S&P500 LDN Open Trading Update 22/5/26

S&P500 LDN Open Trading Update 22/5/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

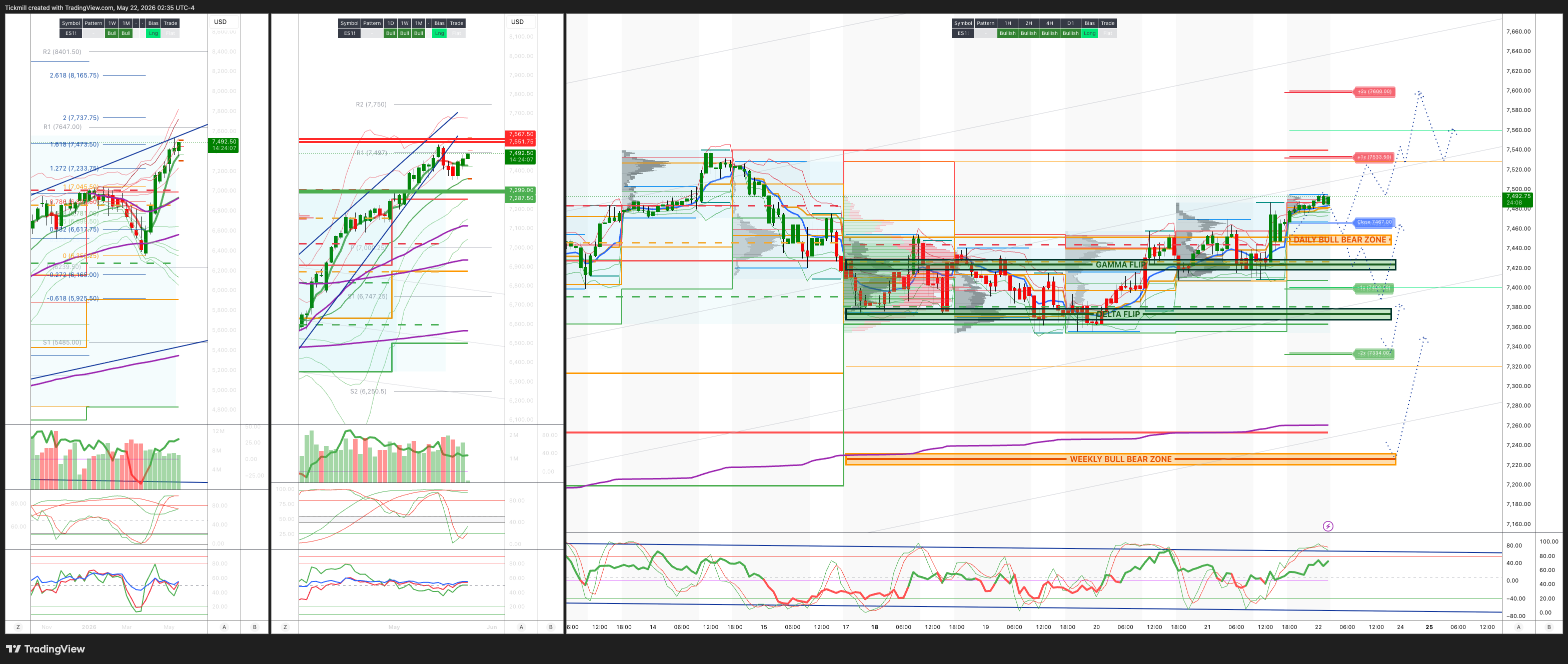

WEEKLY BULL BEAR ZONE 7220/30

WEEKLY RANGE RES 7286 SUP 7550

June MOPEX Straddle: 274pt range implies a OPEX to OPEX range of [7134, 7683]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.03 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BULLISH 7432

WEEKLY VWAP BULLISH 7292

MONTHLY VWAP BULLISH 6898

DAILY STRUCTURE – OTFLH - 7408

WEEKLY STRUCTURE – OTFH - 7363

MONTHLY STRUCTURE - OTFH - 6514

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7450/40

GAMMA FLIP 7425

DELTA FLIP 7374

DAILY RANGE RES 7533 SUP 7408

2 SIGMA RES 7600 SUP 7334

VIX BULL BEAR ZONE 19

TRADES & TARGETS

LONG ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET DAILY RANGE RES

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Squeezy’

US equities finished modestly higher, but the day was much busier beneath the index surface as Iran/US headlines, quantum-computing grant headlines, NVDA digestion, and consumer earnings all pushed the tape around. The S&P 500 gained 17bps to 7,446 with a USD 2bn MOC imbalance to buy, the NDX rose 20bps to 29,357, the Russell 2000 outperformed with a 93bp gain to 2,843, and the Dow added 55bps to 50,286. Volumes were lighter than average at 17.65bn shares versus a YTD daily average of 19bn. Cross-asset price action was supportive: VIX fell 390bps to 16.77, WTI slipped another 84bps to USD 97.44, the 10-year yield eased 2bps to 4.56%, gold was roughly flat at USD 4,542, DXY rose 8bps to 99.17, and Bitcoin was little changed at USD 77,621.

The broad message is that the market is trying to repair. Lower oil, slightly lower yields, and a calmer VIX backdrop are allowing risk appetite to recover, while the post-NVDA AI complex remains broadly supported even though NVDA itself traded lower. The index move was small, but the internals were more active: AI, momentum, internet laggards, shorts, retail winners, and small caps all found bids at different points. The USD 2bn MOC to buy was also a constructive close, especially after several recent sell imbalances.

NVDA was the key micro event, and the reaction was revealing. The stock fell around 2% despite a solid beat-and-raise, and the desk noted that it was shockingly quiet from an incoming and flow perspective. NVDA has now traded lower on the day after earnings in six of the last eight quarters, which reflects the fact that fundamental strength has become extremely well previewed. The market was not surprised by strength; it was looking for incremental upside and perhaps did not get enough to force a major chase.

