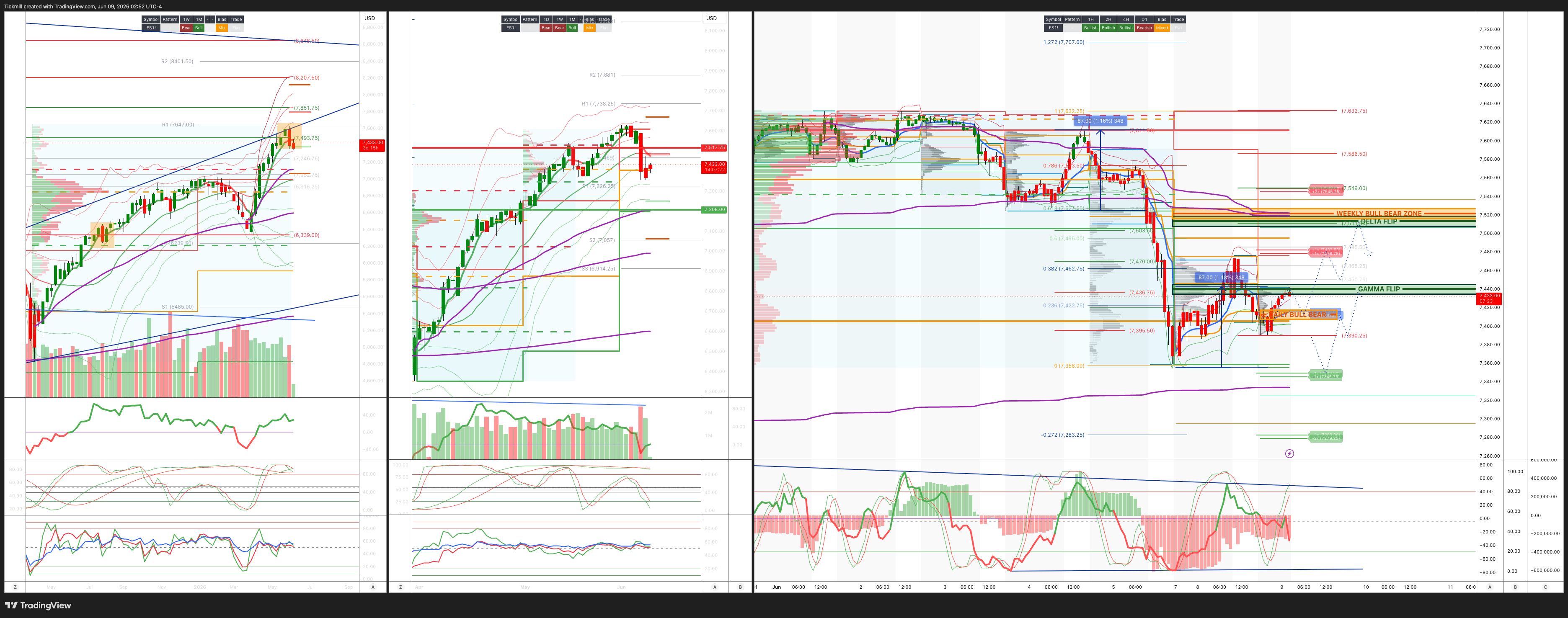

S&P500 Daily Action Areas & Price Targets 9/6/26

S&P500 Daily Action Areas & Price Targets 9/6/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7515/25

WEEKLY RANGE RES 7517 SUP 7208

June MOPEX Straddle: 274pt range implies a OPEX to OPEX range of [7134, 7683]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.09 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BEARISH 7519

WEEKLY VWAP BEARISH 7477

MONTHLY VWAP BULLISH 7036

DAILY STRUCTURE - OTFD 7476

WEEKLY STRUCTURE - BALANCE 7354/7632

MONTHLY STRUCTURE - OTFH - 7199

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7420/10

GAMMA FLIP 7441

DELTA FLIP 7513

DAILY RANGE RES 7479 SUP 7345

2 SIGMA RES 7545 SUP 7279

VIX BULL BEAR ZONE 19

TRADES & TARGETS

SHORT ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET DAILY RANGE SUP

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Summer Famework’

Big-Picture Framework: Bull Market, but Summer Turbulence Likely

The stripped-down market framework is constructive but more tactically cautious. The primary trend remains higher, and the year-end balance of risk still favors the bulls, but the market is entering a more fragile summer trading environment after an unusually powerful short-cycle rally, heavy re-risking by the speculative community, and a growing wave of new equity issuance.

