US August Inflation: More Price Gains Ahead but not Enough for September Fed Policy Shift

US price pressures somewhat receded in August, reflecting mainly the cooling off in consumption hot spots which emerged after the lifting of social restrictions. These spots featured abnormal rise in prices, primarily driven by temporary factors, such as supply chain disruptions and bottlenecks and pent-up consumer demand. Overall, inflation has become more even, affecting more goods and services, while inflation expectations ticked higher, which may worry the Fed.

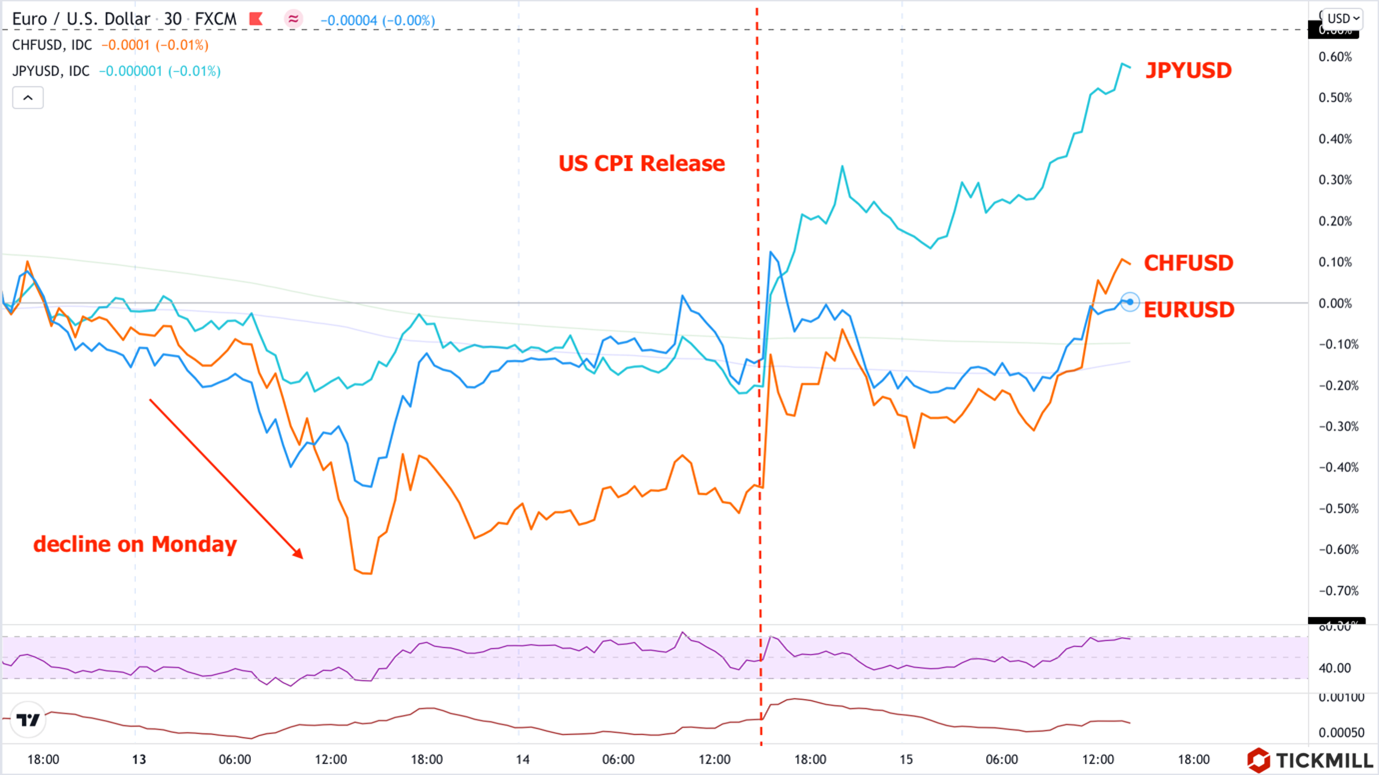

US consumer prices increased by 0.3% MoM, which is slightly below the forecast of 0.4% while core inflation, which has higher significance for the Fed's policy, added just 0.1%, falling short of 0.3% expectations. The easing of core inflation was apparently the primary reason for disappointment and triggered sell-off of the US currency on Tuesday. Today sellers renewed pressure on the dollar while US bond yields trimmed down recent gains.

