July NFP Preview: “Bad News is Good News” Reaction is Highly Likely

The dollar retreated 2% from yearly highs and appears to be primed for a rally which could be triggered by the labor market report. However, the reaction of the US currency may prove to be asymmetrical - if Payrolls disappoint, the correction is likely to be shallow and short in time on the back of expectations of a possible upside surprise in US CPI next week. In addition, there should be a lot of attention on wages as weak job growth combined with a good pace of wage growth will be an indicator that labor supply cannot meet high demand, which means that the labor market will continue to generate inflation through wages, which will require maintaining a high pace of policy tightening.

The volatility of major currency pairs continued to decline this week, and a good picture of the earnings season in the US combined with a couple of solid US macro reports fueled demand for risk assets. Demand for emerging market assets, in particular EM sovereign debt, has also revived, as one indicator that the search for yield is resuming. For example, Turkish bonds denominated in foreign currency showed good rally this week.

Expectations for the Fed's terminal rate this year have stabilized at the level of 3.25-3.5% and are unlikely to change without a serious economic shock. And the Fed itself this week made verbal interventions that attempted to shift focus from the persistence of inflation and excessive concerns about a recession next year, hinting that the central bank is unlikely to deviate from the tightening course or move quickly to cut rates next year. The NFP report today, in general, should reinforce expectations that there will be no deviation from the previously outlined course of tightening. Employment is expected to rise by 250K, and wages by 0.3% in monthly terms and by 4.9% in annual terms. Any surprise higher in wages will mean the Fed will have to work hard to get inflation under control. And the risk of an unfavorable CPI report next week will also keep investors on their toes.

Based on the arguments above, there appears to be few reasons for investors to dump greenback. In addition, the factor of pressure on the two key opponents of the dollar ‒ the euro and the yen ‒ will be a carry trade, due to lower interest rates than in the US, which will make them the currency of choice for the purpose of funding those trades.

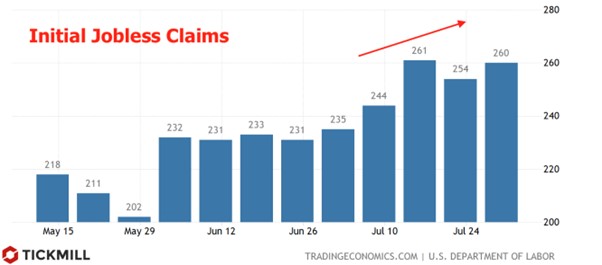

Analyzing preliminary data on the labor market for July, one can note an increase in the number of initial claims for unemployment benefits in July compared to June:

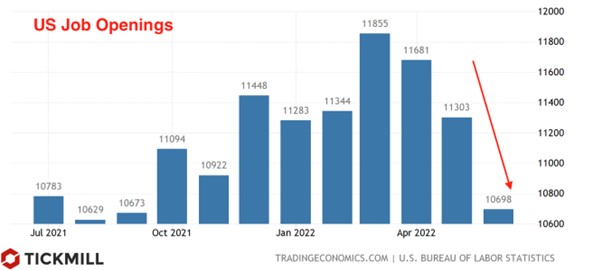

The change in the number of open vacancies indicates some cooling in demand for labor, which also does not speak in favor of strong Payrolls:

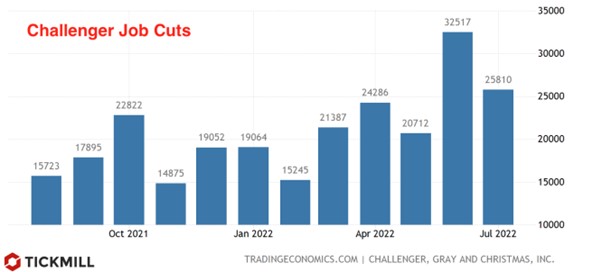

Challenger data shows US companies announced in July plans to cut roughly 25K jobs. This is the second highest this year, after a high of 32.5K in June:

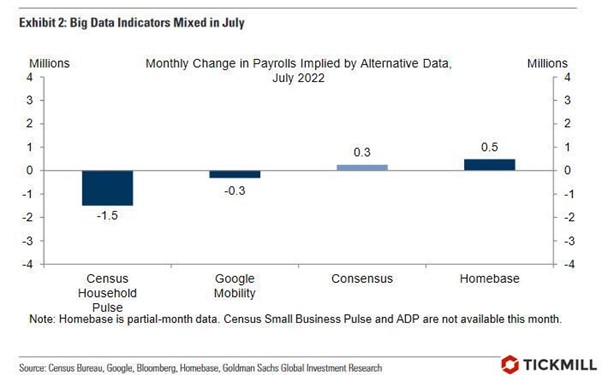

High Frequency Employment Indicators paint a mixed picture of employment dynamics, with Homebase seeing a 500K increase, while Google Mobility and Census Household Pulse data warned the economy is losing jobs:

With market rallies fueled by low interest rates, or at least expectations that the Fed will ease the pace of tightening, market reaction to the NFP today could be in the spirit of “bad news is good news”: weak job growth will help to expect a cautious Fed, while a better-than-expected Payrolls print will further decrease the odds of the dovish “Fed pivot”.

Employment data is also out in Canada today. Last month, the data was not very positive, showing a 43K job cut. This month, according to preliminary data, things should be much better, the consensus forecast expects a gain of 15,000 and unemployment at 5%. If the data confirms expectations, the CAD is likely to react positively, as the Bank of Canada is expected to raise rates by 50 bps in September and the market needs more arguments to count on such an outcome.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.