Bad news for the Economy – “Good” News for the DAX

Inertial forces in German production pave the way for further contraction - output in the sector declined by more than expected in September, data showed on Thursday. It should be taken into account that industrial sector PMI released earlier this week indicated increase in new orders which bodes well for the output growth in 4Q. However, with the September fall, key Eurozone economy will most likely have to go through a technical recession in 3Q. Positive prospects are too remote to be priced in immediately in a concrete market optimism. But they are.

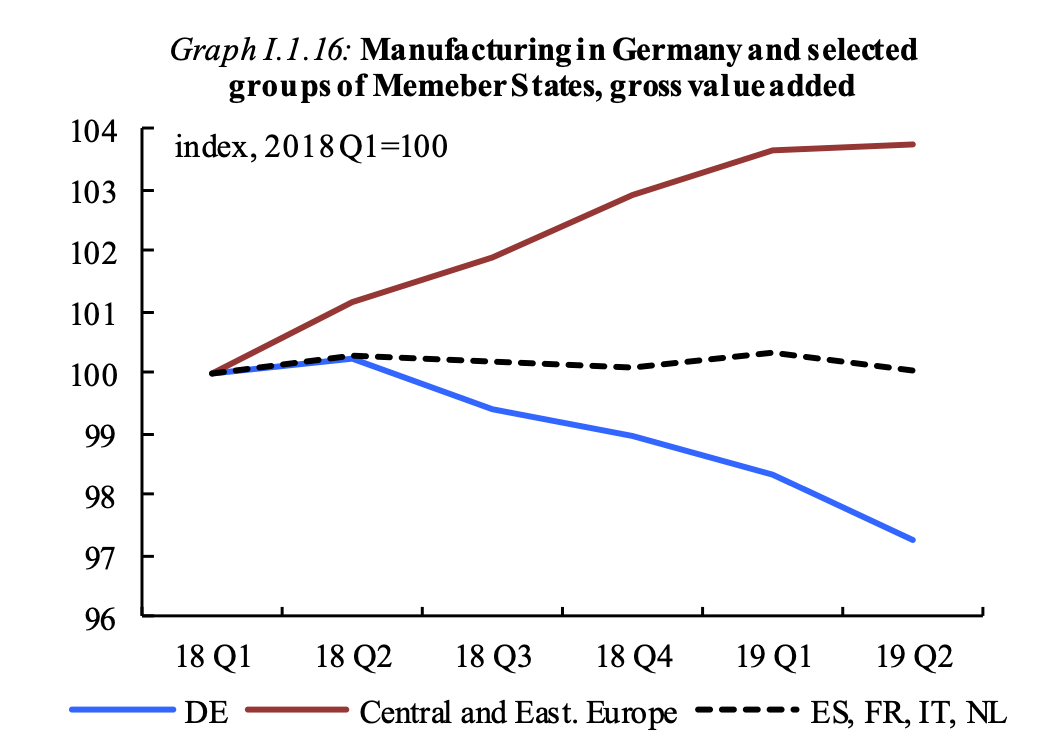

Germany seems to be the only anchor in the EU manufacturing growth…

…and Germany’s slump in industrial confidence seems to contagion other members

Industrial output fell 0.6% compared with August. The consensus forecast was -0.4%. With such trend, economic growth will almost certainly fall into negative area in the third quarter. Germany already has negative growth in the second quarter, so it is likely that the authorities will face a technical recession, which in theory should accelerate countercyclical spending. With subdued external risks like the trade war and Brexit, we are likely to see positive response from the stock market to the seemingly bad economic figures. Why? More fiscal stimulus means more government orders, money transfers, tax cuts, etc. what will help to boost companies’ earnings. German DAX rose 0.82% on Thursday.

Updated economic indicators of the European Commission released on Thursday also speak of more coming fiscal stimulus. Eurozone output growth is projected at measly 1.1% in 2020 (-0.1% compared with the estimate in July), Germany budget surplus is expected to shrink twice in 2020 - from 1.2% to 0.6%. Eurozone aggregate budget deficit is expected to rise from a historic low of 0.5% to 0.8% of GDP this year.

An echo of Draghi's words that fiscal policy should soon overtake monetary policy was also the estimate of the aggregate deficit in 2020 and 2021. It is expected to rise to 0.9% and then to 1.0%, respectively. With a nominal GDP of $18.8 trillion in 2018, this means a permanent increase in the money supply roughly by $170 billion in 2020 and by $188 billion in 2021.

China and the United States reported about stage-by-stage tariff reductions, but specific dates are yet unknown. There are rumors that signing of the “phase one” trade agreement will be delayed till December. As Chinese economy gets back on its foot, the recovery is likely to be gradually translated into Eurozone and particularly Germany growth (because China is the main exports market for Germany) but unfortunately this is relatively remote prospect.

In July-September, Germany industrial output fell 1.1%, a drop recorded in the chemical, metallurgical industries, heavy and automotive industries, as well as among manufacturers of electrical equipment. The construction sector remains stable due to steady demand for real estate and fiscal support through infrastructure costs. Business sentiment was stable in October and the economy is expected to close the fourth quarter with positive growth, IFO said last month.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72% and 71% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.