US eco surprises gain momentum signaling Dollar has more room to rally

January US CPI released on Tuesday was broadly in line with market expectations. Core and headline inflation were higher than expected, but given exceptionally strong Payrolls (+500K jobs in January) it was pretty clear that the CPI was likely to surprise on the upside, which is exactly what happened. Surprise in the CPI still left a mark on the market, the US Treasury yield traded on Wednesday at a higher level than before the release of the report (up about 4 basis points), US futures remained on a slippery slope. Gold price fell today by 1% to $1835 per troy ounce and, in fact, erased gains made this year:

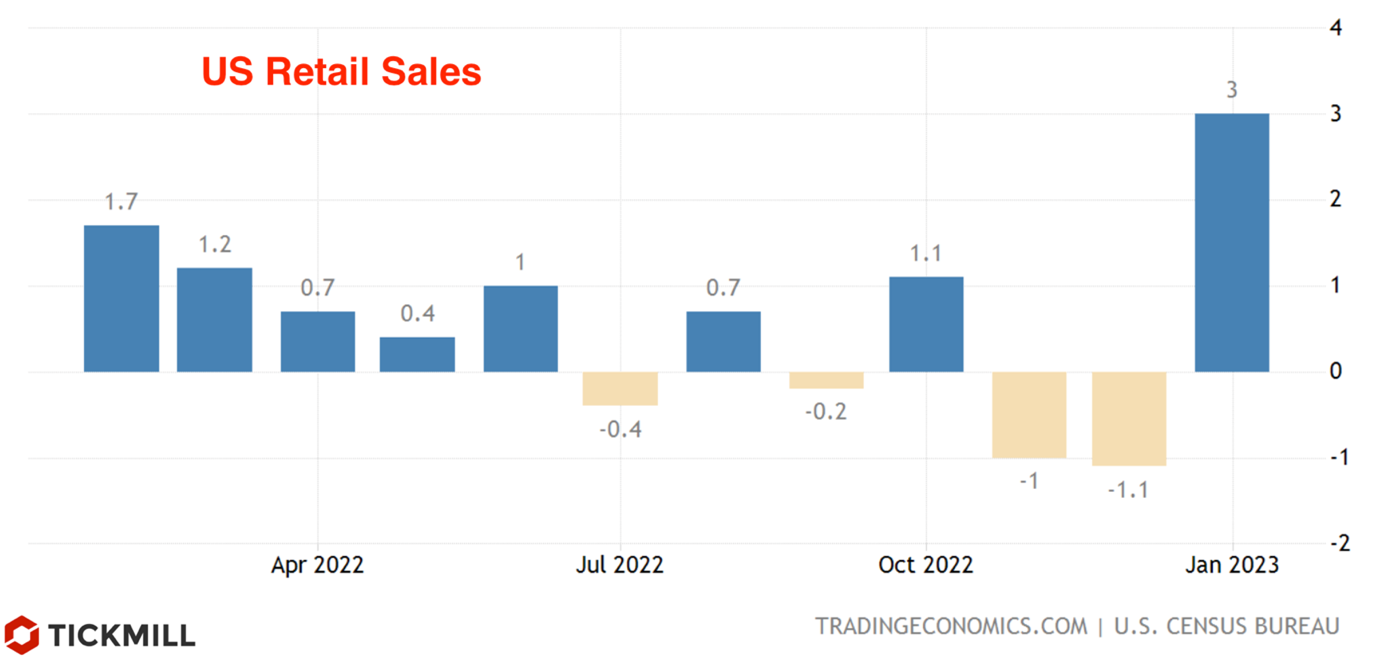

Currencies of the G10 and EM countries extended decline against the dollar on Wednesday after release of the US Retail Sales report, which substantially beat expectations. Broad retail sales jumped 3% YoY, with core sales growth nearly triple the forecast at 2.3% vs. 0.8% expected. The Empire State manufacturing index also showed a significant improvement, rising from -32.9 to -5.8 (forecast -18):

If a single Payrolls report or a single strong CPI print could still be attributed to a statistical outlier or influence of some unique one-time factors, then a significant improvement in three macro parameters at once (employment, inflation, consumption) is very difficult to ignore. Today, the market got another evidence that the US economy growth rate could reaccelerate in January. This is probably not the development that the Fed projected (2023 will be “the year of lower inflation” according to Powell), so the risk of policy adjustments by the Fed, is growing. Since the market is living with expectations, we are already seeing the corresponding reactions. Bond rates are creeping up (the 10-year rate is at a maximum since the beginning of the year), and the main US stock indices are consolidating in inclined (SPX, NASDAQ) or horizontal (DOW) channels, signaling that the wait-and-see stance becomes a dominating mood. The dollar is quickly regaining its "former glory" for itself, gaining about 3% since the beginning of February. Today, the Dollar is rising against all major currencies and currencies of emerging markets. The technical picture of the dollar index deserves consideration, where a rather interesting situation has formed. After a rebound in early February, the price consolidated for about a week in an oblique flag pattern, a classic trend continuation pattern. Today, there was a breakout following retail sales report release and now the target may be a large horizontal resistance level 105.50-106:

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.