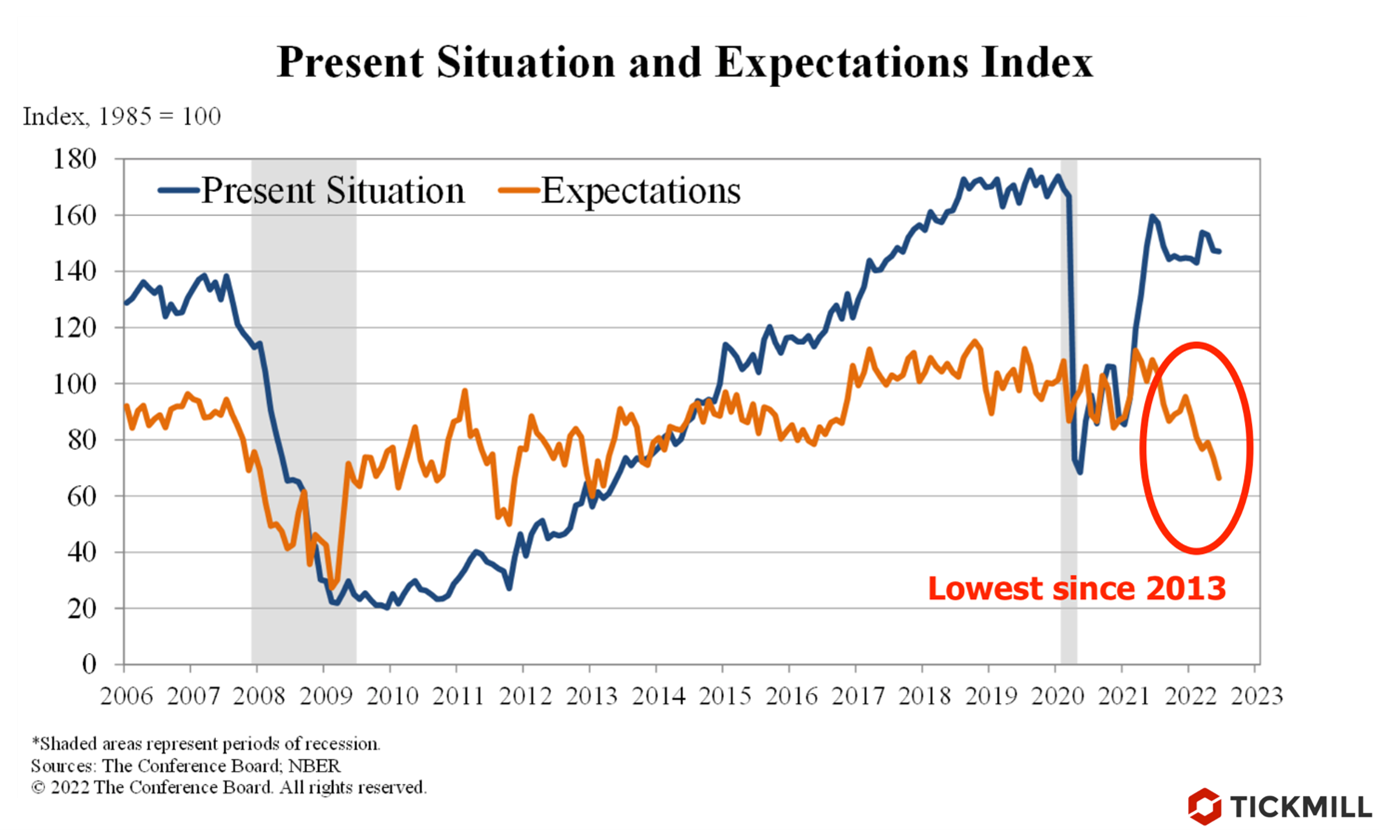

Apart from rising geopolitical tensions there were signs of deterioration on macroeconomic front - the Conference Board report on consumer confidence in the US missed expectations big time, the main indicator fell more than expected (from 103.2 to 98.7 points, forecast 100.4 points). The biggest part of disappointment came from the slack of leading component in the index – household expectations, the corresponding sub-index fell from 73.7 to 66.4 points, the lowest print since 2013:

