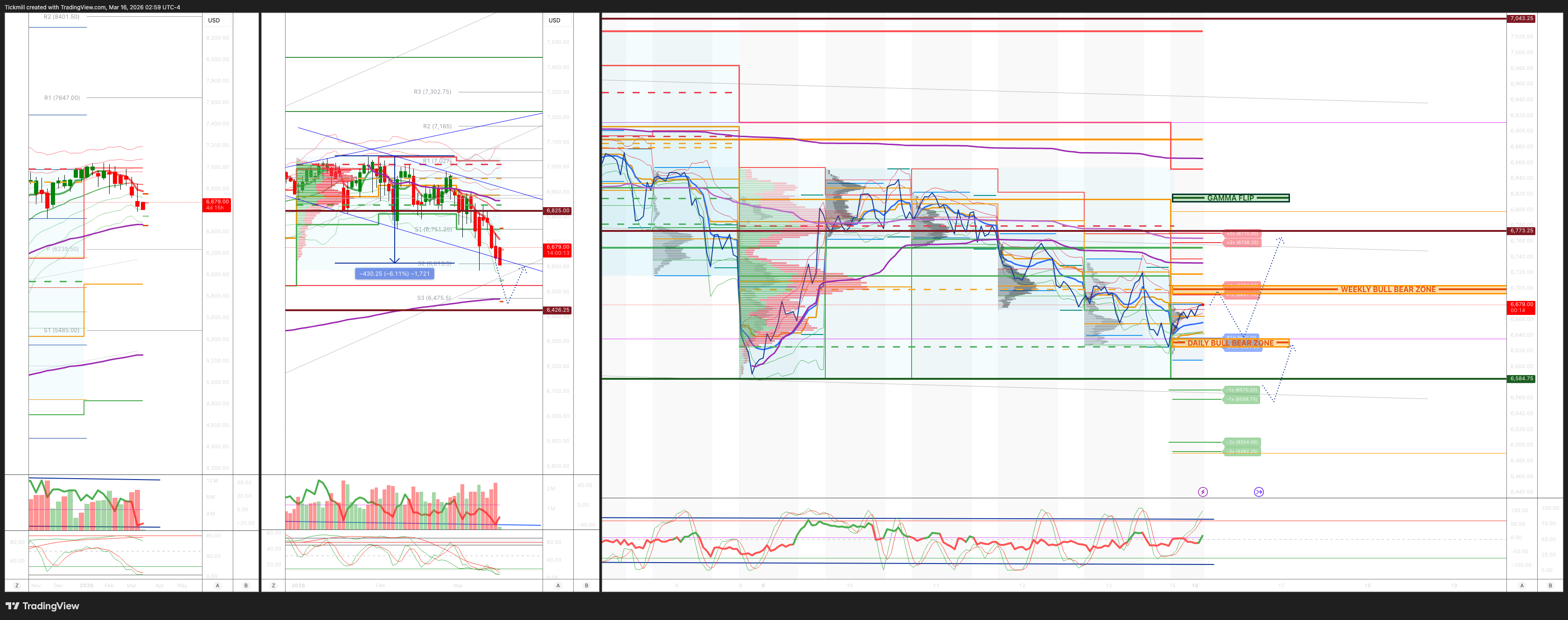

SP500 LDN TRADING UPDATE 16/3/26

SP500 LDN TRADING UPDATE 16/3/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 6700/10

WEEKLY RANGE RES 6825 SUP 6426

Weekly Straddle Range: 199 -point straddle implies a weekly range of [6426, 6824]; monitor 1.5x and 2x moves for key reactions.

March OPEX Straddle: 232.8-point range suggests OPEX-to-OPEX movement between [6677, 7142].

March QOPEX Straddle: 368.55-point range projects [6466, 7203], based on December OPEX.

March EOM Straddle: 255.4-point straddle indicates a monthly range of [6623, 7101]. .

DEC2025 to DEC2026 OPEX straddle spans 945 points, outlining a range of [5889, 7779]."

DAILY VWAP BEARISH 6711

WEEKLY VWAP BEARISH 6777

MONTHLY VWAP BEARISH 6869

DAILY STRUCTURE – OTFD - 6737

WEEKLY STRUCTURE – OTFD - 6852

MONTHLY STRUCTURE - OTFD

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFD): This describ@es a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 6625/35

