Markets rebound on profit-taking, dollar stalls

The FOMC meeting is due tomorrow and policymakers are expected to lift interest rate by 75 basis points. The odds of a larger rate hike of 100 bps are estimated at 20%. Hawkish US inflation report for August ruled out any possibility of easing the pace of tightening. The Market’s focus will also be on the updated Dot Plot, which are the interest rate expectations of the Fed officials in the short, medium, and long term. The market expects the Fed to complete tightening when interest rate gets to 4.5%, some experts see the peak even at 5%.

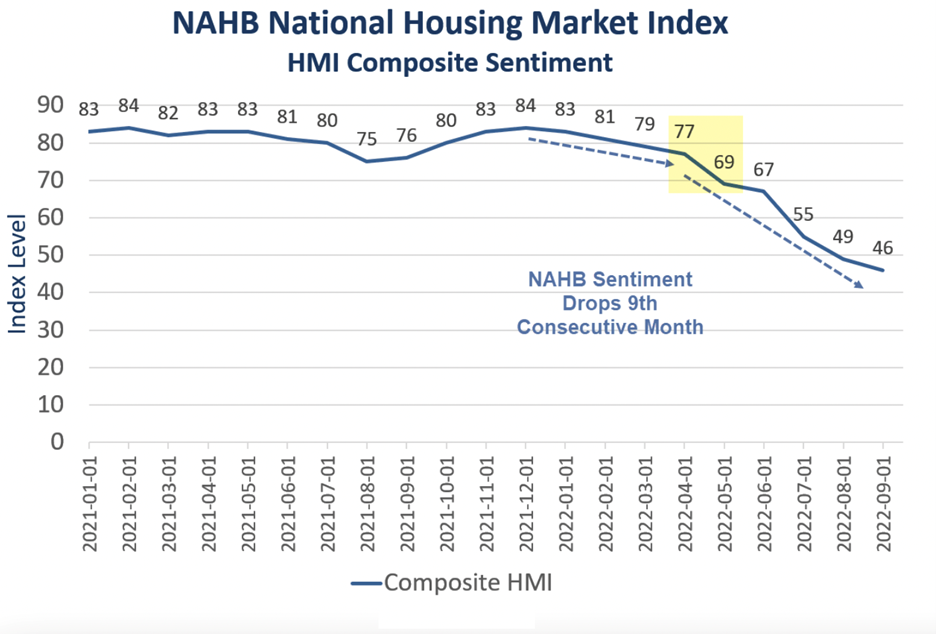

The US NAHB real estate market index fell for the ninth consecutive month in September to 46 points:

Pessimism of US builders rose as monetary tightening pushed up mortgage rates, reducing home affordability, forcing potential buyers to take a wait-and-see approach. Developers are forced to reduce prices (the share of those who announced price cuts was 24%), which should have a favorable effect on inflation soon.

US stock markets closed with gains, Asian markets picked up the baton today, however, before the FOMC, the maximum that can be expected is profit taking on short positions and technical rebound, so the upward movement is limited. The dollar has not decided on the direction and is trading near 110 points on the DXY index. EURUSD is above parity, USDJPY is also trading in a range, the battered pound is recovering slightly more than major opponents, as it has been under especially strong pressure lately due to rising expectations that the gap in the tightening of the Bank of England with the Fed or the ECB will widen, and therefore, local fixed income assets are less attractive. Inflation in Japan has exceeded expectations, is above the target level, but still will not cause a corresponding reaction from the Bank of Japan, which is trailing behind among the largest central banks in the tightening race. The RBA meeting had a negative impact on AUD as the regulator said it plans to slow down the pace of rate hikes. In the US Treasury market, a moderate sell-off continues, with the yield on two-year bond crept close to the 4% mark. Yields are creeping up for the sixth week in a row:

The daily range of oil price movement widened at the beginning of the week, while the intraday change in the price of Brent on Monday was $4 per barrel. On the demand side, there is positive news on Chinese demand as the country eased some more covid restrictions. On the supply side, we can note the news about decision of the UAE to increase output faster - the country plans to increase production to 5 million barrels per day already by 2025 instead of 2030, as announced earlier. The US continues to sell oil from strategic reserves to compensate for the deficit, in November another 10 million barrels will be released on the market. In total, the stabilization plan involves the sale of 185 million barrels, of which 155 million have already been released to the market.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.