The IndeX Files 26-11-2019

Trade Deal Speculation Driving Markets

Benchmark global equities indices remain well supported this week, though better strength is being noted in UK and European asset markets so far. Risk sentiment has been much firmer over recent weeks though we do seem to be in a low volatility period currently.

The dominating theme continues to be that of US-Sino trade relations and the speculation on whether a deal will be agreed ahead of fresh US tariffs. The market is still anticipating that a deal will be done though over the last week or so there appears to be some doubt creeping in. Conflicting news reports have been casting uncertainty over the negotiations and with a signing date yet to be agreed, US asset markets at least, remain below recent highs. Asian equities have recovered at the start of the week as a stronger Dollar is pushing the Japanese Yen lower. However, this theme is subject to swift change on incoming trade-deal headlines.

In the UK and Europe, investors remain encouraged by the ongoing delay in Brexit as well as the expectations of further easing from the ECB. The UK Conservative party is the front-runner in the UK elections race which suggests that PM Johnson’s Brexit deal will likely be passed at some stage, keeping the UK on course for an orderly Brexit as of January 31st 2020.

Recent data weakness in the Eurozone is keeping investor sentiment geared towards further easing from the ECB. Speaking last week, the new ECB head Christina Lagarde highlighted the ongoing challenges facing the Eurozone. Unless investors note a significant recovery in key indicators over the coming months, further easing is likely. With this in mind, European indices should continue to trade higher.

Technical & Trade Views

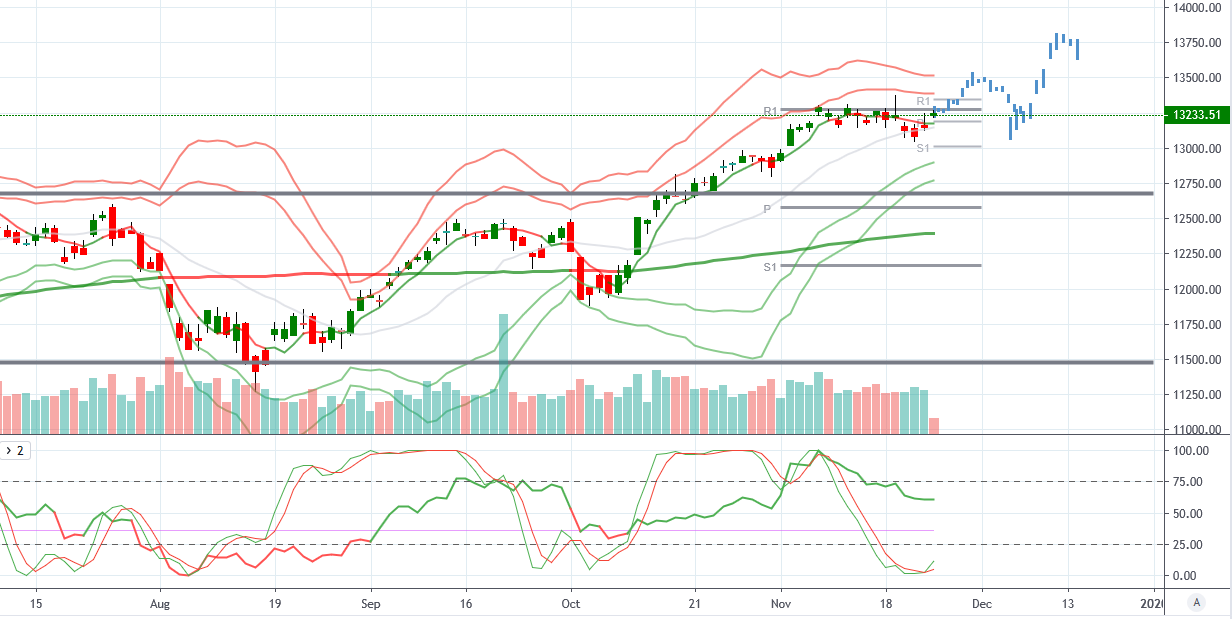

DAX (Bullish above 12667)

From a technical and trading perspective. DAX remains blocked by the monthly R1 at 13265.7 for now, which remains the key topside level to break. With longer-term VWAP positive, bias remains bullish and any correction lower is likely to find support as we retest recent broken highs.

S&P500 (Bullish, above 3031)

S&P500 From a technical and trade perspective. Price retraced lower and retested the monthly R1 at 3106.5 which has held as support for now. With Longer-term VWAP remaining supportive, the bias is for higher prices. If we do reverse lower here, any retest of the broken former highs at 3031 will likely find support, keeping the bullish bias intact while above the monthly pivot at 2981.6

FTSE (Bullish above 7233.4)

FTSE From a technical and trading perspective. FTSE is turning higher once again now and with longer-term VWAP positive again, the bias remains bullish in the near term. Monthly R1 at 7463.20 remains the key topside level to watch and I am anticipating a break higher unless we break below the monthly pivot at 7233.4.

Nikkei (Bullish above 22347.3)

From a technical and trade perspective. Price is trading back up towards the monthly R1 at 23346.1. With longer-term VWAP still positive, expecting the bull trend to continue and move to fresh highs. The last retracement lower saw decent volume into the dip also supporting a continue move higher.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72% and 71% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!