What to Expect From the Fed Meeting this Week? Technical Setup in EURUSD.

Despite the shocks associated with local COVID-19 outbreaks and calm summer season, stock markets find the strength to reach fresh peaks. On Friday, SPX broke through resistance at 4400 as the US economic data and expectations regarding the Fed meeting favored the risk-on move. On Monday, there was a slight pullback that affected all major asset classes. Longer-maturity bonds saw increased demand while risk appetite somewhat eased. Emerging market and commodity currencies stayed under pressure while oil price failed to score additional gains. Gold rebounded. USD stayed offered which is somewhat unusual when combined with broad weak equity performance, however the sell-off could be due to the uncertainty about upcoming Fed meeting, where Powell may disappoint fans of tight monetary policy if he again focuses on employment challenges in the US.

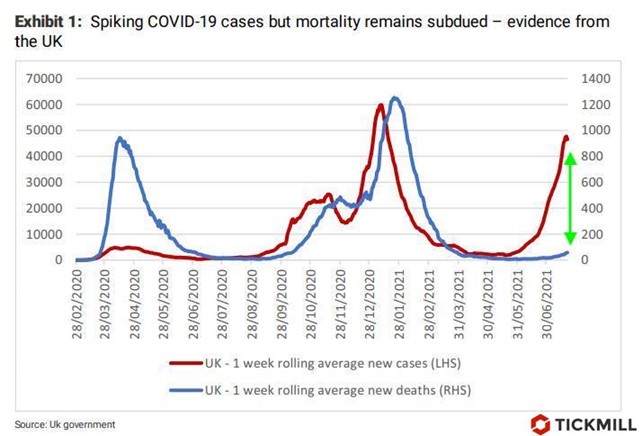

The correction last week failed to gain momentum as the key selling trigger - local COVID-19 outbreaks and associated potential economic setback - quickly proved to be unsustainable. Markets were fast to discount the gloom as several data sources indicated growing evidence that correlation between growth of daily cases and deaths weakened, especially in countries with high vaccination

rates:

The decision of the UK to announce complete lifting of restrictions, despite the surge in incidence, did not seem very far-sighted and even provoked a negative reaction in the GBP, but now the authorities' calculation is clear.

What we need to know before the July Fed meeting? According to the new concept of monetary policy, the Fed will do its utmost to strengthen employment, more precisely to increase its inclusiveness - to involve in work as many people as possible, including people from vulnerable groups. Willy-nilly, the Fed will have to sacrifice price stability, i.e. let inflation fly over the 2% target in this economic cycle. With 6 million fewer employed compared to the pre-crisis period, despite an impressive rebound, the Fed has very little incentive to respond by raising rates to increased inflation rates provided it is seen as temporary. Any, even the slightest hint of a faster monetary policy tightening is likely to lead to a sell-off of risk assets, large USD and Treasury gains as additional hawkish Fed shifts after very hawkish dot plot update in June seem unlikely.

In case of a dovish stance of the Fed at the meeting on Wednesday, the divergence of policies of the Fed and the ECB should weaken a little and EURUSD may have a chance to recoup losses in August. From the point of view of technical analysis, on the daily EURUSD chart, one can consider the falling wedge pattern, which in the classical literature is considered as a reversal formation. Possible entry points for a long can be 1.17 (1) and 1.175 (2):

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.