Institutional Insights: Credit Agricole FX Weekly 22/5/26

The 90-Day Conflict: A Closer Look

Next Friday marks the 90th day of the ongoing US-Iran conflict. So far, oil prices have remained surprisingly stable due to several factors: (1) a surplus of crude oil already in transit and stored outside the Strait of Hormuz; (2) the US permitting imports of Russian oil; (3) a decrease in demand as buyers scale back; and (4) an increase in US energy production. However, we are approaching a tipping point where the first two factors are diminishing, demand destruction is impacting economic growth, and the US's elevated energy output could face challenges if President Donald Trump chooses to limit refined oil exports as we enter the summer driving season.

Investor sentiment regarding a potential US-Iran agreement is far from optimistic. Although Trump claims that negotiations are in their final stages, he simultaneously threatens to escalate military actions against Iran to force a deal. The unclear timeline for Iran to respond and the possibility of renewed US strikes are significant in the coming days.

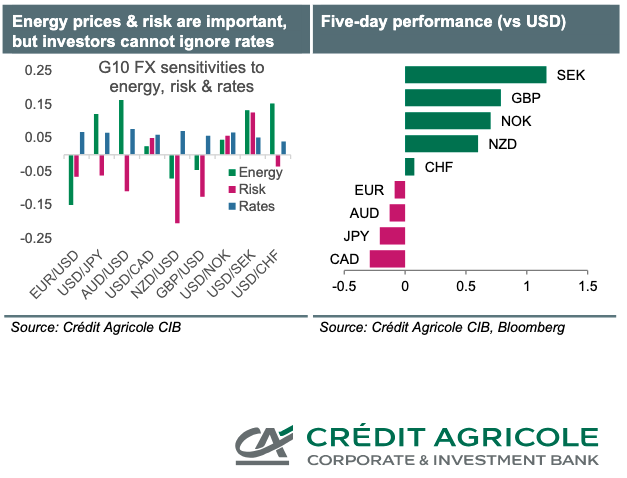

Meanwhile, investors cannot overlook interest rates, as the repercussions of rising oil prices begin to manifest in economic indicators. Recent PMI data has highlighted negative effects on growth, while next week’s release of core PCE data from the US and CPI data from the Eurozone will shed light on inflation trends. Kevin Warsh is set to take over from Jerome Powell as Chair of the Federal Open Market Committee (FOMC). Although there’s no scheduled address from Warsh yet, we can expect insights from other FOMC members, along with comments from several European Central Bank Governing Council members.

In terms of upside potential, unexpected inflation figures in the US and hawkish statements from the FOMC have prompted investors to rethink their previously dovish outlook on Federal Reserve policies. Given the ongoing strength of the US economy, it’s possible that the current pause in Fed rate policy could extend longer than anticipated, regardless of the leadership change at the FOMC. Consequently, US interest rates—an essential element of the ‘USD smile’ alongside market risk sentiment—could continue to be a significant driver for foreign exchange markets, potentially bolstering the USD in the near future.

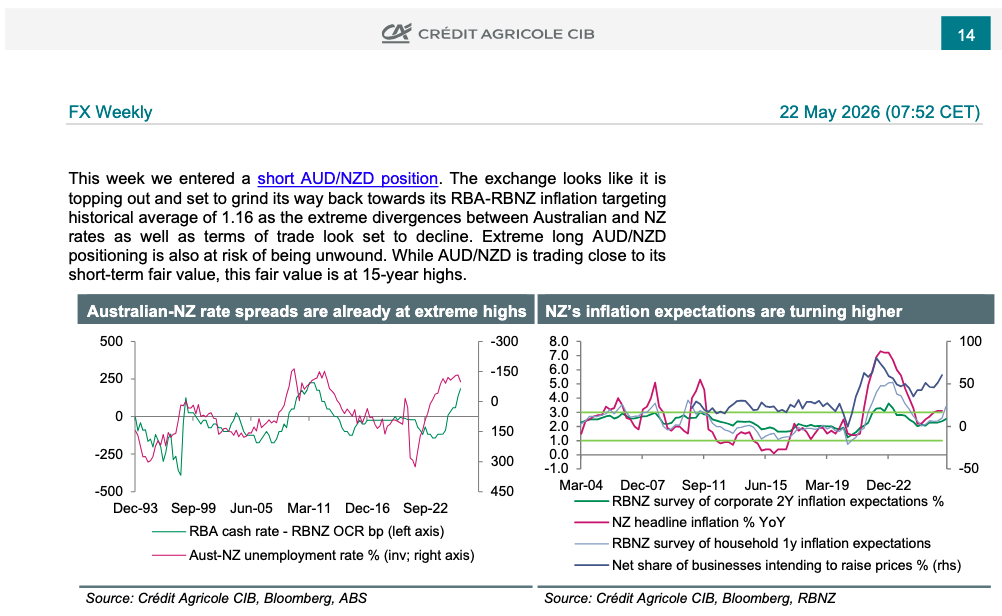

In Australia, inflation data is set to be released soon. While the Reserve Bank of New Zealand (RBNZ) is expected to keep rates unchanged, it will signal its readiness to hike interest rates if necessary. This week, we adopted a short position on AUD/NZD as part of our strategy.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!