Market sell-off ahead of the FOMC increases chances for a dovish policy outcome

Despite mixed data on the US economy released on Thursday (strong retail sales and unemployment claims, weaker-than-expected industrial production), Treasury sell-off gained momentum with two-year yield climbing above 3.90%. Rate futures imply a 4.5% Fed interest rate in March 2023. Since the start of September markets have added almost 50 basis points to the expected Fed tightening, therefore triggering a broad market risk-off, w and facing yet another discount rate shock.

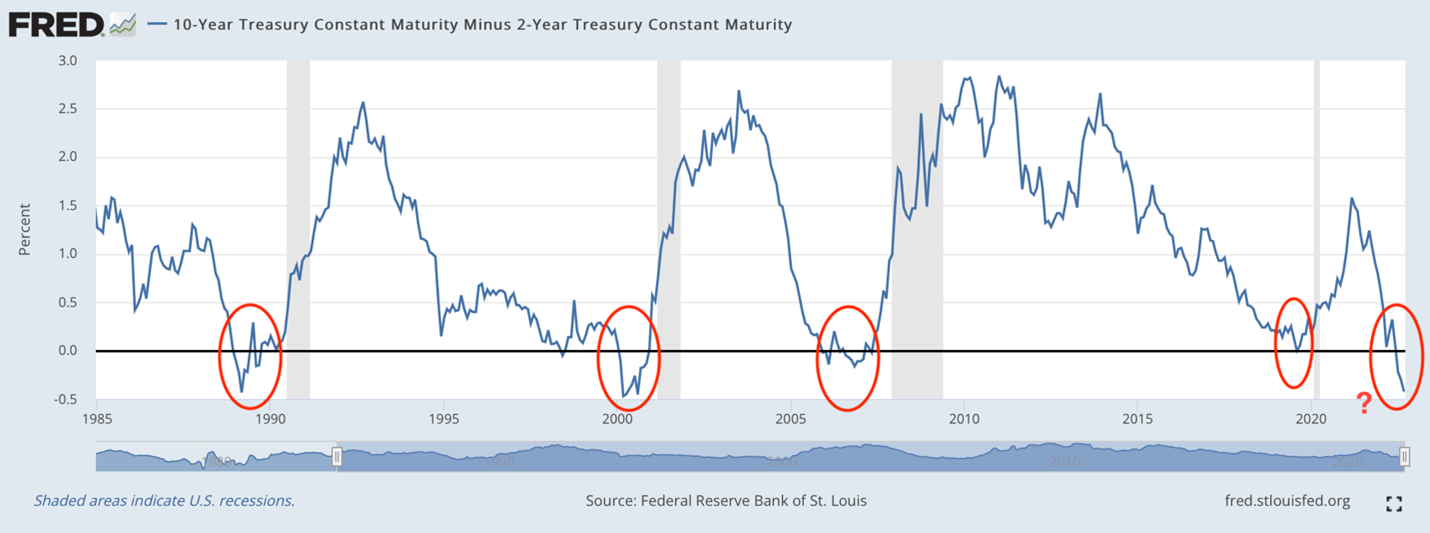

In the Treasury market we see a continuing inversion of the yield curve, with the spread between 10 and 2-year Treasury yields dropping to a new low of -0.43%. At the same time, 10-year bond yield stabilized around 3.45%, while 2-year yield continued its march to higher levels, the expectations of the Fed aggressive withdrawal of liquidity support prevailed over the expectations of high inflation (both negatively affect the price of bonds). A closer look on 10y/2y spread reveals that decline in the spread to zero or its fall into negative territory is often associated with a recession in the US:

Market reaction to intensifying inversion of term structure of US rates is close to that described in macroeconomics textbooks: a strong dollar, hard hit cyclical and commodity currencies, and a downtrend in the commodity market. In fact, key asset classes are pricing in the risk that the central bank tightening will lead to such a destruction of consumer demand that it will cause a recession in the global economy.

In the foreign exchange market, the dollar remains the top choice. The average gain against European currencies since the start of the week was 1.6%, against NOK - about 2.5%. GBPUSD declined the most on Friday, as the market is growing confident that the Bank of England will be the underdog in the tightening race and hike the interest rate by 50 basis points, while the ECB and the Fed have already raised rates by 75 basis points in recent meetings.

It is difficult to expect a sustainable recovery in risk demand in such a situation; market rallies will likely be shallow and short-lived reflecting prevailing bearish sentiment, so betting on a major bounce could be risky.