From here, NVDA’s flow dynamic looks two-sided. On the supportive side, capital returns are ramping, with the company buying back USD 20bn last quarter and raising authorization. That creates a meaningful corporate bid. On the other side, NVDA remains a source of funds for investors looking to finance more dynamic pockets of AI such as memory, new issues, quantum-related themes, neoclouds, and other higher-beta beneficiaries. This does not break the NVDA story, but it changes its role: less of a clean squeeze vehicle, more of an AI anchor and funding source.

The broader AI complex still caught a bid after NVDA, which matters more than NVDA’s own one-day stock move. The earnings print validated demand, capex durability, and the datacenter cycle. That was enough to support the ecosystem even if the stock itself could not rally. In a market that had just experienced a sharp momentum unwind, confirmation from NVDA helped stabilize the factor tape.

Internet was one of the more interesting rotations. There has been heavy incoming recently around the persistent lag in internet names excluding hyperscalers, and SPOT’s analyst day reaction appeared to unlock a relief rally across oversold and out-of-favor internet. SPOT surged 13%, while RDDT gained 4%, NFLX rose 2%, and SNAP added 1%. This felt less like a broad fundamental re-rating and more like a squeeze in under-owned, lagging internet exposure. Still, it is important because it suggests investors are looking beyond the most obvious AI hardware winners and are willing to rotate into neglected growth pockets.

The short squeeze element was obvious. Goldman’s Most Rolling Short basket rose 2%, while Tech Shorts jumped 6%. Pain points included IBM, NBIS, QCOM, GFS, and CHTR. This fits the broader positioning backdrop: investors remain nervous about Iran, rates, and oil, but rather than hedging through single-stock shorts, they have built large short exposure in US macro products. Short exposure in US macro products across index and ETFs on Prime has now risen above pre-Iran ceasefire levels and sits at a 10-year high. That creates real index-level squeeze risk.

This is an important market structure point. If investors are hedged through index and ETF shorts instead of single-stock shorts, positive macro headlines can trigger broad index-covering rallies rather than isolated single-name squeezes. With oil down, rates stable, and Iran/US headlines improving, the risk of forced cover at the index level is high. That helps explain why the tape can levitate even when some major stocks, like NVDA and WMT, are down.

Consumer was mixed but ultimately better than feared. WMT fell 7% after noting customer pressure, which was consistent with existing sentiment around the squeezed consumer. Yet retail broadly acted well, with RL and WSM squeezing on earnings and ROST up 7% after the close. ROST results were as good as hoped despite high expectations, and the 2Q guide was also as good as hoped. The only pushback was that SG&A could have been better given comps were well above consensus. This broader retail resilience suggests that the consumer story remains uneven rather than uniformly broken.

That nuance matters. WMT’s customer-pressure commentary highlights the squeeze from inflation and energy, particularly for lower-income households. But RL, WSM, and ROST show that individual retailers can still beat if inventory, brand, value proposition, and margin execution are strong. The consumer trade is becoming more idiosyncratic, which favors stock selection over broad sector calls.

Flows were more active. The floor was a 7 out of 10, with offsetting activity. Asset managers finished net buyers, led by tech, communication services, healthcare, and financials. Hedge funds were USD 1bn net sellers, driven by supply in tech, with long sales exceeding short sales. That suggests real-money investors are still allocating into the market, while hedge funds are using strength to reduce tech exposure or rebalance after recent factor volatility.

Derivatives were calmer despite headline-driven intraday swings. SPX closed green while vol finished lower, breaking the recent positive spot/vol correlation. Skew relaxed across the curve on the move higher, which is consistent with reduced immediate downside demand. RUT vol outperformed, which makes sense given the strong move in the Russell spot. The more notable development was continued demand for VIX ETPs even as the market rallied. That complex has been a major buyer of vol and is helping keep VIX elevated despite the S&P being at or near all-time highs. The implied move for the end of the week is 0.67%

The desk likes VIX ratios and one-up put spreads to play for VIX rolldown, and sees risk reversals as attractive for a potential vol crush. The logic is that if oil remains below USD 100, yields stabilize, and Iran headlines continue improving, VIX could compress further. However, because investors are still nervous and heavily hedged through macro products, the decline in vol may not be linear.

The trading takeaway is that the market’s risk/reward has improved tactically, but the setup is increasingly squeeze-driven. Lower oil and lower rates have removed the immediate macro pressure, NVDA validated the AI cycle, and retail earnings are not uniformly bad. At the same time, index/ETF short exposure is at a 10-year high, which creates fuel for further upside if the macro headlines cooperate. That argues against being too bearish at the index level.

But there is also a reason not to chase blindly. NVDA’s muted reaction shows that good news is already well understood in parts of AI. WMT’s decline shows that the consumer is still under pressure. The market remains headline-sensitive to Iran/US developments, oil, and yields. And the rotation into shorts and laggards can be violent but not always durable.

The best stance is to stay tactically constructive while managing concentration. Index squeeze risk is real, especially with macro-product shorts at decade highs. Small caps and equal-weight can continue to benefit if yields and oil remain contained. AI remains valid, but NVDA may be more of a stable anchor than the highest-beta upside expression. Internet laggards, software, selective retail, and short-interest names can keep squeezing if flows continue to broaden.The market is repairing on lower oil, stable yields, and a post-NVDA validation of AI demand. The tape is not euphoric at the single-stock flow level, but the positioning backdrop is combustible because investors are heavily short index and ETF products. That means the biggest near-term risk may not be downside — it may be an upside squeeze if Iran headlines improve further and rates stay calm

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!