Inflation Threat Puts Central Banks on Alert

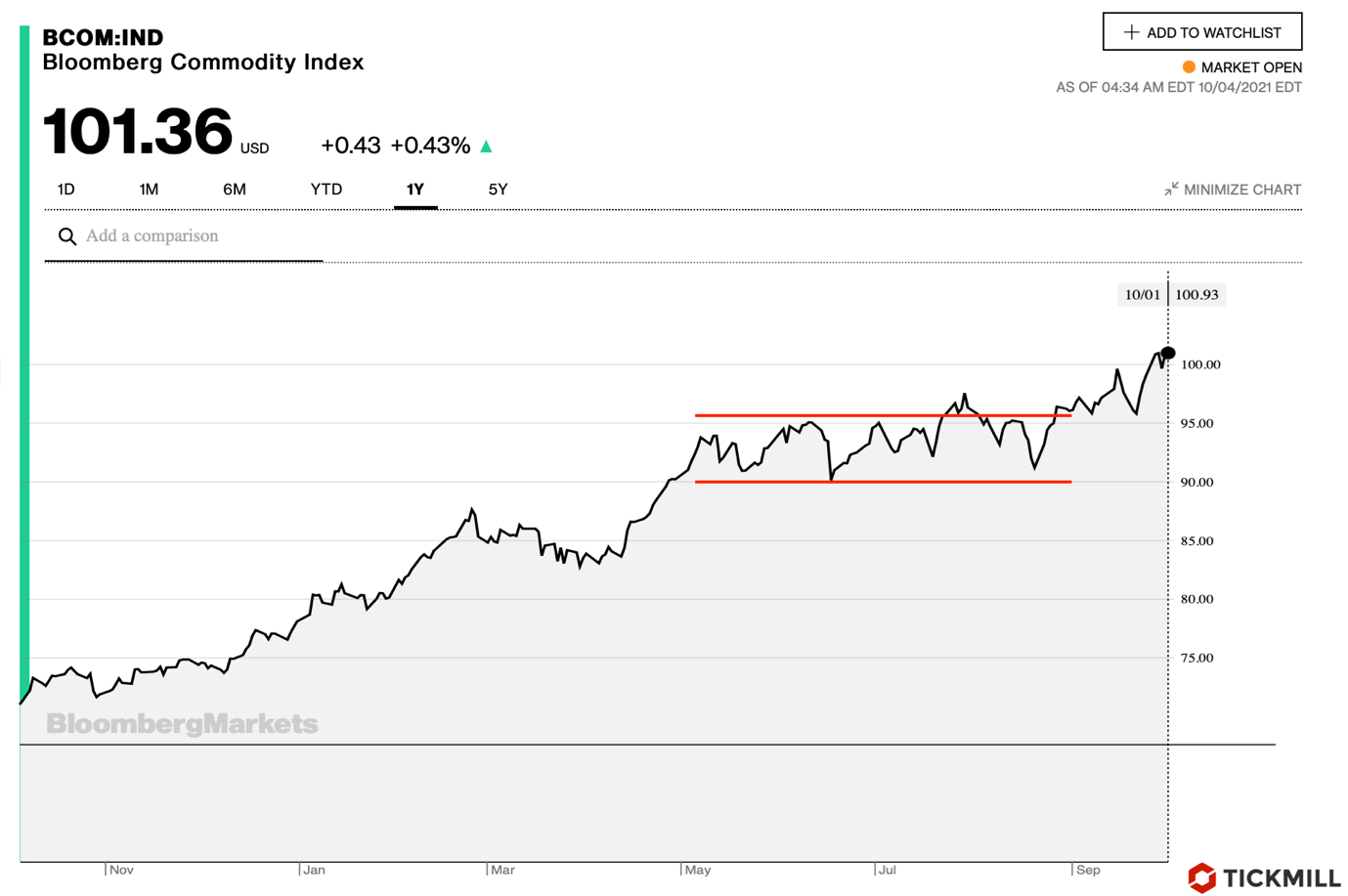

Financial markets are increasingly discussing an inflation surge as shortages arising in the commodity markets increase the risk of price pressures being far more persistent than policymakers expect. After a period of consolidation, commodity prices resumed their rally in September and this coincided with major central bank becoming more hawkish in their guidance (including the Fed); with separate members increasingly voicing their concerns about a “second round” of inflation effects:

It is clear that it is becoming more and more difficult to argue about the temporary nature of inflation, and central banks are forced to adjust their guidance accordingly. The dynamics of exchange rates in the near future will be determined by expectations of how seriously local central banks will take price increases. Those central banks that continue to defend the old point of view (inflation is temporary and does not require policy adjustments) are likely to face more bearish pressure on their currencies.

By the way, the prospect of tighter Fed policy and associated growth in real rates in the US induced a soft downtrend in gold around the beginning of September. This week, expectations for US labor data and the report itself on Friday will most likely allow sellers to test the lower border of the downtrend and the key horizontal level:

On Monday, the ECB official Guindos said that supply disruptions (one of the key supply-side inflation factors) saw emergence of a structural driver, which means there could be more than one "round" of consequences for wages and consumer inflation. Thus, the official hinted that the increased inflation could worry the ECB more than the markets had previously assumed, and perhaps one should expect some policy implications; in particular changes in duration of current asset purchases. The euro gained on the back of hawkish hints of the ECB official, in addition broad correction of the dollar contributed to rebound of EURUSD.

From a technical point of view, the EURUSD rebound from the November 2020 lows is unlikely to develop above 1.17, as key US data are expected this week:

This week's Non-Farm Payrolls report should help the Fed to announce QE tapering at November or December meeting and move to policy tightening later. There is much uncertainty remaining about possible timing of the start of the Fed rate hiking cycle next year, and labor data may affect expectations related to the tightening. A strong Payrolls report may well allow EURUSD sellers to test 1.15 this week.

In the first half of the week, the markets will be focused on the OPEC+ meeting. An increase in production by more than 400 thousand barrels could pull oil prices lower, and NOK and RUB could erase their recent growth.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.