Considering contribution of individual categories of goods and services, it can be seen that there is strong MoM deflation in the components, where prices have been recently rising at abnormal rates. Airline prices dropped 9.1%, used cars fell 1.5%, car and truck rentals tumbled 8.5%, and hotel bookings dropped 3.3%. These changes in prices basically made the key main contribution to the August slowdown in inflation.

The NFIB's report on firms' decisions to raise / lower / hold prices calls into question the prospects of easing of inflation in the near future. According to the latest data from the agency, 49% of enterprises are raising prices, and 44% expect to make additional price hikes in the future. Both are at their highest level in 40 years. This important indicator of inflation was also mentioned by the Fed in the latest release of the Beige Book, which suggests that the US Central Bank takes these data into account as well.

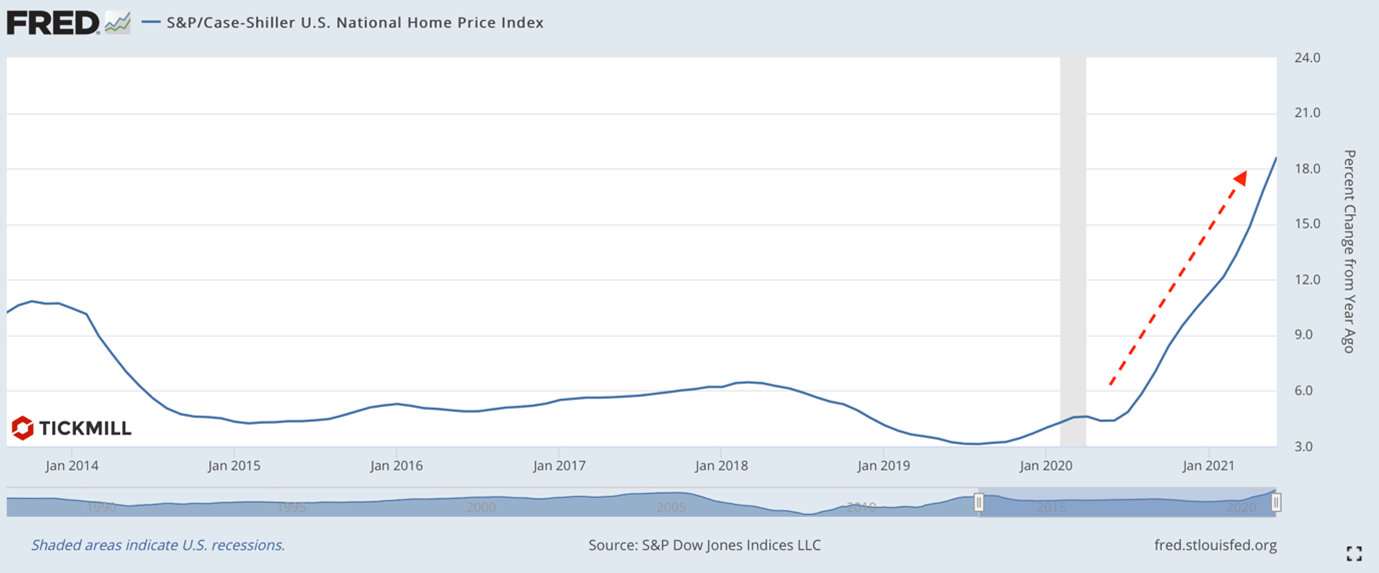

Another reason to expect persistence of inflation is the rise in house prices. In the United States, the dynamics of housing rent is about a year and a half lagging behind changes in real estate prices, given their sharp rise in 2021, rents’ upward adjustment in the future will likely lead to higher consumer inflation:

On Friday, there will be data on consumer inflation expectations from U. of Michigan. The latest reading is 2.9%, however, if inflation expectations rose again in August, the Fed officials may start to mull over the need to communicate a chance of a rate hike next year, since one of the main goals of the Fed's policy is to not let inflation expectations drift from their inflation goals. Given that firms are still willing to transfer rising costs to consumers after positive experience with the pent-up demand, higher expectations of inflation US households may be quite justified, which may eventually trigger some Fed response.

However, in the FX market, the bets for the Fed's early move towards policy tightening seems to be decreasing. On Wednesday, we see that the dollar suffers the biggest losses in pairs with EUR, CHF, JPY - by 0.24, 0.38 and 0.39%, respectively. On Monday, before the release of the CPI, the opposite trend was observed - the dollar posted the largest gain against these currencies:

Takentogether, these phenomena may indicate an inflow and then an outflow ofinvestors from countries with low interest rates on expectations that the Fedwill begin to tighten policy and raise rates on Treasury securities andsubsequent disappointment after release of the August CPI.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.