GAMMA FLIP 6821

DAILY RANGE RES 6703 SUP 6570

2 SIGMA RES 6770 SUP 6504

VIX BULL BEAR ZONE 20

PUT/CALL RATIO 1.22 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

TRADES & TARGETS

SHORT ON REJECT/RECLAIM OF WEEKLY BULL BEAR ZONE TARGET DAILY BULL BEAR ZONE

LONG ON ACCEPTANCE ABOVE WEEKLY BULL BEAR ZONE TARGET 6750

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

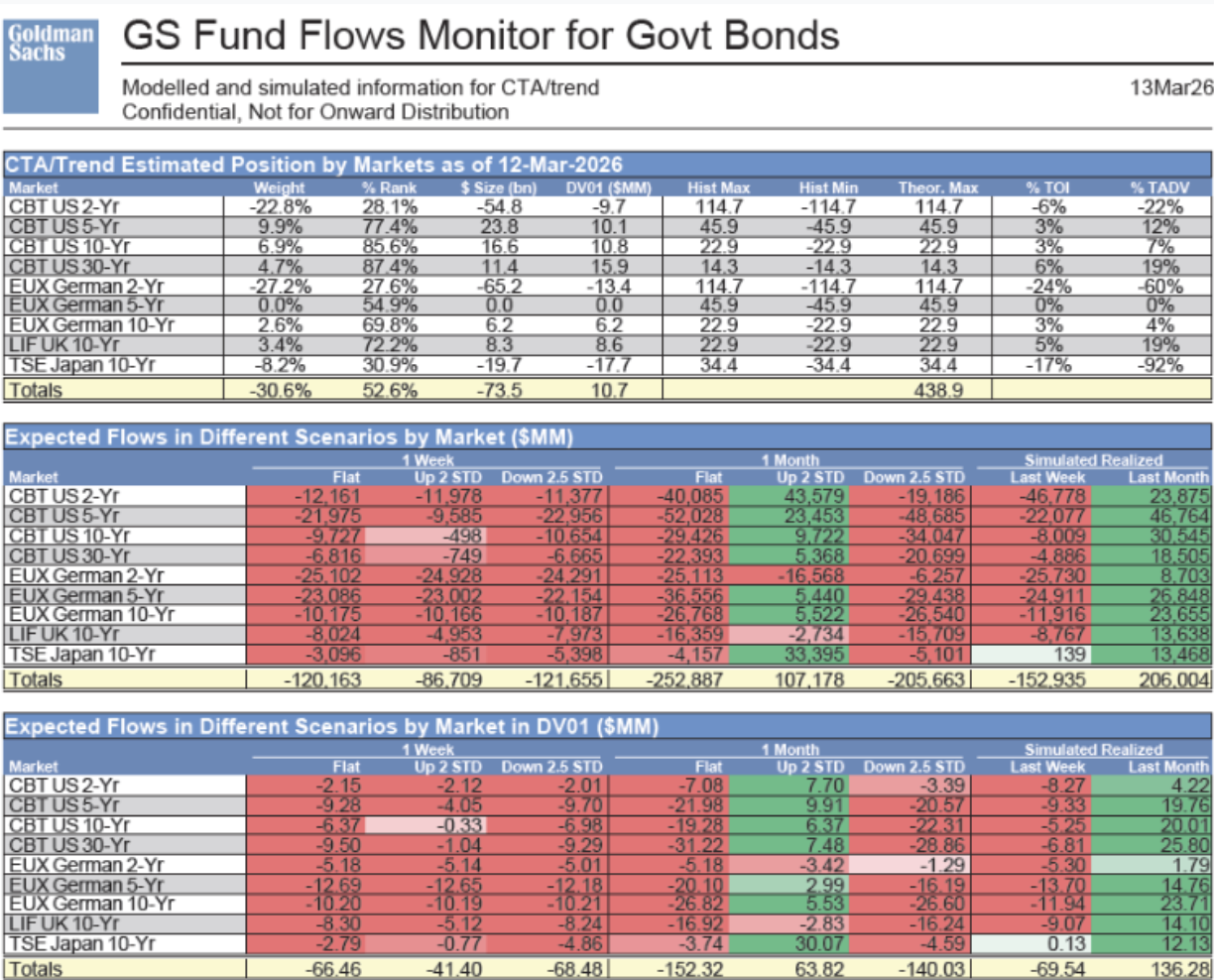

GOLDMAN SACHS TRADING DESK VIEW - ‘Week Ahead’

The Week Ahead from the Futures Desk (Week of March 16th)

Key Events to Watch This Week:

- March 16th: US Empire Manufacturing, Industrial Production, Canada CPI

- March 17th: Italy CPI, German ZEW Current Situation, UK Supply, US Pending Home Sales, 20-Year Auction

- March 18th: Eurozone CPI, German Supply, PPI, FOMC Meeting + Powell Speech

- March 19th: BoE Rate Decision, SNB Rate Decision, Eurozone Labor Costs, ECB Rate Decision + Lagarde Speech, European Supply, Philly Fed Index, Initial Jobless Claims, New Home Sales, 10-Year TIPS Auction

- March 20th: German PPI, Eurozone Trade Balance, ECB’s Nagel Speech, Canada Retail Sales

Market Recap and Key Focus Areas:

Last week, markets remained fixated on the escalating conflict involving Iran, with particular attention on developments around the Strait of Hormuz. Historically, renewed tensions in this critical chokepoint have led to higher oil risk premiums, amplifying inflationary concerns and triggering bear-flattening pressure in European rates. While the U.S. market initially showed resilience, it too experienced bear-flattening as the week progressed.

The inflationary impact of rising oil prices has been widespread. Markets are now pricing in approximately 47 basis points of rate hikes in Europe, 24 basis points in the UK, and 23 basis points of rate cuts in the U.S. by year-end. Credit markets also showed signs of strain, particularly in private credit, as highlighted by reports of institutions like JPMorgan marking down loans held by private credit groups (source: Financial Times).

The market has largely moved past last Friday’s weaker payroll data (negative NFP), with attention now squarely on inflation risks stemming from the potential disruption or uncertainty surrounding Hormuz. Over the weekend, key headlines included:

- “Trump asserts Iran wants to end war but Tehran says no proposal”

- “Wright says U.S. in talks with some nation on reopening Hormuz”

- Financial Times: EU ministers to discuss possible naval options for the Strait of Hormuz

Outlook and Scenarios:

The market currently finds itself at a crossroads, influenced by two opposing forces:

1. Sustained Elevated Oil Prices and Disruption Risk: Continued tension and elevated oil prices are likely to maintain bear-flattening pressure across markets.

2. Potential De-escalation or Agreement: A credible resolution or a clear path to reopening the Strait of Hormuz could unwind oil-driven inflation premiums, potentially triggering a bull-steepening move.

Finally, our CTA model has shifted to a seller stance across scenarios, with positioning remaining short on U.S. and German 2-year notes.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!