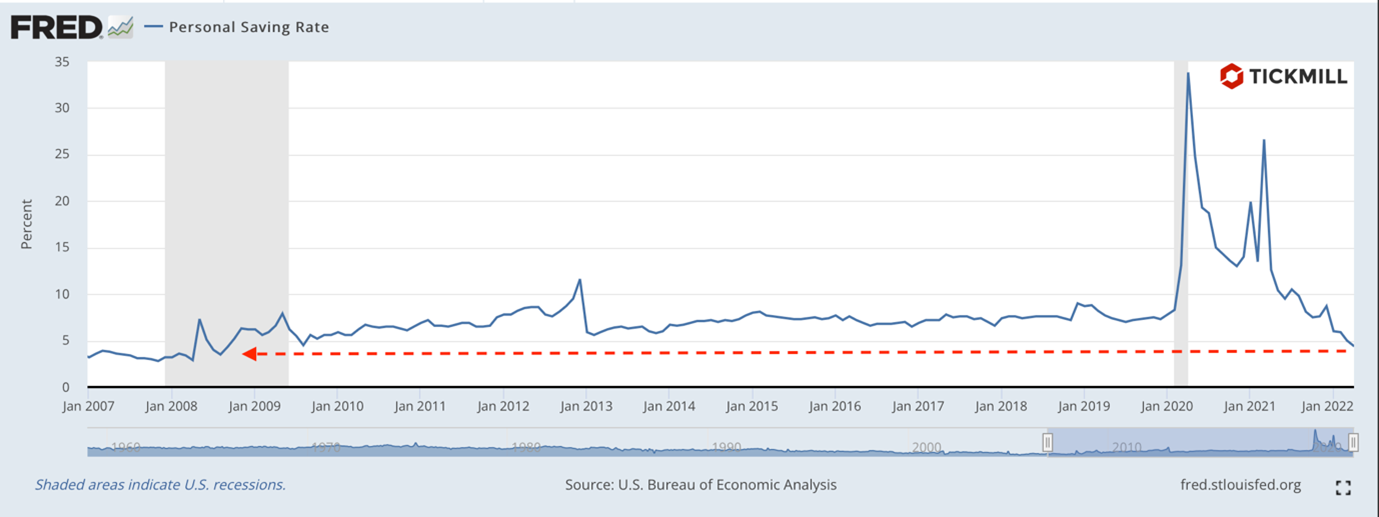

The reason for decline is the drop in the savings rate of American households to 4.4% in response to the rising cost of living and, accordingly, the growing concern about future consumption level:

The Conference Board's index began to show co-directional dynamics with another popular U. Michigan consumer confidence index, which has been falling for several months in a row, which increases predictive power of these soft data points.

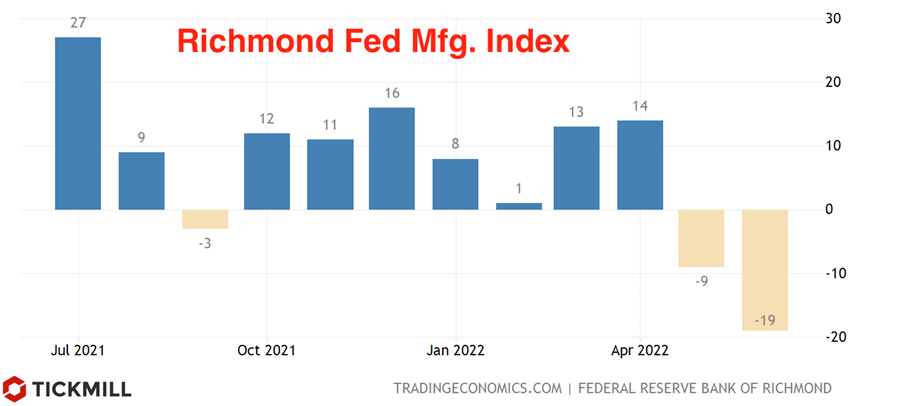

However, pessimism increases not only among households, but also among US businesses, which was reflected in the fall of the Richmond Fed manufacturing activity index from -9 to -19 in June, with a forecast of -7:

Concerns about European growth outlook intensified after release of Morgan Stanley report on Wednesday, which said that the Eurozone economy could fall into recession in the fourth quarter. The two main factors behind the recession, according to the bank's analysts, are a decline in energy supplies from Russia and sustained higher inflation rates, which are reflected in the negative dynamics of consumer expectation and business climate indices. Positive economic growth rates, according to the report, can be expected no earlier than the second quarter of next year on the back of increased firms’ investment. The report also says that the ECB will likely raise rates at each meeting this year bringing the rate to 0.75%, but in September, should economic conditions worsen, the bank may be forced to pause tightening.

June inflation report in Germany reduced pressure on the ECB to expeditiously raise interest rate. Headline inflation was 7.6% against the forecast of 8%, monthly inflation slowed down to 0.1% against the forecast of 0.3%. EURUSD reacted positively to the news, however, the reaction was modest helping the pair to defend the level of 1.05.

Markets will also be closely watching the speeches of the heads of US, EU and UK central banks at the forum in Sintra today. Key thing to watch is the balance between recession/inflation comments. Increased mentions of a recession will likely be interpreted as a signal that policymakers are concerned about costs and risks of aggressive tightening and should prompt market repricing of prospective tightening pace to a less aggressive one. At the same time, the emphasis in speeches on the threat of accelerating inflation or inflation expectations deanchoring will likely be taken as a hint that the pace of tightening will remain high and a negative reaction is likely to follow in risk assets.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.