Institutional FX Insights: HSBC 'Embracing A Stronger USD'

HSBC FX Strategy — Re-Embracing a Stronger USD

Top Takeaways

June FOMC is the catalyst for a stronger USD view. The meeting delivered the key ingredient needed to re-embrace broad USD strength after weeks where the dollar had struggled to benefit from Fed repricing.

The Fed is no longer dovish. Policymakers are split on whether rate hikes may be needed this year, and even if that could be read as “neutral,” the market reaction in front-end yields and USD says investors saw it as hawkish.

No forward guidance = more USD support. Warsh’s rejection of forward guidance creates more uncertainty around the reaction function and keeps the rate-hike scenario alive.

Inflation focus is explicit. The FOMC was unambiguous on price stability, and Warsh ruled out re-examining the Fed’s inflation target.

Rates differentials favour USD again. Fed hike pricing is building, while hike pricing elsewhere is receding as oil falls. That creates a cleaner USD-supportive rates backdrop.

Oil is no longer the only FX driver. The USD-oil relationship has weakened, suggesting the market is shifting back toward data and central banks — especially the Fed — as primary FX drivers.

US exceptionalism is returning. The hawkish FOMC gives the market a reason to re-price the USD higher across the forecast horizon.

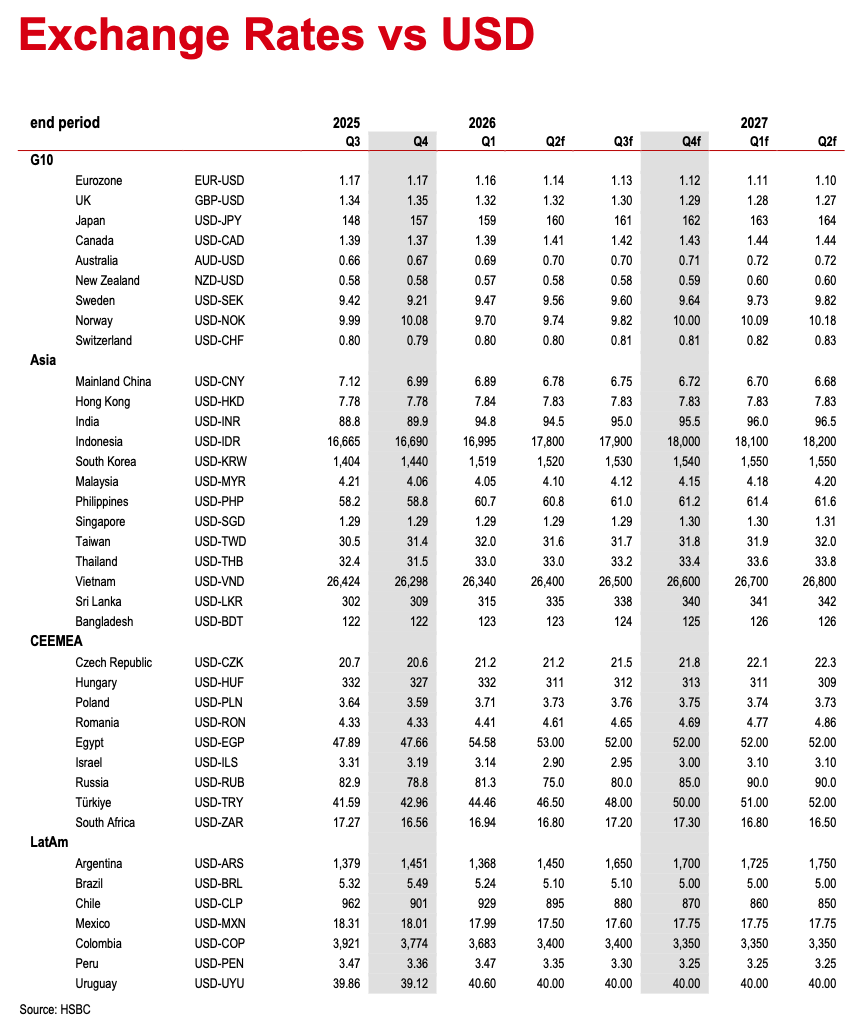

Forecast changes: FX forecasts are being revised to reflect an elevated broad USD throughout the forecast horizon.

