Institutional Inisghts: Deutsche Bank Investor Flows & Positioning 1/6/26

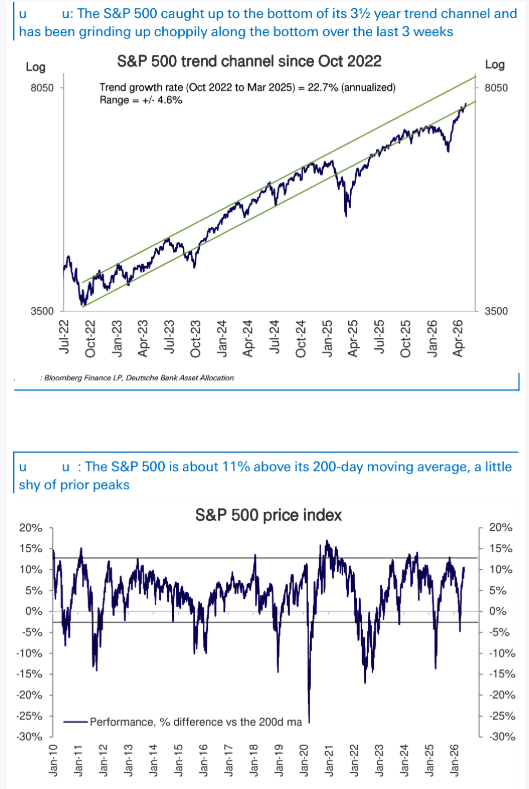

The S&P 500 has effectively caught up to the bottom of its 3½-year trend channel and has been grinding higher along that lower boundary for the past three weeks. Deutsche Bank’s core message is not bearish, but it is more measured: the two main catalysts for the rally, Middle East de-escalation and a very strong Q1 earnings season, now look largely played out. That argues less for a continued straight-line rally and more for a slower, choppier grind higher, potentially with pauses or breathers, and with rotation toward sectors and regions that lagged the Tech-led rebound.

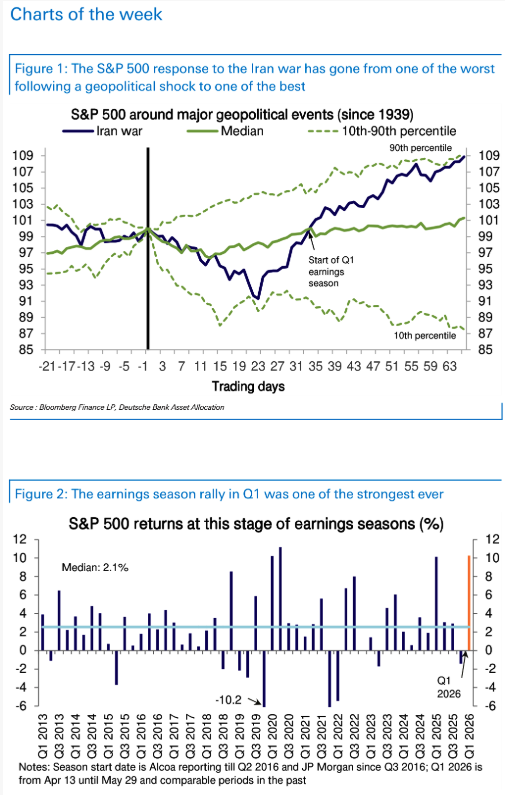

The Middle East relief rally appears mature. At the end of March, the equity market selloff had put the S&P 500 in the bottom decile of historical responses to geopolitical shocks, meaning it was pricing one of the worst outcomes on record. The subsequent rally has now pushed the market into the top decile of outcomes, meaning equities have already moved as if one of the better geopolitical outcomes is likely. In that context, further tangible relief on the war front may not be a major upward catalyst for the overall index. However, it could still matter a lot for relative performance. De-escalation is more likely to drive rotations into lagging sectors and regions, especially those that were penalized by higher oil, risk aversion, and geopolitical uncertainty, rather than deliver another large index-level rerating.

