Why Stock Markets Thursday Fall is a Good Buying Opportunity

Consolidation of 10-year US bond yields around 1.30% turnedout to be a short-lived market state. On Thursday, the yield surged to +1.55% areawhich brought about a massive knee jerk reaction in risk assets. Investorsdumped tech shares with Nasdaq erasing 3.52% of its market cap and SPX losing2.45% of its value. Aggressive selling began right after the NY opening onThursday:

On Friday, there are signs of modest downside pressure remaining - European equities trade in the red, futures on US stock trade near the opening exhibiting some correlation with Thursday returns.

What is really important that the outflow from bonds (which led to steep rise in yields) is not limited to the US Treasury market and is a global phenomenon - the yields of German, Japanese, Australian bonds are rising as well, despite yield curve control efforts from the BoJ or the ECB:

The chart shows that expectations of quickening inflation pace and, to a lesser extent, rise of real interest rate are also driving factors in other developed economies, which is the cause of outflows from fixed income instruments.

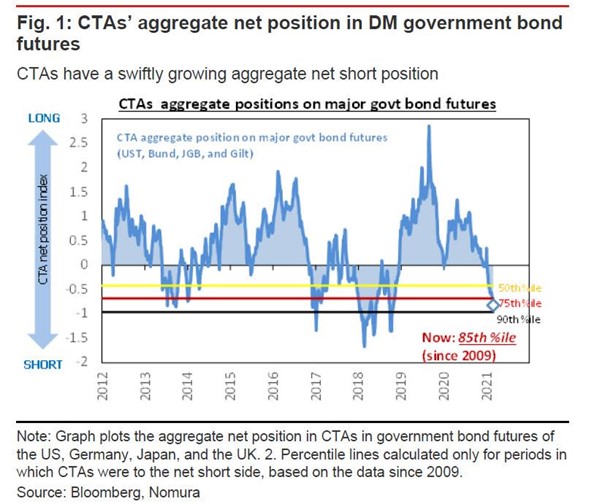

How long will the bond outflow last and weigh on equities? It’s difficult to give precise answer, but CTA futures positions on major government bond futures show that net short increased to 85th percentile:

In other words, only in 15% of cases since 2009, net short exceeded the current level. Therefore, from a technical point of view, investors should be tempted to buy the dip as the sell-off is quite extreme. In addition, according to JP Morgan on Monday, pension funds will have a rebalancing at the end of this month, about $ 90 billion will be available for investments, and the choice may fall on the government bonds, because they of appealing valuations.

Fed officials Williams and Bostic, commenting on the rally in bond yields, said that it is unlikely that the Fed will somehow react to this move, since it is natural and stems from the reassessment of economic growth expectations due to positive data. They also downplayed the impact of fiscal stimulus on inflation. Judging by Powell's speech last week, the Fed's stance on inflation is that the observed inflationary effects are temporary, so no response is required. Consequently, if the FED is correct, the inflation premium in bonds would also need to adjust downward with inflation weakening later.

Let's hope that 1.5% in 10-year yields will become a psychological borderline and the “pernicious” effect of bond rout worldwide on stock assets will not develop further. A cautious buy on SPX and a short dollar is justified, despite the risk of continued slide in bonds to more extreme levels. All the same, world economy has not yet recovered enough to confidently dump bonds.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 65% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.