Markets are Worried about a Recession and the Trend will only Gain Momentum

The toxic mix of hawkish central banks ready to tighten monetary policy "no matter what" and a series of weak macroeconomic data on the US and European economies has become a catalyst for sell-off in risk assets, rally of bond prices and dollar strength. A growing number of market participants believe that central banks are rushing to raise rates (aka "policy error"), which could, if not cause, then at least exacerbate the course of a possible recession. Looking at the two main asset classes - stocks and bonds, we see a flow from risk assets to safe havens (long-term bonds) - bond prices rise (yields decrease accordingly), and stock prices decline. For instance, the yields of 10-year US and German bonds returned to the level corresponding to the beginning of June:

In the risk assets market, considering the key S&P 500 benchmark, the rebound after the correction to the low since December 2020 did not last long, bearish sentiment again prevailed this week. The sellers may target the 3550-3570 zone, which will correspond to the test of the main bearish trend line:

Given these trends, the demand for the dollar, as a defensive asset, is set to remain high and it is very likely that we will see new highs in the dollar index in the near future:

Consumer spending in the US for the first four months was revised down, and after release of the May report, which indicated a significant slowdown in growth, it became clear that the flywheel of the US economy is starting to slow down. The Fed's policy of raising rates, along with a slowdown in consumer spending, is likely to lead to the fact that economic growth forecasts will become less optimistic, while the risks of a recession will increase.

The report, published on Thursday, contained important positive news for the Fed - the preferred inflation measure for the regulator - the core consumer spending index - eased from 4.9% to 4.7% (4.8% forecast). A decrease in the indicator means that the imbalance between supply and demand has somewhat eased, which means that inflation pressure in the economy is less than expected. The rest was less positive - the nominal monthly growth of expenditures amounted to 0.2% (forecast 0.4%), and in real terms it even decreased by 0.4% (forecast -0.3%). At the same time, the April figure was revised down - from 0.7% to just 0.3%. Along with deterioration of consumption data for the first quarter, the market is coming to the realization that the American consumer was not as resistant to inflation as it seemed.

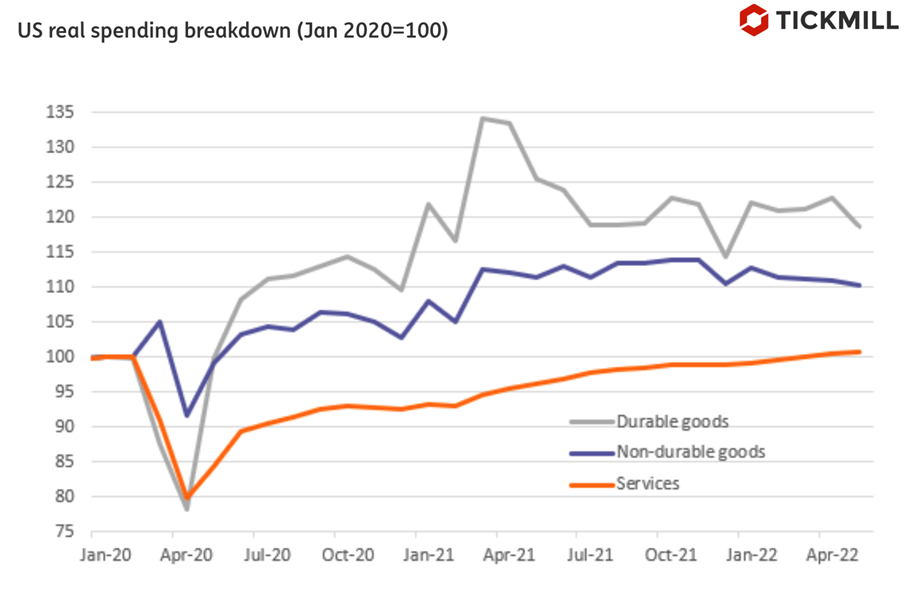

The details show that the indicator of consumption of durable goods behaved the weakest. It sank by 3.5%, while the consumption of non-consumer goods decreased by 0.6%. Service consumption rose by 0.3%, but this was not enough to compensate for the weak behavior of other components.

The component-by-component dynamics of US consumer spending is as follows:

The decline in core inflation is a very good sign, but at 4.7% it is still twice as high as the 2% target. The Fed has signaled that it is ready to sacrifice strong demand to regain control of inflation, so the prospect of high pace of rate hikes is not yet in doubt. After Powell's speech in Sintra, where the head of the Fed announced the good shape of the US economy and the need to reduce inflation, this prospect only became clearer. Other than a strong labor market, there really isn't much to brag about: consumer confidence is at multi-year lows, the housing boom is waning, and fuel prices are likely to remain high. It follows that in the second quarter, the picture of consumption in the US may not be so rosy, and therefore fears of a recession in the fourth quarter of 2022 are likely to only gain momentum.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.