Stronger USD: The June FOMC Was the Missing Trigger

The USD strengthened after the June FOMC meeting.

The meeting showed policymakers are split on whether the next move may need to be a hike this year.

On paper, an even split could be called neutral.

But markets did not trade it that way.

Front-end US yields rose, and the USD rallied. That suggests the message was interpreted as more hawkish than expected.

More importantly, the tone has clearly shifted versus previous meetings.

The Fed is no longer leaning dovish. That alone is supportive for the USD.

Why the FOMC Was USD-Positive

The hawkish message came from several places.

First, the projections showed the committee is open to hikes.

Second, both the statement and Warsh’s press conference made clear that the FOMC remains fully focused on price stability.

Third, Warsh explicitly ruled out revisiting the inflation target.

That matters because any hint of re-examining the target could have undermined Fed credibility and hurt the dollar. Instead, the Fed reinforced the inflation-fighting framework.

Finally, the creation of five Fed task forces — including one on communications — adds uncertainty to the reaction function.

Combined with Warsh’s known criticism of forward guidance, this means markets cannot rely on the Fed to pre-commit or guide them away from hike risk.

Bottom line: No forward guidance plus a clearer inflation focus keeps the rate-hike scenario alive.

Rates Differentials Are Back in the USD’s Favour

The FX implication is straightforward.

If Fed hike risk remains alive, the USD is supported through rates differentials.

This is even more powerful because the recent fall in oil has reduced hike pricing elsewhere.

So we now have:

Fed hike pricing building.

Non-US hike pricing receding.

US front-end yields moving higher.

USD finally responding.

That creates a more constructive broad-dollar setup.

In recent weeks, OIS markets had repriced the Fed path from cuts toward hikes, but the dollar had not benefited much.

That suggested a catalyst was needed.

The June FOMC provided it.

Oil Is Fading as the Main FX Driver

In the latest Currency Outlook, the argument was that risks to the soft-USD view were crystallising and that the June FOMC was a critical juncture.

Before the meeting, the USD was still highly correlated with oil and Middle East headlines.

But that relationship had started to weaken.

That was important.

It signalled that other FX drivers were becoming more important again, especially:

US economic data

Central-bank communication

Fed reaction function

Relative rate expectations

After the June FOMC, that shift looks more durable.

The market has moved from trading the dollar mainly as a geopolitical/oil hedge toward trading it as an exceptionalism/rates currency again.

Forecast Implications

The June FOMC changes the USD baseline.

The prior soft-USD view was already facing rising risks. Now those risks have crystallised.

FX forecasts are being revised to reflect a more elevated broad USD across the forecast horizon.

The core rationale:

The Fed is less dovish.

Forward guidance is gone.

Inflation remains the dominant focus.

Hike risk is alive.

US data remains resilient.

Oil is lower, reducing hike pressure elsewhere.

Rates differentials are again USD-supportive.

Practical FX Read

USD Should Stay Supported Against:

EUR: ECB is hawkish, but Fed repricing and USD exceptionalism cap EUR upside.

CHF: Low-yielding funder; SNB wants a weaker currency.

SEK: Low-yielding funder with weaker growth.

CAD: Lower oil and weak domestic fundamentals weigh.

NZD: Weak domestic backdrop and rich positioning.

USD May Underperform Less Clearly Against:

AUD: Supported by procyclical carry and global growth if the MOU holds.

ZAR/MXN: Carry and risk appetite can still protect higher-yielders.

JPY: Intervention risk and crowded shorts complicate USD/JPY upside.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!