Daily Market Outlook, April 28, 2020

Daily Market Outlook, April 28, 2020

After sizable gains in many equity markets yesterday the market tone this morning is more cautious. Asian stock market performance has been mixed today with most moves only modest. The oil price has slipped again with Brent crude currently trading near $19bbl. Hopes of an early end to lockdowns has continued to act as a support to market risk sentiment. Italy yesterday unveiled a plan to gradually open up its economy from 4th May. France and Spain are expected to today give more details of their intention to start opening up from 11th May and 2nd May respectively. UK PM Johnson yesterday warned against moving too early but also said that more details of how some restrictions will be lifted may be revealed later this week.

In the UK The Lloyds Bank Business Barometer for April, which was released this morning, showed a big fall in business confidence. Sentiment regarding own trading prospects fell to a record low, while optimism about the economy as a whole also dropped sharply. Sentiment fell in all 12 measured areas of the UK and across all sectors. Special questions about the coronavirus revealed that 64% of firms are operating more than 50% below capacity with 20% not trading at all.

The rest of today’s data calendar is relatively light. In the UK, the CBI retail survey for April will be watched for further signs of weakness after Friday’s official data for March showed big falls in spending in most areas apart from groceries. There is no data of note in the Eurozone.

The US Federal Reserve’s FOMC meeting will take place over two days, starting today. There is a substantial US economic data calendar and the key ones will April Conference Board consumer confidence (Bloomberg Est: 87.9 from 120 in Mar), the advance March goods trade balance (Bloomberg Est: US$55bn deficit from US$59.9bn deficit in Feb), March wholesale and retail inventories, S&P CoreLogic CS 20-City Composite Home Price, and Richmond Fed Manufacturing Index for April (Bloomberg Est: -40 from 2 in Mar). Market attention will also stay on the US corporate earnings calendar with more than 30 S&P 500 companies reporting today

Today’s Options Expiries for 10AM New York Cut (notable size in bold)

- EURUSD: 1.0750-55 (630M), 1.0785 (320M), 1.0800 (500M), 1.0820 (750M)

- GBPUSD: 1.2200 (500M), 1.2400 (300M)

- USDJPY: 107.50 (3.3BLN)

Technical & Trade Views

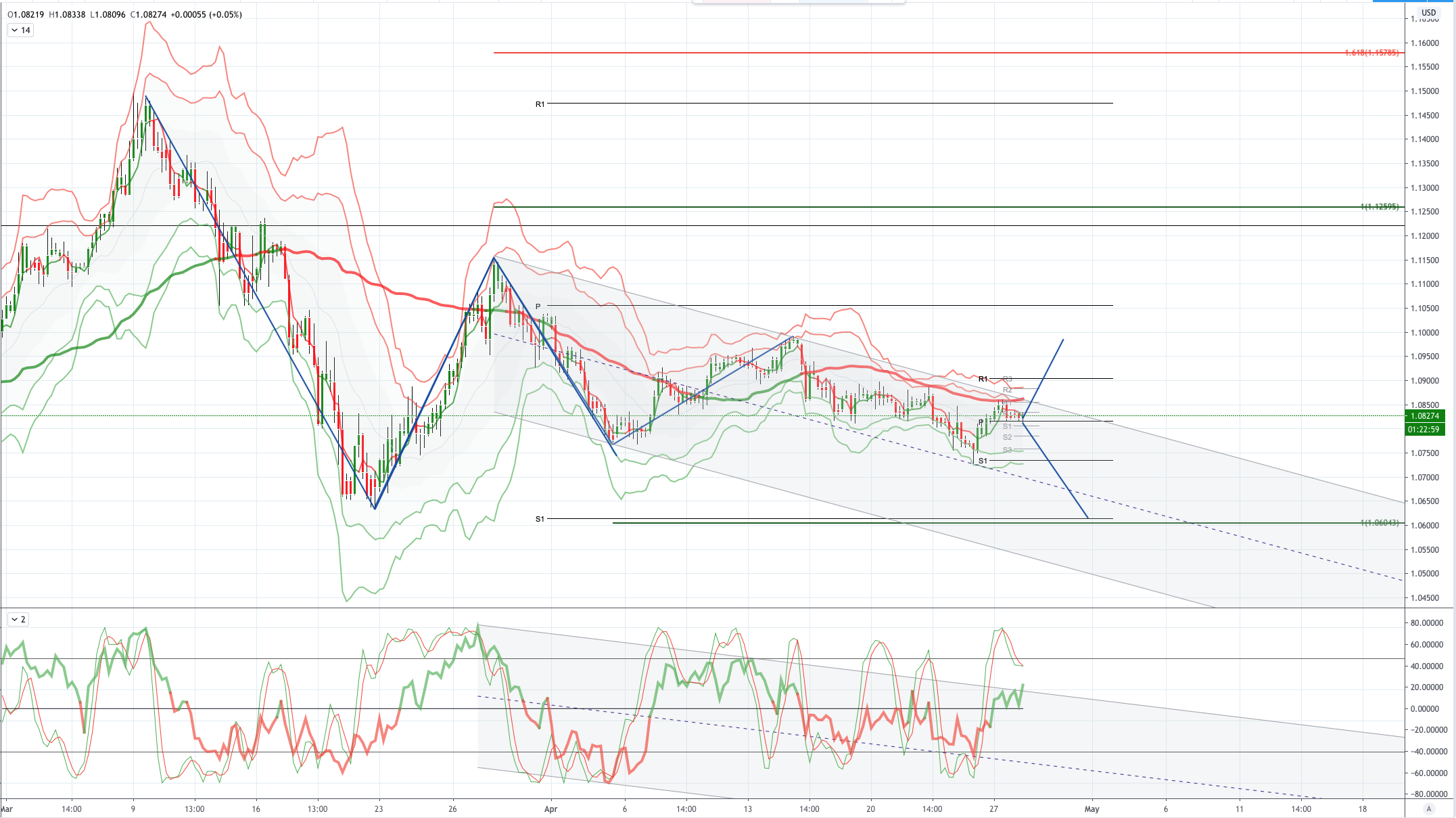

EURUSD (Intraday bias: Bearish below 1.09 targeting 1.0630, Bullish above 1.09 targeting 1.1050 )

EURUSD From a technical and trading perspective, 1.09 remains pivotal, a close above 1.09 would open a test of 1.1050. A continued failure to overcome the 1.09 hurdle will likely see prices grind lower to retest and breach last week's lows en route to the 1.0630 target. UPDATE EURUSD continues to rotate just above the weekly pivot at 1.08, as 108 continues to support we may see a squeeze higher to test the pivotal 1.09, Note the momentum study is threatening a breach its bearish channel

GBPUSD (Intraday bias: Bullish above 1.22 targeting 1.28)

GBPUSD From a technical and trading perspective, a pivotal test of the daily descending trendline is underway. A failure to sustain a breach of 1.2470 would concern the near term bullish bias suggesting another leg lower to test support back towards 1.2150

USDJPY (intraday bias: Bearish below 109 targeting 1.0465)

USDJPY From a technical and trading perspective, range contraction persists,albeit with a downside bias, a breach of 106.80 should inject downside momentum. A topside breach of 108 would delay donside objectives opening a retest of range resistance above 109 before lower again

AUDUSD (Intraday bias: Bullish above .6250 targeting .6700)

AUDUSD From a technical and trading perspective, as .6250 now acts as support look for a grind higher to set up a test of the pivotal .6430/90 area. A close through here sets bullish sights on the equality objective at .6695. Only a decline back though .6250 would concern the bullish bias.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 73% and 70% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!