The message is not to de-risk aggressively or abandon the bull market. It is to recognize that the easy part of the rally is probably behind us, that parts of the market are technically and positionally stretched, and that volatility should be owned rather than ignored. The preferred tactical expression is long delta / long vol: stay with high-conviction, liquid longs, but use puts to manage the downside tail.

The Tailwinds

1. Nominal Growth Is Strong and Financial Conditions Are Easy

The US economy continues to show durability. Nominal growth is strong, financial conditions remain easy, and the economy has again proven more resilient than many expected. This matters because bull markets usually struggle when growth is deteriorating and liquidity is tightening. That is not the current backdrop.

Even after hotter payrolls and a repricing toward a longer Fed pause, the economy is not showing clear evidence of buckling. Payrolls were strong, unemployment remains stable, ISM has improved, and earnings have accelerated. The market may not love higher yields in the short term, but strong growth remains a fundamental support for equities.

2. The YTD S&P Rally Has Been Earnings-Driven

The entirety of the year-to-date rally in the S&P has been a function of earnings rather than pure multiple expansion. That is an important distinction. Earnings-led rallies are generally more durable than valuation-led rallies.

History is supportive here: the S&P has been higher in 12 of 13 years following years when EPS growth exceeded 10%. With S&P earnings growth at 27% year over year in the latest quarter, the fundamental impulse is very strong. Even if the second derivative of earnings growth slows from here, the level of earnings momentum remains a major tailwind.

3. Flows Remain Supportive

The broad flow of capital remains highly supportive. US households, the largest owner of the equity asset class, never lost the trail and continue to sponsor stocks. This has been one of the most important features of the cycle.

Retail and household demand, corporate buybacks, systematic flows, and ongoing fund inflows have all helped absorb shocks. Even during sharp factor rotations, the market has not shown broad-based abandonment of equities. Instead, capital has rotated aggressively between sectors and themes.

This is especially important in a market dealing with large issuance. The ability of investors to absorb large offerings, including recent megacap transactions, suggests liquidity remains deep. But that does not mean the absorption process will be smooth.

4. The Capex Super Cycle

The market is living through a once-in-a-generation, and possibly once-in-a-lifetime, capex super cycle. The AI infrastructure buildout is the clearest example: data centers, semiconductors, networking, power, cooling, storage, security, and cloud infrastructure are absorbing massive amounts of capital.

The more bullish interpretation is that this capex super cycle could eventually become a productivity super cycle. If AI infrastructure translates into higher productivity, margin expansion, faster revenue growth, and broader economic efficiency, then the market’s current optimism may be fundamentally justified.

This is the most important structural bull case. It is why investors continue to buy AI-linked weakness, why megacap platforms remain strategically favored, and why the market has been willing to look through geopolitical and rates volatility.

The Headwinds

1. The Rally Was Historically Powerful

The past two months produced one of the greatest short-cycle rallies in modern market history. On a volatility-adjusted basis, it was the best in the past 50 years. That kind of move is very difficult to repeat immediately.

After such an extreme advance, some mean reversion is normal. It does not require a bearish regime shift. It simply reflects the fact that returns were pulled forward, positioning adjusted quickly, and the market became vulnerable to even modest negative catalysts.

The SOX is a good example. The index had not been this far above its 200-day moving average since early 2000. That does not mean the AI/semi trade is “2000 all over again,” but it does mean the short-term technical setup had become stretched enough to justify caution.

2. Speculative Risk Has Been Added, Often in Levered Formats

The trading community has already added a lot of risk. Much of that risk has been in levered formats, and much of it has been concentrated in a narrow set of high-velocity names. This includes AI infrastructure, semiconductors, non-profitable Tech, quantum, drones, space, crypto-sensitive equities, and other momentum-heavy pockets.

When risk is concentrated in high-beta, high-velocity expressions, the unwind can be violent even if the broader market remains healthy. Friday’s tape was a good example: NDX and SOX were hit hard, but S&P ex-AI was roughly unchanged. That is factor stress, not necessarily systemic equity stress.

The additional complication is new issuance. A set of new deals is coming off the assembly line, and the market needs to fund them. That can create selling pressure in liquid winners, especially megacap Tech and Semis, as investors raise cash for new opportunities.

3. Earnings Growth Is Strong, but the Second Derivative Is Harder

S&P earnings growth of 27% year over year is a major bull-market support. But after such a strong quarter, it is fair to question the sustainability of the second derivative.

The issue is not whether earnings are good. They clearly are. The issue is whether earnings acceleration can continue at the same pace. Markets often struggle when the level of growth remains strong but the rate of improvement slows, especially if valuations and positioning already discount exceptional outcomes.

This is especially relevant for AI and semiconductors, where the bar is extremely high. AVGO’s post-earnings weakness showed that even a good result may not be enough if expectations are elevated.

