US Yields are About to Bottom Out

The dollar starts off the week on a weaker footing, however there is a great chance that bearish pressure will ease as we get closer to Friday. At the meeting last week the Fed left the door open for rumours about a hawkish policy shift in August and the key missing piece that may boost the odds of such an outcome is an upside surprise in the NFP report this Friday.

The number of new jobs created in the economy (aka Payrolls) has taken center stage in the post-pandemic period in terms of impact on the Fed decisions. It is expected to post decent 900K gain. Stronger-than-expected Payrolls reading will likely fuel speculations that the Fed will hint about QE tapering during Jackson Hole Conference in August. In this case, the market will start to price in decreasing demand in the Treasury market (as a result of slowing Fed purchases) and given the passage of Biden infrastructure plan, which will be financed with new debt, investors may start to quit Treasuries en masse.

Recall that long-term Treasuries saw a strong rise in demand over the past two months (yield-to-maturity slid from 1.75% to 1.20%), however, neither weakening of global economic expansion, nor increased covid-10 risks, which were cited as primary catalysts of the move, didn’t started to materialise. According to JP Morgan, investors continue to fit bearish narratives into the Treasury bond rally similarly to the situation when they explained the Treasury sell-off caused by the actual rebalancing of Japanese investors before the end of the fiscal year (when the 10-year Treasury yields rose from 1.0% to 1.75% in 1Q) by sharply increased inflation expectations and growing risks of economy overheating. The investment bank points to the interesting fact that the latest slump in bond yields was not accompanied by a corresponding increase in open interest in Treasury futures, that is, investors did not make new bets on the deterioration of economic situation, but only adjusted the previous ones.

The sell-off in long-dated Treasuries earlier this year was accompanied by rebound in the dollar index from 89.5 to 93 points. The new wave of Treasury bond sales will most likely also provide strong support to the dollar.

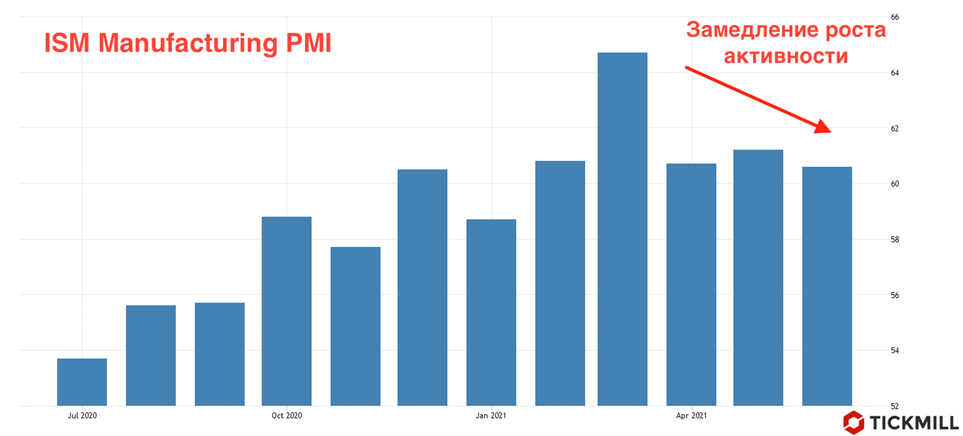

Preparations for this week's NFP report kicks off with today's ISM and Markit Manufacturing indices of activity. It is especially interesting to look at the dynamics of the sub-indices of employment and prices - the first will tell you what to expect from the NFP in the production sector, the second - whether the effect of delays and supply bottlenecks, as well as excessive strong demand, which slow down the economy, are disappearing. The key indicators of the report are expected to extend rise, i. e. the rate of expansion of activity in the sector remained positive in July. A weak report, in my opinion, will have a material impact on the market and will likely fuel more USD downside.

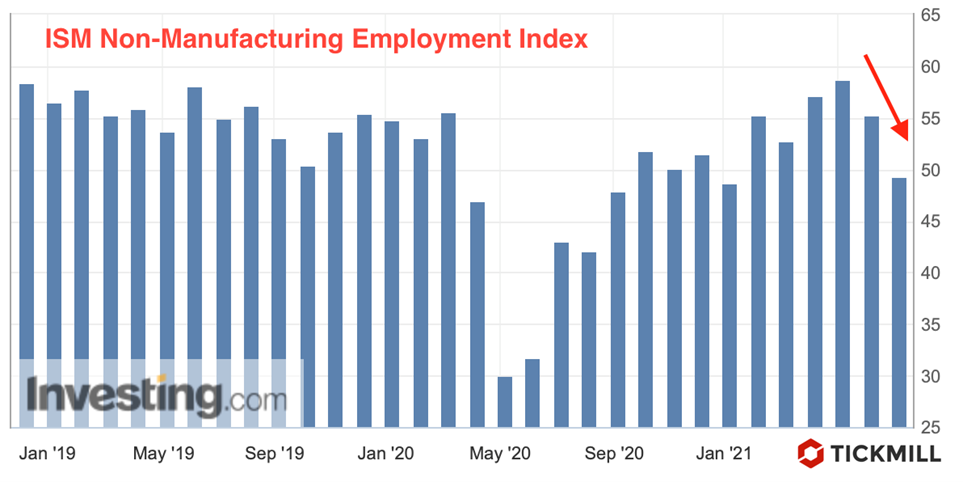

The ADP report and non-manufacturing PMI from ISM are due Wednesday. This time ADP lays down a more conservative estimate of job growth - only 700K (versus 900K NFP). Also pay attention to the hiring component of the ISM index - last month it was in the depressed zone and it is essential to see a rebound to expect strong NFP figure. The greenback are risk assets are expected to post pronounced reaction on release of the reports.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.