Strong March NFP Suggests more US Data Surprises to come

The US jobs market data in March were really impressive. Given momentum effect in the labor market and still incomplete recovery in consumer mobility, payrolls growth April may top 1 million. It means the odds of more economic surprises in the US from the key macroeconomic areas are quite high, which justifies elevated market expectations about US assets and USD performance. We cannot rule out that US labor market can achieve pre-pandemic levels by the end of the year which will certainly trigger premature Fed tightening. For now, it remains a tail risk.

The solid report on the US labor market for March indicated the growth of jobs by 916K against the 660K forecast. The payroll readings for the previous two months were revised upwards by 156K. Employment in the private sector rose by 780K, while the currently not very indicative unemployment rate fell to 6%.

Employment growth overtook the forecast thanks to warm weather which additionally boosted mobility and some economic sectors like construction, strong vaccination program in the US and economy reopening efforts from individual states, which boosted consumer sentiment, business climate, activity and labor demand.

Improved weather helped construction sector to boost hiring by 110K, continuing easing of restrictions led to an increase in jobs by 280K in the leisure and hospitality industry. Public sector employment increased by 136K. However, in no industry has demand for labor recovered to pre-crisis levels.

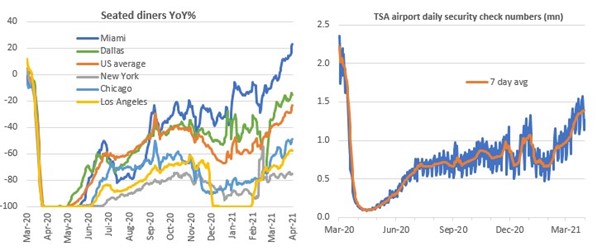

Expectations for the jobs market performance in April are high due to two reasons. Firstly, consumers mobility still has room to recover. Secondly, it’s reasonable to expect that recovery will continue given positive trend in reopening and non-stop supportive government measures. The following shows the dynamics of restaurant reservations for some key states, as well as the number of security checks at airports:

Source: ING

It can be seen from both charts that all the curves (with the exception of Miami table reservations) are still below the pre-pandemic level, so recovery still has a room to go. Consequently, the demand for labor should continue to grow.

Despite the positive NFP update, there are 8.4 million fewer jobs in the US economy than it was before the pandemic. The Fed has signaled that it will not raise rates until 2024 until there is substantial economic progress. Given their lukewarm attitude towards rising inflation, it is clear that they want to see jobs return to pre-crisis levels.

Officials' comments make it clear that unemployment is now giving false signals due to the large number of demotivated workers. Now only 57.8% of the working population is employed. This is very low and, in some respects, comparable to the employment rate of the 1980s. To reach pre-crisis levels (labor force participation rates above 60%), the labor market should add at least 6 million jobs.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 65% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.