The earnings-season rally has also been unusually powerful. The S&P 500 is up roughly 10% since mid-April, one of the largest earnings-season rallies on record. The rally was backed by very strong earnings growth of about 25%, arguably the strongest in two decades, and by substantial upgrades to bottom-up consensus estimates. Deutsche Bank notes that 2027 S&P 500 consensus estimates were upgraded by about 10%, with Tech upgraded by roughly 20% and Semis by an extraordinary 46%. The bottom-up consensus now expects high S&P 500 earnings growth to persist in the 22% to 23% range, a view Deutsche Bank broadly shares, but the key issue is that the pace of further upgrades is unlikely to continue at the same speed.

That matters because a sizable portion of recent earnings strength came from non-linear product-price surges driven by supply-demand squeezes, especially in Tech but also outside it. If supply-demand imbalances begin to ease, prices could fall, and that would flow directly into margins and earnings. In other words, the earnings story remains strong, but the upgrade impulse is likely to slow. The market can continue to rise on high earnings growth, but it becomes harder to rally at the same pace if the earnings revision cycle is no longer accelerating.

Concerns around the coming wave of equity issuance also remain a persistent overhang, even if Deutsche Bank views them as overblown. Investors continue to worry that a deluge of mega-IPOs could crowd out the broader equity market by absorbing capital and creating supply pressure. Deutsche Bank pushes back against that fear, arguing that academic literature and historical evidence from past issuance waves suggest these periods are usually associated with strong equity market returns both before and during the issuance wave. The reason is that robust demand for equities typically more than offsets the added supply. Still, even if the concern is not fundamentally justified, it remains part of the market narrative and may contribute to a choppier tape.

Political noise is another reason to expect less linear upside. With US mid-term elections approaching, the probability of political headline risk is rising. This does not necessarily derail the equity market, especially if earnings, inflows, and buybacks remain supportive, but it adds another layer of uncertainty after a period in which equities have already priced substantial relief from geopolitical and earnings risks.

Importantly, Deutsche Bank does not think overall equity performance or positioning is stretched. The two-month rally has been one of the sharpest on record following comparable selloffs, but it has only brought the S&P 500 back to the bottom of its 3½-year trend channel. The index is about 11% above its 200-day moving average, still slightly below prior extremes. Overall equity positioning is only modestly overweight, in the 61st percentile. Discretionary investors are in the 57th percentile and still have room to add exposure if earnings growth stays strong. Systematic strategies are in the 67th percentile and could also add if volatility remains subdued.

Demand-supply remains favorable for US equities. Inflows into US equities have stayed strong, with another $8.5bn of inflows this week, while buyback announcements remain solid. This is an important offset to concerns about issuance, positioning, and catalyst fatigue. As long as inflows and buybacks remain robust, the market retains a structural bid. The rest of the world, by contrast, has seen large outflows, but Deutsche Bank notes that those could reverse if tangible relief on the war front improves global risk appetite. That is another reason why de-escalation may matter more for rotation than for outright S&P 500 upside from here.

The clear exception to the “not stretched” argument is large-cap Tech. Deutsche Bank argues that Mega-Cap Growth and Tech stocks have come full circle, moving from the bottom to the top of their outperformance channel versus the rest of the S&P 500. Mega-Cap Growth, Tech, and the Nasdaq 100 are now nearly 20% above their 200-day moving averages, close to prior peaks. Positioning in large-cap Tech is also at the top of its historical band, in the 95th percentile. That makes the group vulnerable if positive catalysts dry up, especially after the extraordinary pace of earnings upgrades and the recent AI-led momentum surge.

The practical conclusion is that the market’s next phase is likely to look different from the last one. The March-April rally was powered by relief from an extreme geopolitical shock and an exceptional earnings revision cycle, especially in Tech and Semis. Those supports remain, but their marginal impact is fading. Meanwhile, large-cap Tech positioning and performance are stretched, while broader equity positioning is not. That combination argues for a slower, choppier grind higher rather than a clean breakout, with the best opportunities likely in rotation: lagging sectors, non-US equities, software catch-up, select consumer, financials, industrial idiosyncratics, and other areas that can benefit if the market broadens beyond the most crowded large-cap Tech winners.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!