What Can We Expect on the ADP Report Today? Medium-Term Analysis of NZUSD

The NZD rose nearly half a percent against greenback after data released Wednesday showed that New Zealand's unemployment rate returned to the record low level that it was at before the virus outbreak. The share of unemployed fell from 4.6% to 4.0% in July, well ahead of the modestly positive forecast of 4.4%. Wage growth rate advanced to the highest level in 13 years, which indicates a strong increase in pro-inflationary risks and likely to prompt a hawkish intervention of the Central Bank. The RBNZ is expected to raise the rate at the upcoming meeting, however, the upside potential of the NZD is far from being exhausted. Especially as there is a risk of a large rate hike by 50 bp at once, as well as the risk that the Central Bank will not rule out the possibility of more rate hikes, which could form sustainable bullish sentiment on the NZD.

From the point of view of technical analysis, the bullish scenario for the NZD can be supported by the following observations. On the weekly NZDUSD chart, we can see a wedge pattern; the formation of which began at the end of last year and continues today. The wedge has a negative slope relative to the main bullish trend, therefore it can be considered as a trend continuation formation. On a larger scale, the idea of a trend continuation looks even more plausible because the multi-year peaks are still far away:

In the past few weeks, NZDUSD has been indecisive, which can be concluded from the shape of weekly candlesticks that had long tails and small bottoms - intra-week fluctuations were characterized by both up and down movements with a slight advantage for sellers:

The bounce from the lower bound of the pattern two weeks ago and expectations regarding RBNZ decision which warrant sustainable upside sentiment suggest that bulls may venture a test of the upper bound of the pattern in the area of 0.7150-0.7170 in the coming weeks.

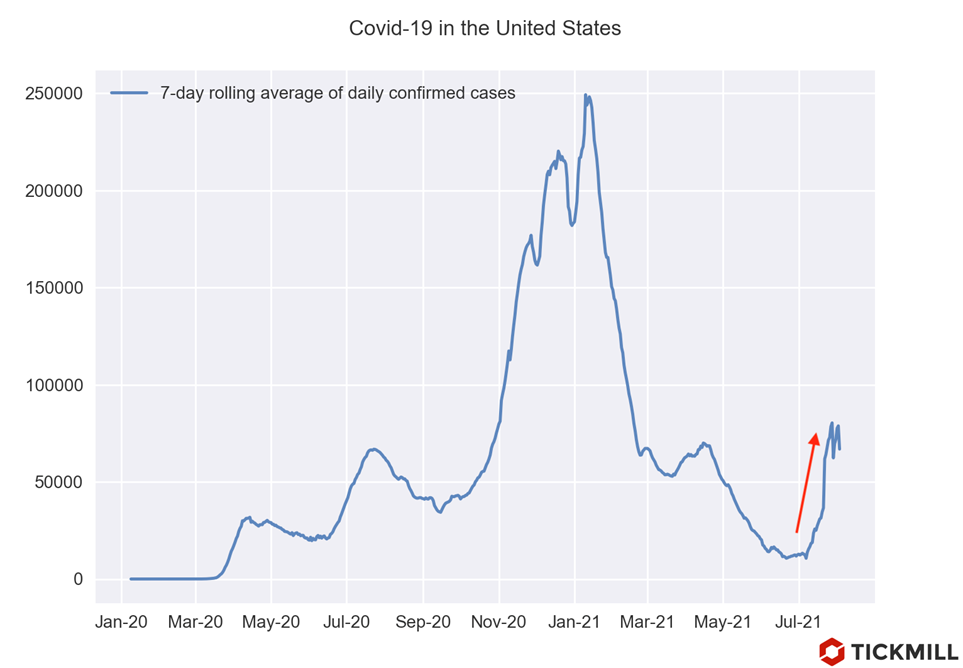

On Wednesday, the dollar is trying to maintain the edge ahead of release of the first batch of labor market data for July - ADP report and ISM report on activity in the services sector. The situation in the manufacturing sector, as shown by a series of data earlier this week (ISM, factory orders, equipment spending) suggests contribution of the sector to the growth of payrolls in July likely beat forecast. However, the share of employed in mfg. sector in the total employment is relatively small, so the ISM report in non-manufacturing sector is much more important in preparing for the NFP. Employment in services sector is now highly subject to fluctuations induced by swings in consumer mobility and social restrictions. Let’s be careful here, since it was in July that the incidence of Covid-19 began to rise in the United States:

Correlation of covid daily cases growth with severity social restrictions is gradually weakening, but this process is slow, so rising incidence in the US in July could still have a drag on creation of jobs due to the pressure on services sector. A negative surprise in ADP and ISM is likely to trigger a wave of dollar sales as it would become more difficult to expect a strong NFP, which is the key report for predicting the Fed's policy move in August.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.