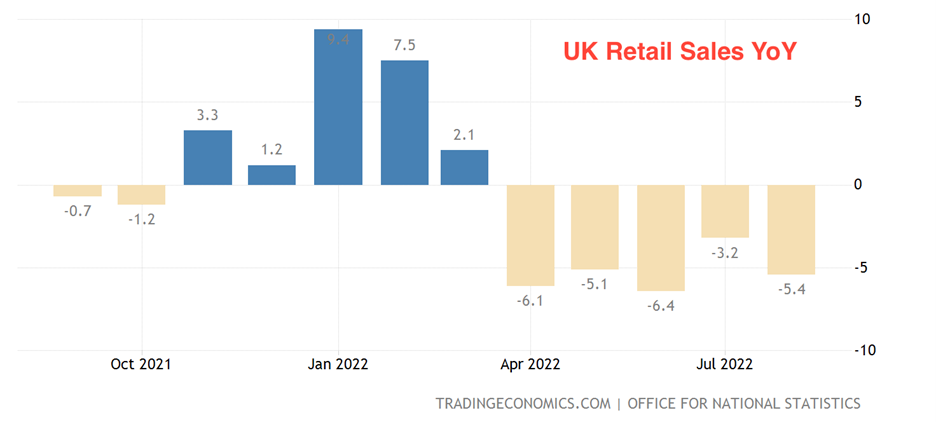

British Pound has been hit badly by gloomy consumption data released today: retail sales plunged by a 5.4% y/y against the forecast of 4.2%, MoM decline accelerated to 1.6% against a much less pessimistic forecast of -0.5%. On an annualized basis, retail sales have been on a slippery slope for the third month in a row:

As a result, GBPUSD broke through the bottom of March 2020 (1.14 level).

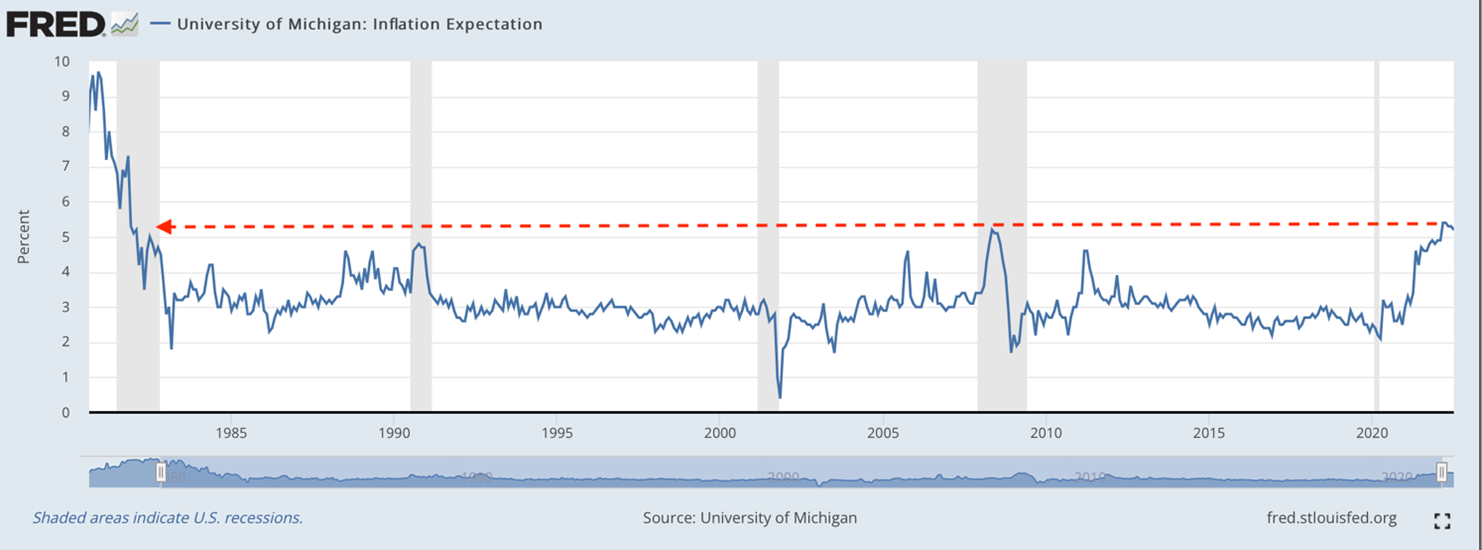

Market focus today is on the index of consumer sentiment from the U. of Michigan. An important component of this report are the inflation expectations. Signs of persistence will strengthen market expectations that the Fed will increase the pace of its monetary tightening. The situation with inflation for the Fed is extraordinary: one-year inflation expectations rose to the highest level since December 1981, which caused concerns of loss of CB credibility and inflation expectationsforcing the Fed to raise the rate at an unprecedented pace:

It is worth noting that bond markets set the bar quite high for the Fed to surprise with a hawkish decision. Investors take flight from risk and buy up the greenback on rumors, however, as it often happens, the market reaction to rumors will likely prove to be too emotional, and facts may trigger a correction. Based on this, the risks are skewed towards a dovish FOMC meeting.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.