4. Iran, Oil, Inflation, and the Fed

The war with Iran remains a key macro headwind. As long as the conflict drags on, oil risk remains elevated, and inflation remains clearly above target. That is an inconvenient truth for the Fed and a problem for real household income growth.

Higher oil and tariffs complicate the inflation picture. Hotter payrolls and firm wage growth complicate it further. The Fed may not need to hike, but it may need to stay on pause for longer than markets would like. That creates a tougher backdrop for long-duration growth and high-multiple momentum.

The key is rates volatility. Equities can live with elevated yields if the move is orderly. They struggle when rates vol rises abruptly. If CPI or oil drives another disorderly move higher in yields, equity turbulence could continue.

Where This Framework Lands

1. It Is Still a Bull Market

The primary trend remains higher. The house call is for a continued rally to the 8,000 level on the S&P 500. That is the big ball: the bull market is intact, earnings are strong, flows are supportive, and the AI/capex cycle remains a powerful structural force.

Near-term corrections, factor rotations, and volatility shocks should be viewed within that broader uptrend unless the macro or earnings regime changes materially.

2. Mean Reversion Is Already Underway in Stretched Pockets

Locally, a patch of mean reversion should be expected. It may already be underway in several areas. The SOX had become extremely extended versus its 200-day moving average, speculative communities had re-risked aggressively, and much of the exposure was concentrated in high-velocity trades.

Korea dropping another 8% overnight is another example of how global speculative and Tech-linked exposures can reset quickly when positioning becomes crowded. These moves can be sharp, gap-driven, and uncomfortable, even while the broader bull market remains intact.

3. Summer Trading Conditions Should Bring Turbulence and Gaps

The year-end balance of risk favors the bulls, but summer trading is likely to be choppier. Liquidity can be thinner, event risk remains high, and the market has multiple catalysts to digest: CPI, Fed blackout, ECB, OPEC, Iran headlines, tariffs, IPO issuance, SpaceX, AI conferences, software events, and continued megacap supply.

That argues against complacency. The market can move higher, but the path is unlikely to be smooth.

Tactics of Navigation

1. Prefer Long Delta / Long Vol

The preferred framework remains long delta / long vol. In practice, that means staying invested in high-conviction longs while adding convex protection against drawdowns.

This is a sensible structure because the base case remains bullish, but the tails are underpriced. VIX and VVIX have been low, skew in some high-risk areas has been cheap, and the market has been slow to price the possibility of liquidity shocks from issuance, geopolitical headlines, or rates volatility.

2. Stay With Highest-Conviction, Most Liquid Longs

The idea is not to own everything. It is to stay in the pocket with the highest-conviction and most liquid longs. Liquidity matters because summer gaps and issuance-related rotations can punish crowded, illiquid positions.

High-conviction longs can still include parts of AI, capex, semis, security, data infrastructure, Financials, Health Care, Industrials, and select cyclicals. But the position sizing and entry points matter more now than they did during the straight-line rally.

3. Use Puts as Functional Downside Protection

A three-month, 25-delta S&P put costs less than 2% of spot, making it a liquid and functional hedge. That is the kind of protection that fits this environment: not a bet on collapse, but an insurance policy against air pockets.

This is particularly relevant because the market’s downside risks are more about gaps and tails than slow deterioration. A hot CPI print, Iran escalation, oil spike, failed IPO absorption, or another AI narrative shock could produce sharp moves. Puts help maintain long exposure without being forced to sell into weakness.

4. Pair Equity Length With Short Global Fixed Income

The framework also keeps the view that equity length should be married with a short position in global fixed income. The logic is straightforward: nominal growth is strong, inflation remains above target, and central banks may need to stay restrictive for longer.

If growth remains strong and rates move higher, the equity side can still work through earnings, cyclicals, and nominal revenue growth, while the short fixed-income position helps offset duration pressure. If rates volatility spikes too abruptly, puts provide protection for the equity side.

The big-picture market call remains bullish, with the S&P still expected to move toward 8,000. The structural supports are strong: durable nominal growth, easy financial conditions, earnings-driven equity gains, supportive household flows, and a massive AI/capex super cycle.

But the short-term setup is less forgiving. The rally was historically powerful, Tech and Semis became technically extended, speculative risk was added aggressively, new issuance is coming, earnings acceleration may be harder from here, and Iran/oil/inflation keep the Fed constrained.

So the right stance is not bearish. It is constructively hedged: stay long the bull market, rotate away from the most crowded high-velocity exposures where appropriate, and own downside convexity. Summer can still end higher, but it is likely to bring turbulence, gaps, and mean reversion along the way

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!