Was Market Reaction to the US GDP Contraction Too Emotional? Looking Under the Hood, it may Seem so

Demand for risk increased markedly, greenback declined and US bond yields took out recent lows (2.8% for 10-year bonds, 2.9% for 2-year bonds), finding an equilibrium at the lowest levels since April, as the US economy unexpectedly for many, including doomsayers, showed a negative growth rate in the second quarter. Nominal output fell by 0.9% QoQ, missing the estimate of 0.5%, which formally means that US entered recession. The release of the report made a strong impression on the dollar, as earlier at the meeting the Fed made it clear that after hiking interest rate by 75 bp two times in a row, further rate hikes will be much more dependent on incoming data i.e., adjustment of the path of tightening in either direction is now more likely. After the release, the dollar index fell from 107 to 106.50, and then continued its gradual decline to 105.50, from where it was able to rebound:

The contraction in US GDP has cast a shadow over the investment thesis that US assets provide the best risk/reward ratio in the face of a global slowdown, high inflation, geopolitical risks and a cycle of central bank tightening. In addition, the weak report spurred a revision of the Fed's policy tightening forecasts: the expected aggregate size of the rate increase by the end of the year was reduced from 100 bp to 90 bp.

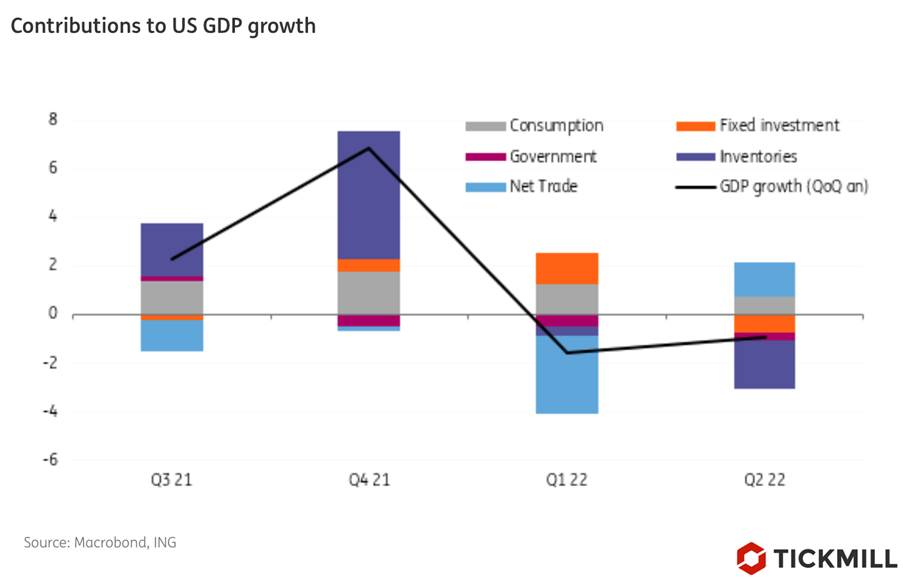

However, looking at the details of the report, one can find arguments in favor of the fact that the market reaction to the weak report was excessive and, in fact, the US economy did not enter a recession. If we look at the contribution of each component of the GDP, we can see that growth was pulled down by volatile components - firms' investment in inventories (-2% of the total) and investment in fixed assets (-0.7% of the total). Consumer spending growth in the second quarter was positive at +1%:

The downturn phase of the business cycle is usually characterized by contraction in consumer spending and rising unemployment, but so far in the US, these two indicators do not give cause for concern. In the labor market, initial jobless claims have risen for the fourth week in a row, but the Fed has warned that the tightening policy will have some costs, so the deterioration in individual indicators is not much of a surprise.

The Fed officials' argument that recession risks are exaggerated also continues to be based on the fact that the classic signs of lower consumer spending and rising unemployment are absent. Raphael Bostic said in an interview yesterday that the economy is far from recession, but he shares concerns that a "self-fulfilling prophecy" effect could actually make matters worse.

In general, in my opinion, the effect of a weak report on GDP should come to naught next week and the dollar index will be able to resume growth. From a technical point of view, the dollar index completed a bearish pullback to the lower edge of the main trend channel, which creates the conditions for a rebound:

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.