Institutional Insights: Goldman Sachs Month End Rebalancing Flows To Know

Month-End US Pension Rebalancing: $14bn Equity Sell / Bond Buy

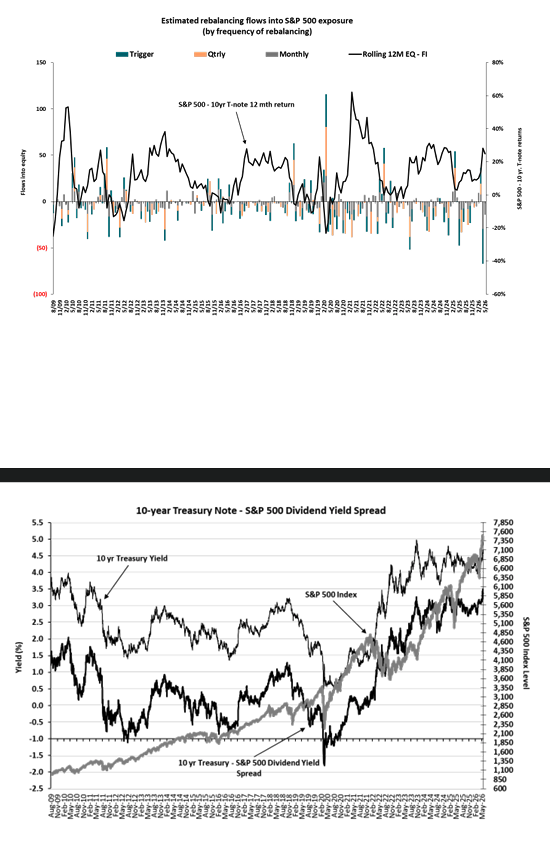

The month-end pension rebalance adds a modest but real supply risk into an otherwise constructive equity tape. The desk’s model estimates $14bn of US equities to sell from US pensions into month-end, with an equivalent amount of bonds to buy, reflecting the fact that equities have materially outperformed fixed income in May.

Month-to-date, the relative performance gap is large:

- **S&P 500 total return:** +3.77%

- **10-year Treasury total return:** -1.03%

- **Equity outperformance versus fixed income:** +4.80%

That equity outperformance mechanically pushes balanced pension portfolios above target equity weights, requiring sales of equities and purchases of bonds to rebalance.

## How the estimate evolved

The rebalance estimate started May as insignificant. During the first week of the month, it remained small until the 1.46% equity move higher on May 6, which pushed the model to a modest $3bn equity sell estimate.

From there, the estimate grew in a relatively linear fashion as equities continued to outperform bonds. By May 18, the model entered double-digit territory, with roughly $12bn of equities to sell.

More recently, the estimate has fluctuated in a $3-4bn range and currently stands at $14bn of US equities to sell, with a matching $14bn of bonds to buy.

## Historical context

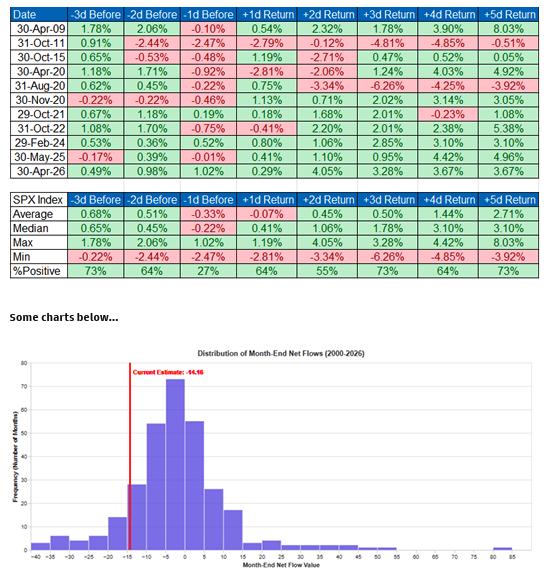

The $14bn sell estimate is meaningful, but not extreme.

On an absolute dollar basis, across both buy and sell estimates:

- It ranks in the 69th percentile over the past three years

- It ranks in the 80th percentile going back to January 2000

On a net basis, however, the sell pressure is less extreme:

- It ranks in the 25th percentile over the past three years

- It ranks in the 13th percentile going back to January 2000

The reason for the difference is that $14bn is a relatively large absolute rebalance, but as a directional equity sell estimate it is not especially large compared with the biggest historical sell events.

The desk also notes that this is the 12th largest non-quarterly sell estimate on record since 2000. Historical returns around the 11 larger non-quarterly sell estimates are mixed, though the three-day pre-rebalance return was positive nearly three-quarters of the time.

## Market implications

This flow is a headwind into month-end, but it does not appear large enough by itself to overwhelm the broader tape. It should be understood as incremental supply, not a stand-alone bearish catalyst.

The context matters:

### Supportive forces

- Geopolitical headlines have improved, supporting risk appetite.

- Buybacks remain active, with 99% of S&P 500 corporates in the open window.

- Hedge funds have been buying again, especially macro products, discretionary, and tech.

- Short exposure in US index and ETF products is at a 10-year high, creating squeeze risk.

- Software, most-shorted names, and unprofitable tech are catching a bid.

- VIX has fallen toward 15.7, and front-end implied vol remains soft.

### Offsetting headwind

- Month-end pension rebalancing implies $14bn of equity supply.

- That equity sale is paired with $14bn of bond demand, which may modestly support Treasuries.

- If bonds rally further and yields fall, that could partially cushion the equity impact by supporting duration-sensitive growth and software.

## Link to current tape

The rebalance estimate lands at an interesting moment. Equities have just rallied on hopes for a US/Iran de-escalation and a broadening software/short-covering squeeze. The S&P 500 closed at 7,564, and the near-term implied move through tomorrow was roughly 0.47%, or about 36 points, implying a range around 7,528 to 7,600.

The pension rebalance could make it harder for the index to break meaningfully above the top of that implied range into month-end, especially if discretionary sellers and asset managers remain net sellers. But the associated bond buying could help keep the 10-year yield contained, which would be supportive for the same parts of the market that have led the recent broadening: software, consumer discretionary, and higher-duration growth.

The model points to $14bn of US equity selling and $14bn of bond buying from month-end US pension rebalancing. This is a meaningful flow, ranking in the 80th percentile in absolute terms since 2000 and the 12th largest non-quarterly sell estimate on record, but it is not extreme on a net historical basis.

For trading, it argues for expecting some month-end equity supply and potential bond support, rather than a major de-risking event. The bigger directional driver remains geopolitics and positioning. If US/Iran headlines continue to improve, the market can likely absorb the rebalance. If headlines deteriorate, the rebalance could amplify near-term downside pressure.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!