German Ifo Falls For 11th Consecutive Month

It has been another poor showing for German data this week as both the German IfO readings released on Monday and Q2 GDP released on Tuesday have highlighted further weakness in the second largest economy in the eurozone.

German Ifo Falls Again

The Ifo reading on Monday showed an eleventh consecutive monthly drop over August moving to 94.3, from 95.8 in July. The Ifo is now sitting at its lowest levels since 2012. Over the last year, the move lower has been significant with the index moving from levels of 104.2, close to all time highs, to the current low standing. Indeed, both current assessment and expectations elements of the index has deteriorated sharply. In August, the expectations element fell to its lowest level since June 2009.

The main drag continues to be weakness in the German manufacturing sector which shows no signs of improvement in the near term. Indeed, increased inventories and weakened order books are not a good omen for industrial activity over the coming months. It would require significant easing of the ongoing trade tensions and a general improvement in broad sentiment to help fuel an increase in industrial activity towards the end of the year. Furthermore, the manufacturing slowdown and persistent, increasing external issues have now started to dampen the domestic economy.

German Q2 GDP Contracts

The release of the second estimate of German Q2 GDP yesterday, showed the economy having still contracted over Q2 by 0.1% to just 0.4% on the year. There are some minor positives: the majority of the decline was driven by weak exports while domestically, the only sector which contracted was construction. However, the near term outlook remains dire and the risk of a further contraction in Q3, which would signal a technical recession, remains elevated. Rising external pressures as well as the ongoing collapse of the German manufacturing sector is creating a very dangerous situation and calls are now growing for action from the German government.

Easing Expectations Grow

It is not just expectations for action from the German government which are rising. The market is now widely expecting the ECB to announce a range of measures when it meets in September. The release of the July meeting minutes showed that the majority of policy makers favour a multi-pronged approach over a single action and given the escalation in US / China trade tensions recently, it seems the ECB is now poised to act. In the past, when the ECB has signalled forthcoming easing but then under-delivered, the backlash has been swift and severe. This time around, and with Draghi’s term coming to an end, it is likely that we will once again see full fireworks from the ECB.

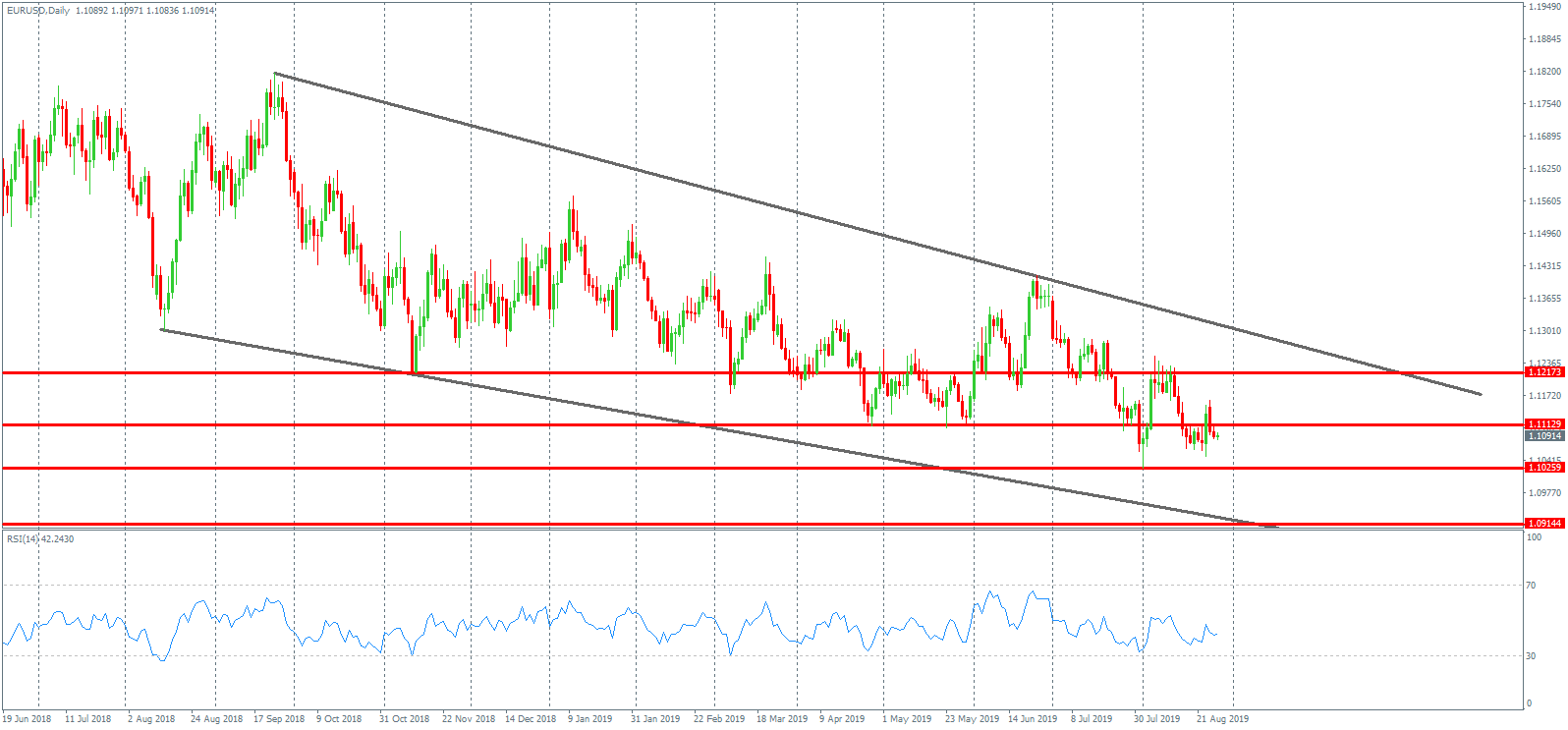

Technical Perspective

EURUSD continues to battle it out around the 1.1112 level, in the middle of the bearish channel which has framed price action over the year so far. The local bearish trend line from June highs, offers immediate resistance, while above here, the 1.1217 level sits just ahead of the bearish channel top. To the downside, 1.1025 remains the key support, a break of which paves the way for a run down to deeper support at the 1.0914 level where we have the bearish channel low.

Please note that this material is provided for informational purposes only and should not be considered as investment advice. Trading in the financial markets is very risky.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

With 10 years of experience as a private trader and professional market analyst under his belt, James has carved out an impressive industry reputation. Able to both dissect and explain the key fundamental developments in the market, he communicates their importance and relevance in a succinct and straight forward manner.